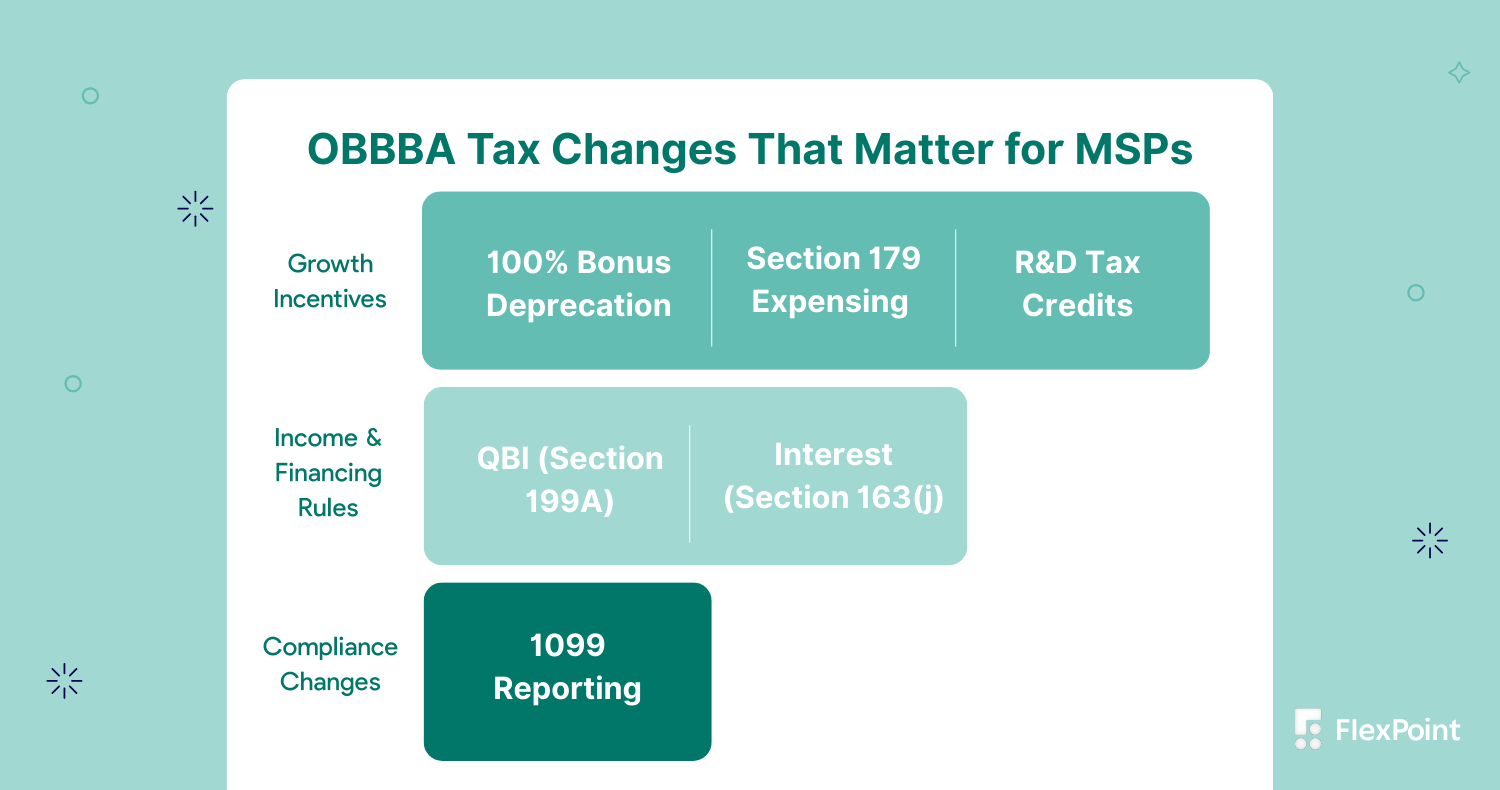

The One Big Beautiful Bill Act (OBBBA) is one of the most consequential tax updates MSPs and IT service firms will face over the next three and a half years. While it builds on earlier Trump-era tax reforms, the OBBBA introduces meaningful changes to depreciation, deductions, reporting requirements, and planning timelines that directly affect how MSPs operate their businesses and (of course) file taxes.

