According to the PYMNT 2023 Money Mobility Index, businesses that offer their customers various payment options rank high in customer satisfaction scores.

This trend shows the importance of offering flexible payment methods to meet varying client preferences and enhance overall client experiences.

By exploring and implementing various payment solutions, you can cater to a broader audience and foster greater client loyalty and satisfaction.

This article will explore various payment methods and options that MSPs can offer their clients to ensure flexibility, timely payment/billing cycles, and improved financial efficiency.

We will also discuss innovative payment solutions and offer strategies for effective implementation, equipping you with the tools to enhance your payment processes and drive success.

Comprehensive List and Review of MSP Payment Options

A Modern Treasury survey has identified delivering a better customer experience as a top priority for businesses seeking to improve their payment operations. The research indicates that 41% of organizations consider this a critical benefit.

Payment options can significantly influence client satisfaction and an MSP's operational efficiency.

Selecting the correct payment methods can streamline your processes, enhance customer satisfaction, and drive business growth.

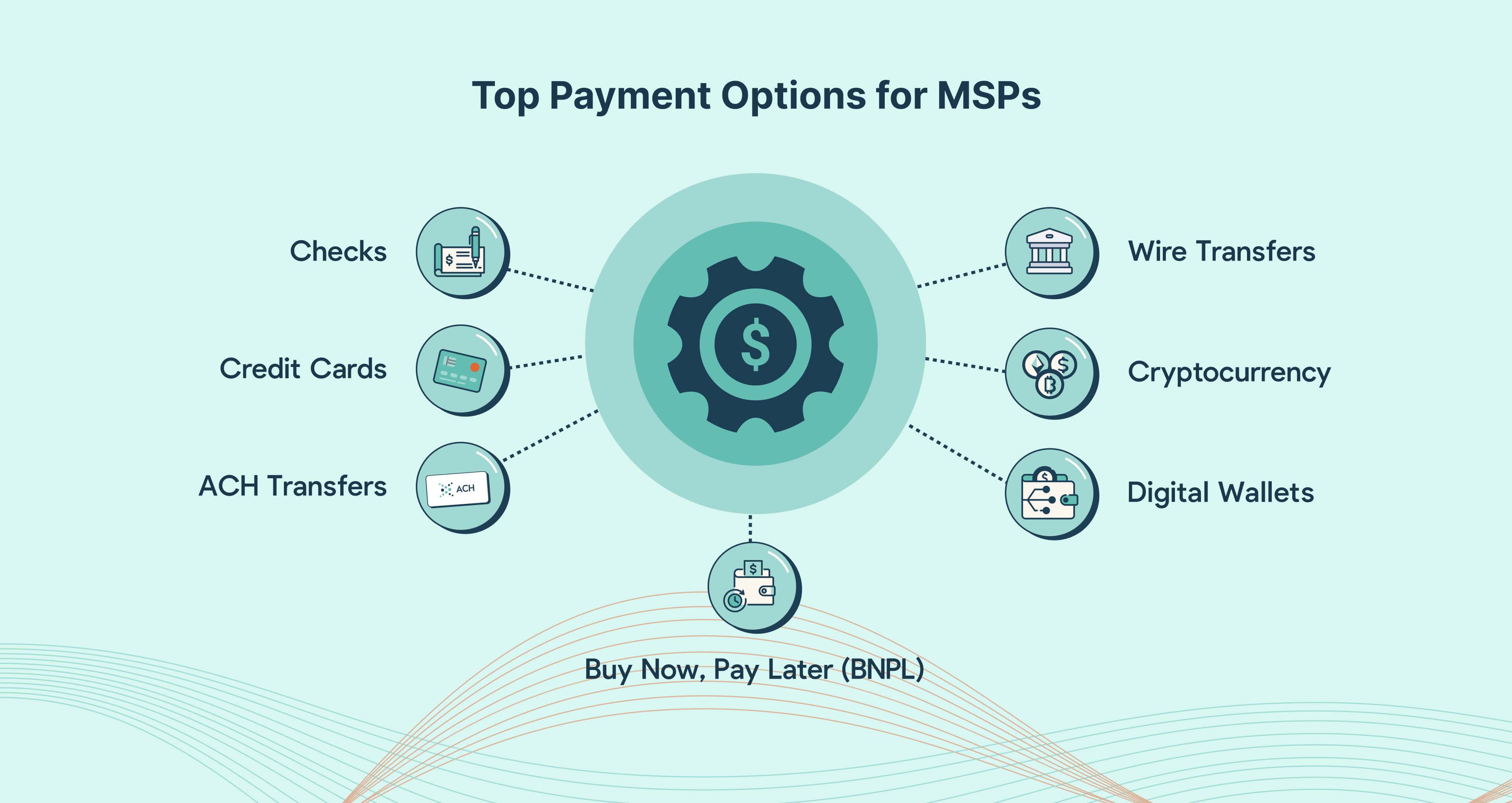

Here are the top payment methods MSPs can offer their clients. We will discuss each option's advantages and potential limitations.

1. Checks

According to the AFP Online Digital Survey Report, checks for B2B transactions are still prevalent and are used by 33% of businesses.

Although checks are becoming increasingly rare and considered outdated, some companies still use them as a payment method, especially for large transactions.

MSPs often offer this for clients who prefer traditional payment methods or need to make large payments that exceed digital transaction limits.

