The One Big Beautiful Bill Act (OBBBA) isn’t a one-time tax change MSPs can deal with and move on from. It’s a multi-year shift in how business taxes work, with provisions rolling out through 2025 and 2028 that affect deductions, depreciation, reporting, and long-term planning.

For MSP owners and IT service providers, knowing what the law changes is only half the equation. Knowing when those changes take effect is what determines whether your tax strategy actually works. You may have the best intentions in how you manage cash flow, investing in equipment, and structuring your entity and compensation, but timing is what makes those efforts effective or not.

Unlike the short-lived tax updates many businesses are used to, the OBBBA functions as a long-range planning framework. Decisions made in 2026 won’t just affect one filing season, they will shape tax outcomes years down the line.

In the sections below, we’ll walk through the key dates in the OBBBA timeline and explain why each one matters for MSP tax planning.

Why the OBBBA Timeline Matters for MSP Tax Planning

The One Big Beautiful Bill Act (OBBBA) is a sweeping U.S. tax law signed in July 2025 that fundamentally reshapes business taxes, deductions, depreciation rules, and reporting requirements.

For MSPs, IT service providers, and other service-based companies, it’s not enough to know what the law changes; the timing of each provision is equally crucial. When a deduction, depreciation rule, or reporting requirement takes effect determines how you plan cash flow, capital investments, and overall business strategy. A misaligned timing decision can reduce available deductions, trigger higher estimated taxes, or complicate compliance workflows.

Specifically, timing under the OBBBA directly impacts:

- Cash flow and estimated taxes: When deductions and credits apply affects quarterly payments and liquidity.

- Capital expenditures and depreciation strategy: The difference between a 2025 or 2026 asset purchase can dramatically change write-offs.

- Entity structure and owner compensation: Timing influences S-corp distributions, pass-through QBI benefits, and long-term succession planning.

- Compliance and reporting workflows: Payroll, 1099s, and accounting systems must align with when rules are active to avoid costly errors.

Knowing the timeline lets MSPs make proactive decisions, rather than react to filing deadlines or last-minute IRS guidance.

What Is the OBBBA Timeline?