For MSPs, these changes matter more than they might for traditional SMBs. Managed services businesses are both asset-heavy and labor-heavy. They rely on recurring revenue, significant tooling and infrastructure investment, and complex delivery models that don’t always fit neatly into generic tax frameworks. That makes understanding the OBBBA less about theory and more about execution.

In this blog, we break down what the OBBBA is, what changes in 2026, and how MSPs and IT companies should prepare. We’ll also highlight what proactive leaders should be doing now to stay compliant and protect margins.

If you want a walkthrough version of this discussion, we also cover many of these topics in our 2026 Tax Changes Webinar, which dives deeper into MSP-specific scenarios and planning considerations.

What Is the OBBBA and Why MSPs Should Pay Attention

The One Big Beautiful Bill Act (OBBBA) is a continuation and modification of a tax framework introduced under the Tax Cuts and Jobs Act (TCJA). Rather than replacing the TCJA outright, the OBBBA adjusts certain provisions while introducing new compliance and reporting requirements that take effect between 2025 and 2026.

At a high level, the OBBBA affects how businesses:

- Deduct capital investments

- Expense or capitalize research and development

- Claim pass-through deductions

- Deduct interest expense

- Report vendor and contractor payments

For MSPs, the impact is amplified because many of these rules touch everyday operational decisions, such as when to buy hardware, how to structure service agreements, how to compensate owners, and how to finance growth.

As a result, MSP owners and operators, IT consultants, project-based service firms, and SaaS-enabled or hybrid service providers are most significantly impacted by the OBBBA.

What is the OBBBA?

The One Big Beautiful Bill Act (OBBBA) is a federal tax law that builds on prior Trump-era tax reforms, adjusting business deductions, depreciation schedules, and reporting requirements beginning in 2025 and 2026.

OBBBA Timeline at a Glance

The One Big Beautiful Bill Act (OBBBA) was signed into law on July 4, 2025, and its business tax provisions begin to take effect across tax years 2025 and 2026 with some changes being made permanent and others set to end December 31, 2028, with impacts that extend beyond into long-range planning. Understanding the timing of these changes is critical for MSPs that invest in infrastructure, purchase equipment, or rely on deductions that were scheduled to phase out under prior law.

If you need an in-depth timeline with every single date, read this!

January 19, 2025: Bonus Depreciation Cutover

Despite being enacted six months later, one of the earliest effective dates tied to OBBBA occurred on January 19, 2025. For property acquired after this date and placed in service, 100% bonus depreciation is permanently reinstated. Assets acquired after Jan. 19, 2025 generally qualify for full expensing, even under OBBBA’s permanent rules. Assets contracted before that date may still fall under the old phase-down schedule.

December 31, 2025: End of Pre-OBBBA Phase-Down and Section 179 Expansion

Many business tax provisions hinge on the end of the 2025 tax year: Section 179 expensing thresholds increase to a base of $2.5 million (reduced dollar-for-dollar after $4 million of qualifying property), indexed for inflation. If any old energy and other credits were scheduled to expire or phase down at the end of 2025, those phase-outs are now governed by new OBBBA timelines.

January 1, 2026: Rising Importance of 2026 Provisions

While the core OBBBA passed in 2025, tax year 2026 marks the first full year where many of the law’s provisions apply in their final or “new normal” form like QBI deduction (Section 199A) permanence and expanded wage/income phase-ins, business interest expense limits under Section 163(j), and larger 1099 reporting thresholds.

For reporting guidance, you’d see updated IRS guidance for 2026 returns.

Disclaimer: We are not tax professionals. This content is for general informational purposes only. Always consult a licensed tax advisor for guidance specific to your MSP or IT business before making financial decisions.

The timing of the OBBBA provisions matters because asset acquisition timing changes depreciation eligibility and Section 179 limits reset for 2025 and beyond, meaning assets placed in service during 2025 count against higher caps.

Taxes are complex, and with the OBBBA changes, MSPs can either unlock meaningful savings or unintentionally increase their tax liability, so staying informed about how these rules directly affect your operations is critical. We will discuss this more in the next section.