One advantage of using checks is that they offer a tangible payment record, which can be beneficial for accounting and auditing purposes.

Your clients can also postdate checks, allowing for a certain degree of control over payment timing.

Post-dated checks offer better cash flow management, as your clients can schedule payments for a future date.

The benefit to you as an MSP is that it allows you to plan your finances more effectively and align incoming funds with planned expenditures, providing greater control over payment timing and financial planning.

However, manually handling and processing checks demands extra administrative resources, such as tracking and reconciling payments, which can be time-consuming and labor-intensive.

According to research by QuickBooks, 65% of businesses surveyed said they spend 14 hours a week on administrative tasks when collecting payments.

One of the biggest challenges to using checks is that they are significantly slower than digital payment methods. This leads to delays in receiving funds and thus causes potential disruptions in cash flow. In addition, checks are also the most vulnerable to fraud.

2. Credit Card Processing

MSPs use this payment method when you want your transactions to be completed swiftly. At the same time, you can also cater to clients who prioritize quick and efficient payment solutions.

For MSPs, the average cost of credit card processing is 1.5% to 4% of the total transaction. This can eat into their profits, especially for large transactions.

If an MSP processes $100,000 in payments monthly, credit card fees averaging 3% would result in $3,000 in monthly fees, or $36,000 annually.

Despite these costs, the ability to provide clients with a seamless, flexible payment option strengthens relationships and ensures timely payments, ultimately contributing to more predictable revenue and client satisfaction.