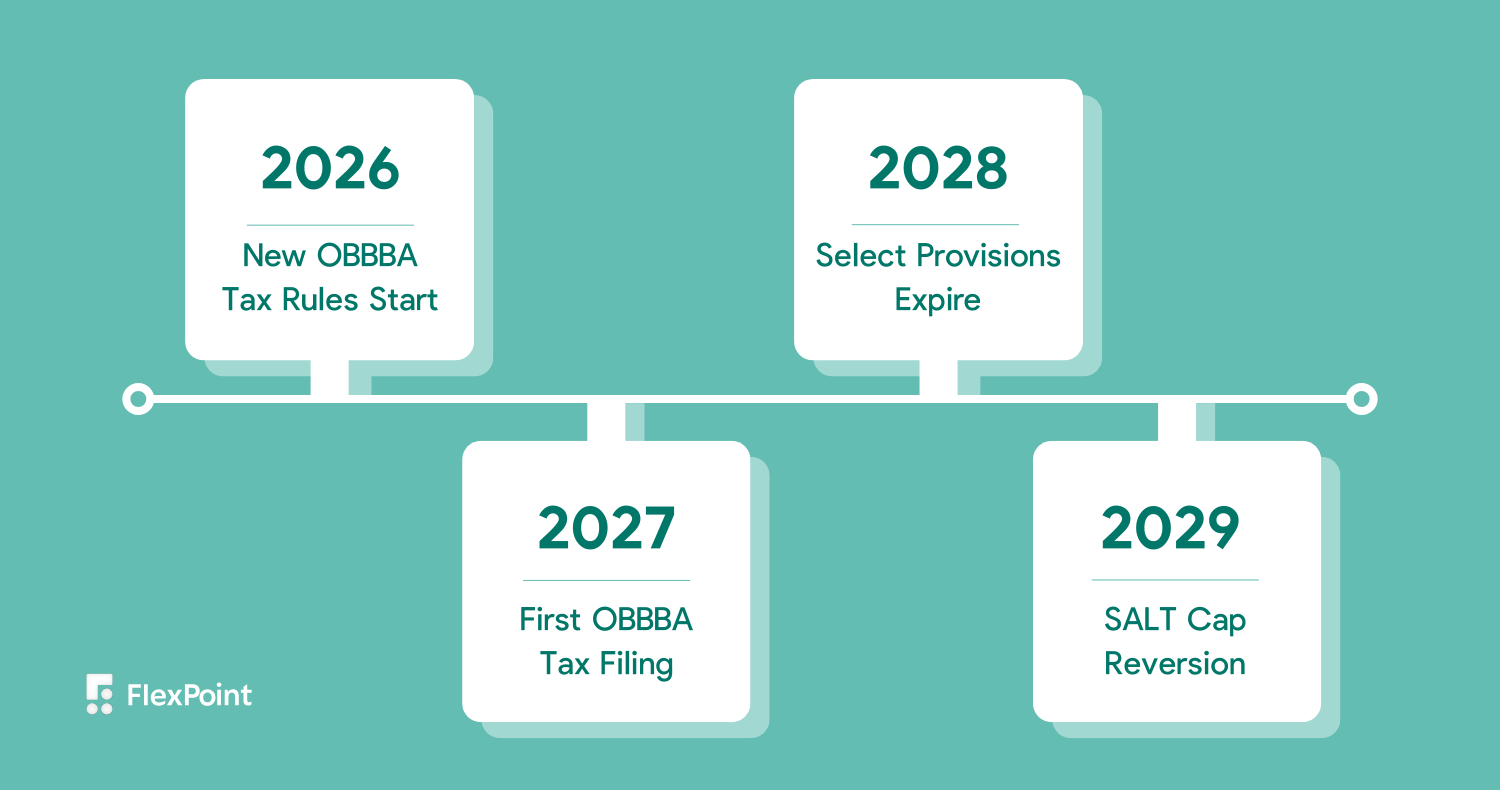

The OBBBA timeline is the schedule for when key provisions of the One Big Beautiful Bill Act take effect from 2025 through 2029, including business deductions, depreciation, QBI rules, and the SALT deduction cap. While enacted in 2025, the first tax year it affects is 2026 with certain provisions going away after that.

July 4, 2025: OBBBA Signed Into Law

The OBBBA officially became law on July 4, 2025, codified as Public Law 119‑21. While most MSP tax returns weren’t immediately affected, this date set the stage for all future effective dates, IRS guidance, and planning deadlines.

For MSPs, this was less about immediate action and more about preparing for what’s coming like updating accounting systems, consulting advisors, and starting to model the impact of the law. In practical terms, July 4, 2025, marked the beginning of a multi-year planning timeline that businesses could no longer ignore.

January 1, 2026: Major OBBBA Tax Changes Take Effect

This is the first real pit stop on the timeline: most of the OBBBA’s business tax changes apply to tax years starting after December 31, 2025. For MSPs, that means the 2026 tax year (filed in 2027) is your first test. Key provisions include:

- 100% Bonus Depreciation restored for qualified property placed in service after January 19, 2025. This lets businesses deduct the full cost of qualifying equipment and tech in the year it’s placed in service, a major timing lever for MSPs making capital purchases.

- Section 179 Expensing limits increased, allowing more upfront deductions for qualifying assets.

- Qualified Business Income (QBI; Section 199A) deduction made permanent and enhanced, giving long‑term stability to a key pass‑through deduction many MSPs rely on.

- State and Local Tax (SALT) deduction cap temporarily increases to around $40,000, indexed annually through 2029.

- Depreciation and R&D expensing revisions that strengthen business investment incentives.

If you’d like to know more about these changes and how they impact your business, read How the OBBBA Impacts MSPs & IT Companies in 2026.