What the OBBBA Means for Business Tax Rules

For better or for worse, the OBBBA reshapes key business tax mechanics that MSPs rely on for planning, investment, and cash flow. At its core, it alters how deductions, depreciation, interest expense, and pass-through benefits are calculated. Of course, these changes are strategic for MSPs and other service-heavy firms that depend on both capital equipment and ongoing labor.

We will have a brief overview and then a deeper dive into these business tax rules and strategies in relation to the OBBBA below.

Business Deductions and Depreciation

Under the OBBBA, bonus depreciation and business interest deductibility are fundamentally different from what they were under the post-TCJA wind-down that was scheduled through 2026. For example, the OBBBA permanently reinstates 100% bonus depreciation on qualifying property acquired and placed in service after January 19, 2025, meaning MSPs that invest in servers, networking equipment, or other depreciable assets can often write off the full cost in the first year rather than spread it out. The old phase-down schedule (80% in 2023, 60% in 2024, 40% in 2025, 20% in 2026) no longer applies for property acquired after January 19, 2025.

For MSP leaders planning infrastructure upgrades or equipment refreshes, this is a big deal: capital expense timing now directly affects taxable income and cash flow more than it would under the old schedule, and if you acted before year-end 2025, you may be able to make a notable difference in year-over-year taxable income.

Interest Deductibility (Section 163(j))

Another major shift relates to the deduction for business interest expense under Internal Revenue Code Section 163(j). Before the OBBBA, the definition of Adjusted Taxable Income (ATI) was based on EBIT (Earnings Before Interest and Taxes), which effectively reduced the amount of interest an MSP could deduct if it had significant depreciation or amortization. The OBBBA permanently restores the EBITDA basis for calculating ATI for tax years beginning after December 31, 2024, allowing businesses to add back depreciation and amortization when determining the limit on interest expense.

For MSPs growing through equipment financing, acquisitions, or leverage, this change can materially increase the amount of interest expense that is deductible, improving cash flow and lowering effective tax burden. But starting in 2026, additional modifications clarify that nearly all business interest, including certain capitalized interest, must be included in the calculation, shifting how aggressive financing strategies are evaluated.

Pass-Through Deductions (QBI / Section 199A)

Before the OBBBA, the Qualified Business Income (QBI) deduction under Section 199A was scheduled to expire after tax years beginning beyond December 31, 2025. The OBBBA makes this deduction permanent for pass-through entities such as S corporations, partnerships, and sole proprietorships, which is particularly relevant for MSP owners structured as pass-throughs.

Importantly, while the final law did not raise the deduction rate to 23% as originally proposed in some House versions, it does expand the income ranges over which the wage and property tests phase in, making the benefit accessible to more business owners at higher income levels. The law also introduces a minimum $400 QBI deduction for taxpayers with $1,000 or more in QBI beginning in 2026.

For MSP owners, this means thoughtful compensation planning and structuring of labor and owner draws are now part of the long-term tax strategy, not just annual optimization.

How the OBBBA Impacts Reporting for MSPs

Under the One Big Beautiful Bill Act (OBBBA), tax reporting rules have shifted in ways that reduce administrative burden but raise the bar on accounting accuracy. It restores the higher 1099-K threshold ($20,000 and 200 transactions), eliminating the widely criticized $600 trigger. Beginning with the 2026 tax year (filed in 2027), it also raises the reporting threshold for Forms 1099-NEC and 1099-MISC from $600 to $2,000. While this reduces the number of forms many MSPs must issue, it does not change tax liability, income is still taxable even if no form is required. Because MSPs rely on a mix of employees, contractors, vendors, and payment platforms, clean, well-organized billing and accounting systems are critical to avoid missed filings, over-reporting, and unnecessary.

Entity Type Differences

It’s important to note before moving on to more in-depth overviews of these changes that entity structure plays a major role here. C-corps, S-corps, partnerships, and sole proprietors all experience the OBBBA rules differently:

- C-corporations: Keep the flat corporate tax rate inherited from TCJA, but now operate with permanent bonus depreciation and restored interest deduction limits, shifting where they invest and when they deduct costs.