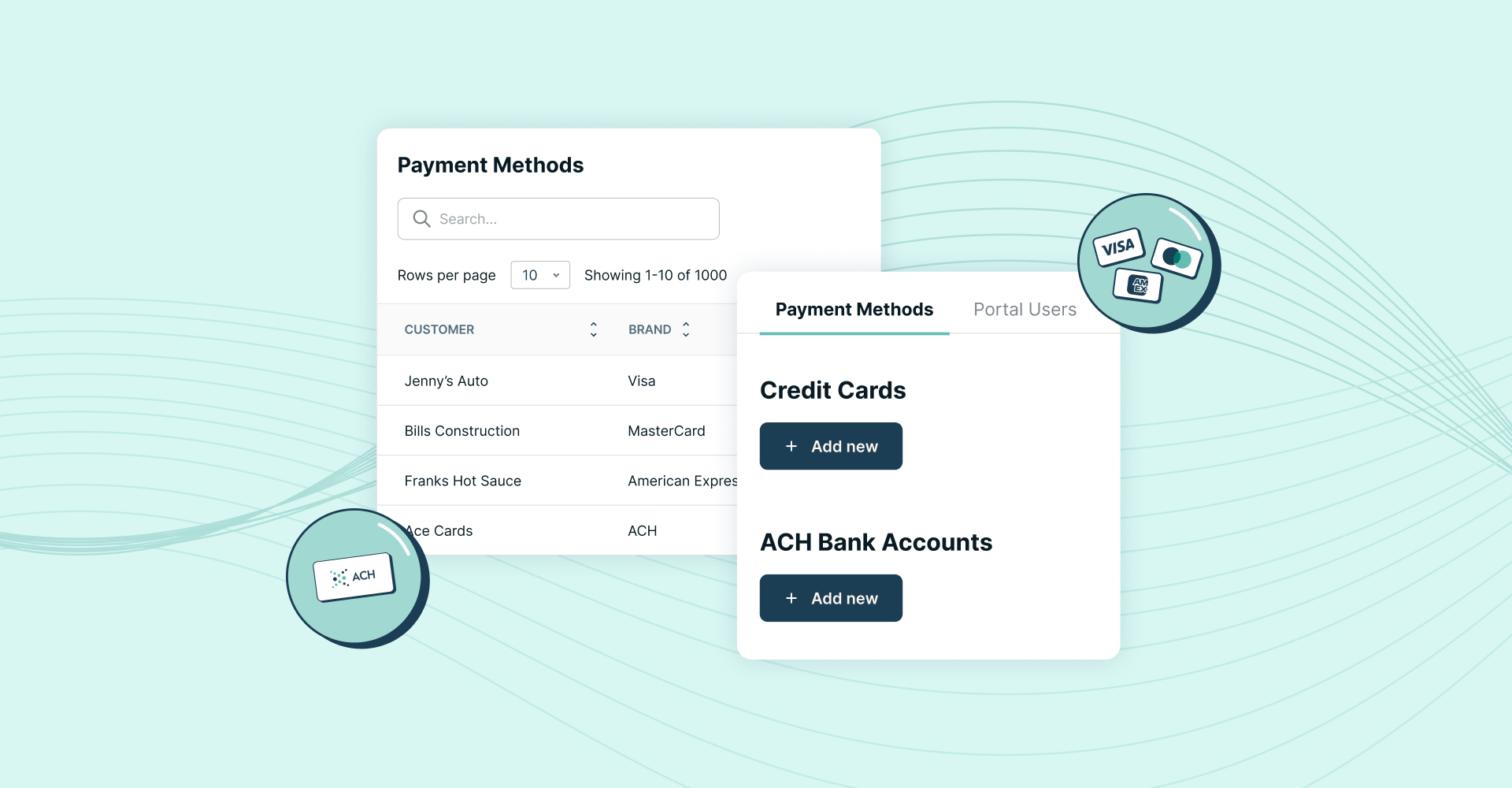

3. ACH Transfers

ACH (Automated Clearing House) is an electronic network for processing payments, allowing funds to be transferred directly between bank accounts.

One of the main advantages of ACH transfers is that they give you lower fees than credit card transactions, making them cost-effective for handling large volumes of payments.

Take, for example, an MSP with a monthly transaction volume of $100,000, split equally between ACH and credit card payments; here’s the detailed cost breakdown:

- ACH Transactions: With a monthly volume of $50,000 and each transaction being $5,000, there are 10 transactions per month. some text

- The cost is $0.25 per transaction plus a $0.25 transaction fee, totaling $5 per month (10 transactions * $0.50).

- Annually, this amounts to $60.

- Credit Card Transactions: The remaining $50,000 processed via credit card incurs a 3% fee, resulting in a monthly cost of $1,500. some text

- Annually, this amounts to $18,000 ($1,500 per month x 12 months).

Note: The $0.25 ACH transaction is not the industry average. FlexPoint typically offers a cost-effective method of accepting ACH payments.

By using ACH for half of the transactions, the MSP benefits from a lower fee than credit card payments, illustrating ACH’s cost-effective advantage in managing payment processing expenses.

However, unlike credit card payments, ACH transfers are not instantaneous; they typically take 2 to 5 business days to process, which might impact cash flow if immediate payment is required.

4. WireTransfers

According to the Federal Reserve Payment Insight Brief, Wire transfers grew by 23% – second only to digital wallets for business transactions in the US.

Wire transfers are processed within minutes. They are more expensive, with fees ranging from $10 to over $50, and are better for urgent, large, or international transactions.

On the other hand, ACH transfers typically take 2 to 5 business days and are cost-effective, ideal for recurring payments within the U.S.

For an MSP handling a $1,000 payment, ACH transfers typically take 2-5 days to process and cost around $0.25 per transaction, totaling $0.25 in fees.

In contrast, a wire transfer might process the payment within hours but could incur higher fees, such as $30 for an international wire transfer.

Thus, for a $10,000 transaction, the ACH method would cost $0.25 and take a few days to process, while the direct bank transfer, despite offering quicker access to funds, would cost $30 and be preferred for urgent transactions.

This method facilitates substantial transactions directly between banks, making it ideal for high-value payments that require enhanced security. Direct bank transfers often involve rigorous validation and encryption, offering high protection against fraud.