This is a major reset for MSPs and IT businesses, not just a rule revision, because your 2026 estimated taxes, depreciation decisions, and asset timing all directly affect the outcomes reported on your first tax return under the new law, making it critical to align asset purchases, bookkeeping methods, and entity and compensation strategies from the outset.

Throughout 2026: Operational and Reporting Adjustments

While 2026 doesn’t come with one dramatic “circle this on the calendar” deadline, it is arguably the most important implementation year of the OBBBA timeline. This is the year where strategy turns into execution. The tax law is live, deductions are real, and the way MSPs track money, assets, and vendors starts to materially affect future tax outcomes. And applying what you used to know about tax law here can cause major consequences for your return.

For MSPs, 2026 is less about filing and more about building the infrastructure that makes filing accurate, defensible, and optimized when returns are submitted in 2027 (and for the years beyond).

What MSPs Should Update During 2026

In 2026, MSPs need to make key updates to ensure the OBBBA changes are correctly applied.

- Accounting and AR systems: Update for 100% bonus depreciation and expanded Section 179 rules, making sure assets like hardware, internal tools, and infrastructure are properly classified and placement-in-service dates are tracked.

- Vendor and contractor reporting: Review 1099 workflows and vendor classification to ensure accurate, consistent reporting, especially for subcontractors and third-party specialists.

- Documentation practices: Keep clear records supporting all deductions and credits, including depreciation schedules and R&D-related activities, so filings are accurate and defensible.I f you need help cleaning up your books with a finance expert in the MSP space, use our accounting guide to get ahead of the curve.

By focusing on these areas, MSPs set themselves up for a smooth first OBBBA-era filing in 2027 and reduce the risk of missed deductions or compliance issues.

Key IRS Guidance and Updates MSPs Should Track

Throughout late 2025 and into early 2026, the IRS is expected to issue transitional relief notices and implementation clarifications tied to the OBBBA. These typically answer practical questions the statute itself doesn’t fully resolve, such as how certain rules apply to service businesses or how transitional years should be treated.

For MSPs, this guidance directly affects how 2026 activity is recorded. Decisions made during this year flow straight into 2026 tax returns filed in 2027, making it essential to stay informed and adjust processes as clarity emerges.

Disclaimer: We are not tax professionals. This content is for general informational purposes only. Always consult a licensed tax advisor for guidance specific to your MSP or IT business before making financial decisions.

April 15, 2027: First Tax Filing Under OBBBA 2026 Rules

April 15, 2027 marks the first major filing milestone under the OBBBA for most MSPs. S-corps, LLCs, and partnerships will file their 2026 returns (extensions aside), and for the first time, the real financial impact of the new law becomes visible on paper. For example, an MSP that upgraded servers, networking equipment, or internal IT tools in early 2026 may be able to fully expense those purchases under 100% bonus depreciation, reducing taxable income far more than in prior years. That same MSP might also see a larger QBI deduction applied to pass-through income and a higher SALT deduction flowing through to the owners’ personal returns, changing both the business’s tax liability and the owners’ cash flow at the same time.

This is when MSPs experience the cash-flow effects of updated depreciation rules, see permanent or extended QBI benefits reflected in actual tax liability, and apply the expanded SALT deduction in practice rather than theory. For many service businesses, this filing season will feel different, not necessarily because the forms changed, but because the outcomes did.

The most important planning insight here is simple but often overlooked: the numbers reported in 2027 are largely the result of decisions made in 2025 and 2026. Asset purchases, compensation structures, bookkeeping discipline, and timing choices all converge at this point. Filing season reaps what was sewn all year.

January 1, 2027: Secondary OBBBA Provisions Phase In

Not all OBBBA provisions move on the same schedule. Beginning January 1, 2027, a secondary set of rules starts to phase in, many of which matter more at the owner level than in daily MSP operations.

One notable shift is the inflation indexing of estate and gift tax exemption amounts. For MSP owners thinking about long-term succession, partial exits, or eventual sales, this adjustment influences how ownership transitions can be structured over time.