- S-corporations and partnerships: Benefit from permanent QBI deductions but must carefully manage wage and capital tests and consider how depreciation and bonus writing affect ATI, interest deductibility, and pass-through taxable income.

- Sole proprietors: Also retain QBI benefits with a guaranteed minimum deduction starting in 2026, but must align personal and business reporting more tightly.

MSPs tend to feel these shifts more acutely because they invest heavily in both people and technology.

100% Bonus Depreciation Under the OBBBA

As mentioned briefly above, bonus depreciation lets a business deduct a large portion of the cost of qualifying assets in the year they are placed into service rather than spreading that cost over multiple tax years. For MSPs, this is important because significant portions of your cost structure are tied up in physical and digital infrastructure that directly support service delivery.

How Bonus Depreciation Changes in 2026

Bonus depreciation lets a business deduct a large portion of the cost of qualifying assets. Under the Tax Cuts and Jobs Act (TCJA), bonus depreciation was phased in at 100% for assets acquired and placed in service through 2022. Originally scheduled to phase down to 80% (2023), 60% (2024), 40% (2025), and 20% (2026), the OBBBA permanently reinstated 100% bonus depreciation for qualified property acquired after January 19, 2025 and placed into service thereafter. This timing rule is critical: taxpayers must have signed a binding contract to purchase the asset before January 20, 2025 to use the old phase-down schedule; otherwise, the new permanent 100% regime applies. Since it is already 2026 by the time I’m writing this, the 100% rule is now fully in action.

That said, the “100%” benefit is subject to specific qualification criteria, including:

- New property only. Used property generally does not qualify unless it meets certain continuity-of-use tests.

- Placed in service test. The asset must be put into service in the tax year for which the deduction is claimed.

- Not listed property subject to special rules. Certain vehicles and luxury items have separate rules that may limit immediate expensing.

Under the old schedule, many MSPs delayed purchases late in the year to accelerate expensing while still capturing a high bonus percentage. With OBBBA’s reinstatement, assets placed into service after the January 19 cutoff generally qualify for full expensing regardless of year, provided the acquisition date and related rules are met. This removes some timing pressure, but it also changes planning dynamics: instead of focusing on squeezing into a prior tax year’s phase-down number, MSPs must evaluate the strategic benefit of accelerating purchases versus preserving cash flow.

What This Means for MSP Capital Investments

For MSP leaders, bonus depreciation under the OBBBA influences several real business decisions:

1. Timing Infrastructure Upgrades

Taking a new asset into service before year-end can generate a large current-year deduction, reducing taxable income when margins matter most.

What you can do: Build depreciation timing into your planning calendar by Q3 each year. Compare the expected tax savings of placing an asset in service in December versus the following March, factoring in cash flow forecasts.

2. Hardware-as-a-Service (HaaS) Models and Bonus Eligibility

HaaS transforms capital purchases into operational expenses for clients, which complicates bonus depreciation for MSPs if the MSP retains title. The key is distinguishing between owned assets (where bonus depreciation applies) and leased or pass-through assets (where it typically doesn’t). This means reconsidering whether certain hardware belongs on the balance sheet.

What you can do: Ensure your HaaS contracts clearly assign ownership and service responsibilities. Clarify whether you or your client owns the hardware at each stage to support proper treatment under bonus depreciation rules.

3. Tradeoffs Between Tax Savings and Cash Preservation

While bonus depreciation can generate significant near-term tax savings, it does not improve cash flow directly. In fact, expensing an asset early can reduce book basis and future depreciation, which means higher taxable income in later years.

What you can do: Run side-by-side scenarios with your tax advisor to compare the present value of full expensing today versus phased depreciation over several years. Prioritize assets where the tax benefit meaningfully improves current-year cash flow.

Section 179 Expensing: What MSPs Can Still Write Off

Section 179 continues to be one of the most flexible and MSP-friendly tax provisions under the OBBBA, particularly for firms that want control over when deductions are taken. Unlike bonus depreciation, which applies automatically to all qualifying assets, Section 179 allows MSPs to elect which assets to expense and how much of each asset to deduct, up to annual limits.

For MSPs, this selective control matters. Eligible Section 179 property typically includes internal-use servers, networking equipment, firewalls, backup appliances, laptops and desktops, and certain off-the-shelf software used for business operations. Because these assets are core to service delivery but not always tied to aggressive expansion, Section 179 often aligns better with practical infrastructure refresh cycles.