5.Digital Wallets

Bank of America believes using a digital wallet through tokenization will help reduce fraud and the administrative burden of acquiring data.

According to the AFP payment fraud survey key highlights 2023, digital wallets are the second most secure means of receiving business payment after cryptocurrency.

Digital wallets like PayPal, Apple Pay, and Google Pay provide a convenient and secure way to handle transactions. These services streamline payment processes, allowing clients to pay quickly using their smartphones, smartwatches, or other devices without needing physical cards or cash.

Furthermore, tokenization in digital wallets enhances security by protecting sensitive financial information from fraud. It also increases efficiency and improves customer experience, as it simplifies transactions and caters to various client preferences.

For example, when a client needs to pay for a completed IT support service, the MSP can send an invoice through the digital wallet’s platform.

The client receives a notification and can pay instantly using their smartphone without needing checks or credit card information.

The MSP gets the payment in real-time, and the transaction is securely processed through tokenization, minimizing fraud risk.

Even though this sounds simple, it is not optimal for MSPs with larger average transaction sizes than traditional businesses.

For instance, integrating these wallets into their existing systems may present technical challenges like compatibility and transaction reconciliation.

More so, MSPs are skeptical of the adoption for several reasons, including:

- Integration Issues: Connecting digital wallets with existing systems can be complicated and costly.

- High Fees: Transaction fees and service charges from digital wallets can be a deterrent. For example, PayPal charges 2.9% + fixed fee for domestic transactions.

- Client Resistance: Some clients prefer traditional payment methods and may be reluctant to switch.

- Third-Party Dependence: Relying on external providers can lead to issues if their service is disrupted.

- Regulatory Challenges: Complying with financial regulations and local laws can be difficult.

- Low Adoption: The benefits may not justify the implementation effort if only some clients use digital wallets.

Additional Reading:

6. Buy Now, Pay Later Options

According to a report by Juniper Research, B2B BNPL transactions are expected to reach $687 billion globally by 2028, up from $334 billion in 2024.

This payment solution offers you and your clients flexibility in managing cash flow. This option allows your clients to spread the cost of services over time. Often, there are no interest charges if paid within a specified period.

BNPL (Flexible financing) can be a powerful tool for attracting and retaining clients. It is beneficial if you are facing budget constraints or seeking to preserve working capital. Removing immediate financial barriers can help close deals faster.

For instance, an MSP offering IT services may have clients who need help paying for an infrastructure rebuild with new equipment costing $50,000. Most small and mid-sized MSP clients might not have the funds to invest in IT infrastructure.

Alternatively, the MSP can offer a flexible financing option that allows clients to spread the cost over several months or years at a relatively low interest rate.

7. Cryptocurrency Payments

A nationwide survey conducted by Zogby Analytics showed that one-third of small businesses in the US accept crypto as a means of payment.

Cryptocurrency is becoming increasingly popular among US businesses due to its benefits of lower transaction fees, enhanced security, and reduced vulnerability to fraud. In 2022, cryptocurrency transactions experienced fraud rates of just 5%, making it one of the most secure payment methods available.

Cryptocurrencies are a high-security blockchain technology system. Blockchain technology verifies and records transactions, reducing fraud risk. Additionally, transactions are processed quickly, improving cash flow management.

Adopting cryptocurrency as a payment method has several challenges, including:

- Volatility: Cryptocurrency values can fluctuate dramatically, making predicting and managing financial outcomes difficult.

- Tax Implications: Tax regulations for cryptocurrency transactions can be complex and vary by jurisdiction, leading to potential compliance issues.

- Accounting Implications: Integrating cryptocurrency payments into accounting systems requires specialized knowledge and tools, complicating financial reporting and management.

- Reconciliation: Reconciling cryptocurrency transactions can be challenging due to its decentralized nature and the need to track multiple transactions and exchanges.

- Local Regulations: Different regions have varying regulations regarding cryptocurrency, which can create legal and operational hurdles for MSPs.

According to this Reddit thread on r/msp, most MSPs are still wary of offering their clients cryptocurrency as a payment method.