Section 179 Limits and Thresholds Under the OBBBA

Under the OBBBA, Section 179 remains in place and continues to be indexed annually for inflation, rather than phased out. While the IRS will publish exact 2026 limits closer to the filing year, current law establishes a framework MSPs should plan around: a maximum deduction cap that adjusts upward each year with inflation, a phase-out threshold that reduces the deduction once total qualifying purchases exceed a set amount, and a taxable income limitation, meaning Section 179 cannot create or increase a net operating loss

In recent tax years, Section 179 caps have exceeded $1 million, with phase-outs beginning once total equipment purchases surpass several million dollars. The key takeaway for MSPs is not the exact dollar amount, but the behavior of the rule: Section 179 rewards moderate, intentional investment and penalizes unchecked asset accumulation.

Section 179 vs. Bonus Depreciation: Key Differences MSPs Should Understand

While both provisions accelerate deductions, they behave very differently in practice.

Bonus depreciation applies broadly and automatically, offering speed but little discretion. Section 179, by contrast, gives MSPs precision. You can expense a firewall but depreciate a server, or fully expense equipment used internally while spreading out assets tied to long-term contracts.

Another critical difference is income dependency. Bonus depreciation can create losses; Section 179 generally cannot. For profitable MSPs that want to reduce taxable income without distorting future years, Section 179 often produces cleaner financial outcomes.

When Section 179 Makes More Sense Than Bonus Depreciation

Because of that, Section 179 is often the better choice for smaller or mid-sized MSPs focused on cash flow stability rather than aggressive tax minimization. It allows leadership to align deductions with actual profitability instead of pulling future deductions forward unnecessarily.

For larger MSPs or PE-backed firms making multi-million-dollar infrastructure investments, bonus depreciation may still dominate due to Section 179 phase-out limits. In those cases, Section 179 often plays a supporting role rather than a primary strategy. As always, it’s best to have these discussions with an MSP-knowledgable tax expert who knows the ins-and-outs of your specific business.

The R&D Tax Credit and OBBBA Changes

Why MSPs Often Qualify for the R&D Credit

Many MSPs underestimate their eligibility for the federal research and development (R&D) tax credit, yet the nature of modern service delivery puts them squarely in the landscape of qualifying activities. The R&D credit is designed to reward companies that innovate within their business, and for MSPs, real qualifying work happens often in the form of internal automation, integration development, custom tooling, and technical problem-solving.

Eligible activities for MSPs and IT businesses typically include things like:

- Custom automation development that streamlines repetitive IT tasks or builds unique operational workflows.

- Systems integrations between core platforms (such as custom PSA to RMM connectors, advanced alert handling, or billing integration with internal tooling).

- Internal tooling and workflow optimization that goes beyond routine maintenance or cosmetic scripting to address technical uncertainty or design challenges.

To qualify under the IRS’s four-part test for R&D credit eligibility, work must seek a technological improvement, involve uncertainty that requires experimentation, and be developed through a process of testing and refinement. Compensation for employees directly engaged in these activities (design, coding, testing, and redesign) often forms the basis for the credit, along with certain contract research expenses.

How the OBBBA Affects R&D Expensing

One of the most impactful parts of the OBBBA for MSPs and other technology-driven businesses is how it changes the underlying treatment of R&D costs themselves, which in turn interacts with eligibility for the R&D tax credit.

Prior to the OBBBA, businesses were required to capitalize and amortize domestic qualified research and experimental (R&E) expenses over five years (15 years for foreign R&E), which delayed deductions and increased taxable income in high-spend years.

With the OBBBA and its introduction of Internal Revenue Code Section 174A, MSPs now have two alternatives for domestic R&E expenditures: immediate expensing and optional amortization. This restoration of immediate expensing improves cash flow timing and reduces taxable income in the year of heavy R&D investment, which can be especially valuable for MSPs investing in automation, internal platform development, or custom integrations tied to service delivery.

Tips for MSPs Claiming the R&D Credit

Because the credit itself is complex and IRS scrutiny is high, documentation is essential. Best practices include:

- Maintain contemporaneous documentation: Keep records of project goals, technical uncertainty, experimentations, trial outcomes, and revisions to demonstrate that work meets the IRS’s four-part R&D credit test.

- Track eligible labor costs separately: With payroll often being a major credit component, logging hours associated with qualifying R&D activities helps substantiate claims.

- Coordinate with your tax advisor: Generic CPAs often overlook technical nuance around software and process innovations; specialists can help integrate Section 174A expensing with R&D credit calculations to maximize benefit while ensuring compliance. Finding the right financial support for you is crucial here.

- File elections carefully: If you claim the gross credit, you must reduce your Section 174A deduction accordingly, or elect the Section 280C(c) reduced credit to avoid that reduction.

For MSPs already investing in internal workflows, automation, custom integrations, and service delivery innovation, the OBBBA’s R&D treatment represents a real opportunity to lower effective tax rates and improve short-term cash flow.

QBI (Section 199A) Deduction: What’s Changing for MSP Owners

The Qualified Business Income (QBI) deduction under Section 199A is a powerful tax benefit for owners of pass-through type businesses, including many MSPs structured as S-corps, partnerships, or sole proprietorships. At its simplest, QBI allows eligible taxpayers to deduct up to 20% of qualified business income from their taxable income. The original Tax Cuts and Jobs Act (TCJA) scheduled this deduction to expire after 2025, but the OBBBA makes it permanent, which can be a meaningful win for MSP owners anticipating higher income tax burdens in 2026 and beyond.

Under the OBBBA, the basic 20% deduction remains, but the rules around income limits and phase-outs have changed. Previously, the wage and capital investment limitations (which reduce or eliminate the deduction for higher-income taxpayers) kicked in over a $50,000 phase-in range for singles and $100,000 for joint filers. The OBBBA expands these ranges to $75,000 and $150,000, respectively, which means more MSP owners with growing income can retain at least part of the QBI deduction.

Another practical change is the introduction of a minimum deduction of $400 for taxpayers with at least $1,000 of QBI from active participation in a qualified trade or business. This helps very small MSPs and side-businesses benefit even if their income is modest.

How the OBBBA Could Reduce or Preserve QBI Benefits

Because the QBI deduction interacts with wage and capital tests, MSP owners should pay close attention to compensation planning and entity structure. For example, S-corp owners who underpay themselves wages may inadvertently reduce their QBI deduction, while those who adjust wages carefully within the safe harbor can maximize their benefit. Likewise, pass-through MSPs with significant capital investment may need to model whether retaining earnings, increasing payroll, or re-allocating compensation yields a better QBI outcome. Planning these details now can preserve a deduction that will matter for 2026 returns and beyond.

Business Interest Limitation (Section 163(j)) and MSP Financing

Section 163(j) limits how much business interest expense a company can deduct in a given year, traditionally capping the deduction at 30% of adjusted taxable income (ATI). Under post-TCJA rules from 2021 onward, ATI was calculated after depreciation and amortization were deducted (an EBIT basis), which often constricted deductions for companies making heavy capital investments.

The OBBBA reinstates the more generous EBITDA basis. This change generally increases the amount of interest expense MSPs can deduct, which directly affects leveraged growth strategies such as equipment financing, acquisitions, or private-equity-backed expansion.

However, beginning in tax years after December 31, 2025, the law also excludes certain types of income (like Subpart F income and GILTI inclusions) from ATI for purposes of the interest limitation calculation. These refinements mean larger or internationally engaged MSPs will need to coordinate taxable income sources carefully when planning financing.

What This Means for MSP Growth Strategies

For MSPs pursuing aggressive growth, the biggest practical takeaway is that interest expense treatment now requires closer alignment between tax planning and cash-flow forecasting. A loan taken to finance a data center refresh or an acquisition no longer carries as heavy a tax cost as it would under the old EBIT regime, but it still needs to be planned to avoid surprises in taxable income and interest deductibility. (This underscores why MSPs with debt should integrate tax modeling into their broader financial planning rather than treating financing as a separate operational decision.)

A few specific examples would be:

Equipment financing: Loans for servers, networking gear, or data center upgrades now interact differently with interest deductibility, so MSPs should model timing and placement to optimize tax impact.