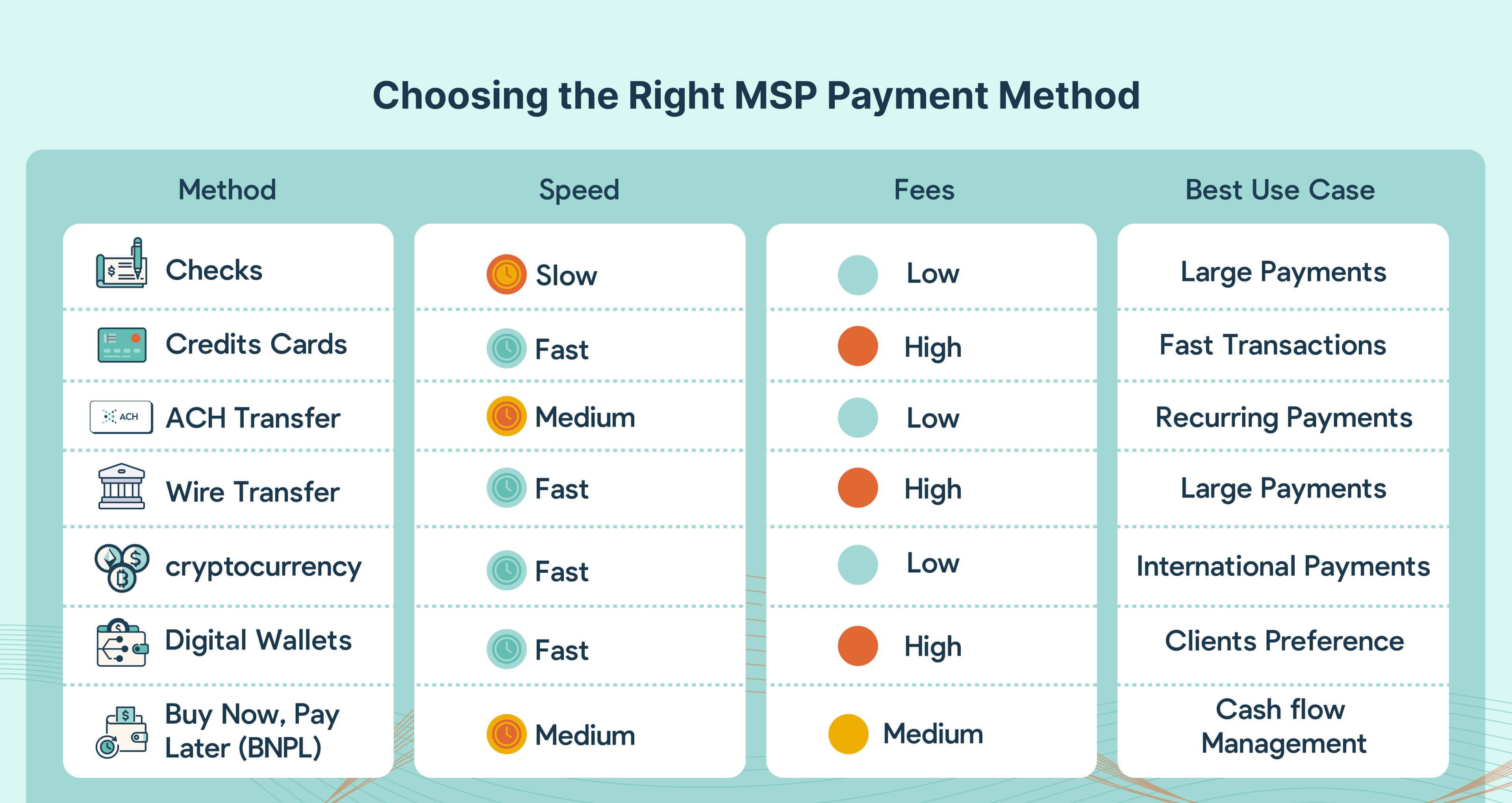

Summary Table: MSP Payment Options

This table compares and summarizes key aspects of the payment methods discussed:

8 Strategies for Enhancing MSP Payment Options for Clients

In the previous sections, we explored various payment methods, both digital and traditional, to help you choose the best billing solutions for your MSP. We also compared these payment options to understand their usability and limitations.

Now, we'll focus on strategies to optimize your payment systems.

We'll discuss the importance of integrating payment systems with your management software and implementing advanced security measures. These strategies will help you effectively meet your clients' payment needs.

Here are key strategies to ensure efficiency, security, and a seamless client experience:

1. Integration with MSP Management Software:

When integrated with payment software, management software like PSA or RMM tools (ConnectWise, SuperOps) ensures accurate data entry through automation. This helps you streamline your workflows and reduce the errors usually associated with manual data entry.

For example, when an MSP integrates PSA and RMM tools with payment software, service tickets, and system performance data automatically update billing information. This integration ensures that invoices are accurate and reflect the amount due, reducing manual errors and discrepancies.

As a result, you reduce billing inaccuracies, and clients are charged correctly. Also, financial reporting becomes more precise, leading to improved client satisfaction.

2. Integration with Accounting Software:

Ensure payment systems sync effortlessly with accounting software (such as QuickBooks Online, QuickBooks Desktop, Xero). This integration automates reconciliation processes and ensures compliance with financial reporting standards. Doing so reduces errors and saves valuable time for your accounting teams.

For instance, WJP Technology Consultants, a Texas-based MSP, faced a billing challenge because its provider was too costly and limited.

However, they seamlessly integrated their accounting and payment software after switching to another MSP-specific payment software, which helped them increase their payment processing speed by 300%.

Integrated payment and accounting software is crucial to automating reconciliation, which verifies and matches your invoice with payment records. Automated reconciliation saves you and your team 9 hours of reconciliation every month.

3. Enhanced Security Protocols:

Implementing robust security measures protects transaction data from unauthorized access. These measures include encryption, tokenization, multi-factor authentication (MFA), and passwordless authentication to safeguard sensitive information.

Update your security protocols regularly to identify and mitigate vulnerabilities effectively. Conduct thorough audits to ensure client data remains secure at all times.

Also, automation payment software enhances security by offering robust and encrypted processing, adhering to top payment security standards like PCI-DSS and SAQ-A compliance. This automation minimizes human error and unauthorized access by automating transaction authorizations.

The software securely handles sensitive payment data with tokenization and encryption, bolstering overall financial security. Similarly, it thoroughly audits and assesses your payment security to maintain PCI compliance and ensure client data remains secure.

4. User-Friendly Interfaces:

Create easy-to-use payment portals for all clients, regardless of technical expertise. A clear and concise interface reduces frustration and encourages timely payments. It simplifies the payment process, enhances the overall user experience, and lowers support inquiries.

For instance, SkyCamp Technologies, an Ohio-based MSP, had issues addressing its billing needs. It tried using QuickBooks ACH for payments but lacked integration and invoicing capability. As a result, it had to invoice clients manually, which was time-consuming.

However, using a payment platform with a user-friendly centralized client portal, they increased pay by 20% with autopay.

5. Customization Options:

Implementing customization options can increase client trust and satisfaction, as clients perceive the MSP as more professional and attentive to detail. It also reinforces brand identity, which can improve client retention and loyalty.

Customization allows you to tailor invoices and payment portals to reflect your branding, such as adding logos, colors, and personalized messaging.

For instance, an MSP that includes its logo, color scheme, and brand messaging throughout invoices and payment portals can reinforce its identity and reliability. This personalized touch makes the process more visually appealing and instills confidence in clients, making them feel valued and secure.

Therefore, clients are more likely to trust you and be satisfied with the service, leading to stronger business relationships and increased customer loyalty.

6. Automated Invoicing and Reminders:

Utilize computerized systems to ensure timely invoices are sent to your clients. If payments are overdue, you can trigger follow-up reminders. Automate recurring invoices for subscription-based services. This reduces the administrative burden and improves your cash flow predictability.

For instance, as soon as an invoice is sent, the system schedules follow-up emails and notifications if payment still needs to be received by the due date.

This automated process ensures that invoices are always on time. It helps minimize payment delays by informing clients and prompting them to settle their bills without requiring manual intervention from the MSP’s team.

For example, TAZ Networks, a Detroit-based MSP, sent invoices manually and could not track past-due payments because they did not have a centralized payment system.

To streamline their invoicing, they moved to a centralized payment platform that allows them to automate invoicing and send reminders for past due payments, enabling them to decrease invoicing time by 30%.

7. Flexible Payment Plans:

Offering your clients different payment options and schedules based on their financial needs will further reinforce your credibility and ensure client retention. This can include monthly, quarterly, or custom intervals, and buy now and pay later.

These plans are essential because they help clients manage their payments more efficiently, reducing late payments and improving cash flow. You can build and retain better client relationships by offering flexible options.

For example, imagine you’re working with enterprise clients who prefer not to pay upfront for your services. To accommodate this, you can offer a flexible payment option through your payment software.