M&A and PE-backed MSPs: Acquisitions and private equity-backed growth must account for OBBBA interest limits when structuring deals to avoid unexpected taxable income spikes.

1099 Reporting Changes MSPs Need to Prepare For

The OBBBA revises key informational reporting thresholds that affect how businesses report payments to vendors, contractors, and service providers. Perhaps the most visible change is the increase in reporting thresholds for Forms 1099-MISC and 1099-NEC from $600 to $2,000, starting for tax year 2026. In other words, payments under $2,000 generally no longer trigger automatic 1099 reporting on those forms, reducing administrative burden for many recurring smaller payments.

Simultaneously, the OBBBA restores the prior Form 1099-K reporting threshold of $20,000 and 200 transactions, reversing the lower thresholds implemented in recent years. This change affects payment processors and third-party settlement organizations, meaning many MSPs and vendors will see fewer 1099-K forms for small-transaction business payments.

How to Stay Compliant in 2026 with OBBBA 1099 Reporting Changes

Staying compliant into 2026 requires MSPs to ensure their accounting and payroll systems can accommodate the updated thresholds and automate much of the tracking. Without strong system integration, MSPs risk either missing required reports or over-reporting unnecessarily, both of which create administrative drag and potential IRS notices.

MSPs need accounting and payroll systems that are fully prepared to handle the updated 1099 thresholds. This means:

- Accounting System Readiness: Ensure your general ledger, billing, and payroll systems can track payments to contractors, vendors, and service providers by type and amount, including separating payments that cross the new $2,000 and $20,000 reporting thresholds.

- Automation and Reporting Best Practices: Automate 1099 generation, reconciliation, and filing wherever possible to reduce errors, prevent missed reports, and maintain an audit-ready trail, while aligning reporting with operational and billing data.

One of the most important steps you can take, though, is to hire an accounting expert with specific MSP knowledge to help you stay compliant.

Key Takeaways: How MSPs Should Prepare for OBBBA Tax Changes

The MSPs that come out ahead under the OBBBA will be the ones that treat it as a full year strategy, not a year-end accounting problem. These changes directly affect how and when MSPs invest in infrastructure, compensate owners, finance growth, and report activity. Waiting too long for any of these will limit options and likely lock in higher tax exposure.

For MSPs and IT service providers, the most important actions to take now include:

- Pressure-testing capital investment timing, especially for servers, networking gear, and internal tooling, to determine whether purchases should be accelerated, deferred, or restructured under changing depreciation rules

- Reevaluating entity structure and owner compensation, particularly for S-corps and partnerships where QBI eligibility, W-2 wages, and distributions directly affect deductions

- Reviewing financing strategies for equipment, acquisitions, or PE-backed growth in light of updated interest deductibility calculations

- Ensuring accounting and billing systems can support accurate reporting, deferred revenue tracking, and 1099 compliance as reporting thresholds and rules evolve

- Resisting reactive year-end behavior, such as last-minute asset purchases made purely for deductions without considering cash flow, amortization, or long-term margin impact

Common mistakes we see MSPs make include over-relying on prior-year tax strategies, failing to coordinate tax planning with operational decisions, and treating tax optimization as separate from billing, forecasting, and financial reporting. Under the OBBBA, those silos create real financial risk.

For a tactical, MSP-specific breakdown of what to review and when, our 2026 Tax Prep Checklist walks through the exact decisions MSP leaders should be making before year-end so tax strategy supports growth instead of reacting to it.

Final Thoughts: Planning Ahead for 2026 and Beyond

The OBBBA makes one thing clear: your tax results are determined long before you file. For MSP leaders, every operational decision can directly impact deductions, depreciation, and cash flow. Waiting until year-end to react is a missed opportunity.

Winning under the OBBBA requires more than this technical knowledge, though, it requires alignment. That means working with a tax advisor who understands MSP-specific realities like pass-through income, Section 179 and bonus depreciation, and R&D credits, while also maintaining clean, integrated financial systems where billing, expenses, and deferred revenue accurately reflect how the business operates. When cash flow, accounting, and tax strategy work together, MSPs can plan confidently, reduce surprises, and invest for growth without disrupting financial stability.