This means your payment software provides the total payment amount upfront, allowing you to deliver your services immediately. In return, your clients can pay over time, guaranteeing you predictable cash flow.

By offering this flexible payment solution, you reinforce your credibility and build stronger relationships with your clients, who are more likely to remain loyal when their financial preferences are accommodated.

8. Regular Updates & Maintenance:

To keep payment systems up to date, you need to update the software regularly with the latest version. This ensures that payment platforms stay efficient and secure by fixing vulnerabilities and adapting to new threats.

According to Statista, counteracting novel security threats (61%) is the second business challenge MSPs face globally.

Keeping software up-to-date is essential because outdated systems are more vulnerable to cyberattacks, which can lead to data breaches and financial losses.

Regular updates address security issues and improve system performance, while audits help spot and fix risks before they become significant problems.

For example, an MSP that updates its payment software with the latest encryption and performs quarterly audits can find and address any weaknesses. This approach improves security, making transactions smoother and boosting client trust. It also helps avoid disruptions and supports long-term business stability.

Ideally, your payment software vendor or provider should do this automatically so you can focus on attracting and servicing your clients.

Conclusion: Leveraging Multiple Payment Choices for MSP Success

This article explained how efficient payment systems are crucial to MSPs. We discussed various payment methods to automate your billing processes and improve cash flow. We explored the strategies you can implement to meet diverse client needs and streamline payment operations.

Diverse payment options and flexible solutions are essential for you to thrive. They keep clients happy with convenience and improve cash flow through automation.

Upgrading to a versatile solution like FlexPoint will significantly enhance your payment management.

FlexPoint is explicitly designed for MSPs and offers robust features that support various payment strategies, such as ACH transfers and credit cards.

MSP Accepting Flexible Financing Payments Using FlexPoint

The first option is flexible financing or Buy Now Pay Later.

FlexPoint gives you access to capital to meet the needs of your enterprise clients who are unable to commit upfront financially.

For instance, Loud & Clear, an Indiana-based MSP, faced challenges when expanding to enterprise-level clients due to cash flow issues and flexible financing.

The large-scale projects required significant upfront costs, which Patrick Kemp, Co-Founder and Director of Operations, found challenging to cover without asking clients for advance payments.

Upon discovering FlexPoint’s working capital solutions, Loud & Clear transformed its financial operations. Partnering with FlexPoint secured consistent cash flow and allowed the company to offer flexible payment terms.

The impact was significant. In just eight months, Loud & Clear saw a 400% revenue increase, processed payments five times faster, and saved thousands in fees and interest.

MSP Accepting ACH Payments Using FlexPoint

Another option available is ACH payments. With FlexPoint’s integrated system, you can automatically invoice clients and receive payments through ACH without manual effort.

SkyCamp Technologies, an Ohio-based MSP that services businesses with up to 75 users, faced several payment challenges and enlisted FlexPoint’s help.

Among these challenges was a lack of integration among the multiple payment processing platforms it needed to address its billing needs.

SkyCamp Technologies' president, Dan Illausky, explained he had to manually process each monthly ACH payment since invoice amounts changed based on customer license counts.

Upon switching to FlexPoint, SkyCamp saved eight hours of work per month. Payments from late clients also became 30% faster, and 20% more clients used AutoPay.

MSP Accepting Credit Card Payments Using FlexPoint

You can also save a lot of money by paying optimal credit card processing fees, using FlexPoint’s level 2 and 3 card data, or avoiding paying fees when you use customer surcharging options.

For instance, Excellent Networks, an El Paso-based MSP providing cybersecurity and desktop services, manually processed credit card payments and faced high processing fees.

This was due to their disjointed payment processing system, which required manual payment handling, increased costs, and was time-consuming.

Mark Luna, the president of Excellent Networks, needed a solution to streamline invoicing and discovered FlexPoint, which simplified their billing operations with its client portal and AutoPay features.

Since using FlexPoint, FlexPoint’s payment portal has saved Excellent Networks over $10,000 annually in credit card fees.

Using FlexPoint as your payment software, your MSP can offer your clients various payment methods without incurring significant fees.

Streamline your MSP payment operations with FlexPoint's tailored solutions. Visit our website to learn more about our adaptable payment systems, or schedule a demo today to see how we can enhance your MSP's efficiency and client satisfaction!