In addition to wealth-transfer rules, the OBBBA updates certain employee benefit provisions that begin to shift around this period. Employer-provided student loan repayment assistance, which was made permanent by the OBBBA, will have its annual exclusion amount indexed for inflation beginning in 2026, meaning the value of that tax-free benefit grows over time rather than staying frozen at a historic limit. Employers and MSP owners who offer or plan to offer benefits such as this should factor in these adjustments when designing compensation packages, these inflation-indexed incentives affect total taxable compensation and future payroll tax planning.

New Opportunity Zone designations and characteristics also become active during this phase. While this won’t affect most MSPs’ day-to-day operations, it can matter for owners with broader investment, real estate, or expansion strategies. Opportunity Zones can influence where owners choose to reinvest capital gains, open secondary offices, or structure long-term investments tied to business growth, making them another consideration in owner-level planning beginning in 2027.

The key takeaway is that these changes don’t typically disrupt operations, but they do quietly shape long-term planning decisions, especially for owners with growth, exit, or legacy goals.

2027–2028: MSP Optimization Window

Once the first OBBBA-era return is filed, MSPs move out of transition mode and into what can best be described as an optimization phase. At this point, the rules are no longer theoretical. Businesses have real tax returns, real cash-flow outcomes, and real data showing how the OBBBA actually impacts their bottom line.

This is the window to evaluate whether an existing entity structure is still performing as expected under the updated and now-durable QBI rules. An MSP operating as an S-corp may discover that reasonable compensation levels or profit distributions should be adjusted to better align with QBI eligibility based on how the deduction played out on the first return.

It’s also an ideal time to rebalance capital expenditures. With bonus depreciation and Section 179 expensing rules stabilized, MSPs can be more intentional about when they purchase servers, networking equipment, internal tools, or other qualifying assets. Instead of rushing purchases into a single year out of fear that deductions will disappear, businesses can plan multi-year investment cycles with more certainty.

Cash-flow forecasting deserves renewed attention during this period as well. Adjustments to AR processes, billing cadence, and estimated tax calculations can significantly reduce underpayment penalties or year-end surprises. Many MSPs find that after their first OBBBA filing, prior assumptions about quarterly estimates or owner distributions no longer hold up.

There are fewer hard deadlines during 2027 and 2028, but that’s exactly what makes these years valuable. MSPs that use this time to fine-tune structure, spending, and forecasting tend to operate from a position of control rather than reaction, setting themselves up for stronger outcomes as the next phases of the OBBBA approaches.

December 31, 2028: Select Temporary Provisions Expire

By the end of 2028, several temporary or individual-focused provisions under the OBBBA are scheduled to sunset or change. While many of the core business reforms (like permanent QBI and bonus depreciation) remain in place, these temporary perks are tied to individual tax roles and benefits that historically influence personal cash flow, retirement timing, and owner-level compensation decisions.

Examples include:

- Enhanced standard deduction and senior additional deduction windows: for taxpayers age 65 and older, certain expanded deduction allowances are set with phased indexing and sunset timelines that realign after 2028. These benefit packages don’t apply directly to business income but can affect an owner’s personal tax picture, especially in high-income years.

- Temporary individual credits and deductions that were extended or expanded under OBBBA (for instance, expanded child tax credit amounts or senior add-on deductions) are generally tied to the 2025–2028 window, after which they return to pre-OBBBA norms unless further law changes occur.

- Individual tax incentives such as overtime and tipped wages deductions are available through 2028 only; beyond that, these wage-related deductions expire.

While most of these provisions don’t affect day-to-day MSP operations, they indirectly influence owners’ personal tax exposure and cash flow, which in turn can affect decisions around profit distributions, salaries, retirement contributions, and investment planning. For example:

- An MSP owner nearing retirement might structure compensation to take advantage of higher deduction windows before 2029.

- Higher temporary credits on personal returns might influence whether an owner accelerates or delays certain income.

- Changes to individual deduction thresholds can shift marginal tax rates, which affect net take-home cash and how aggressively the business funds retirement plans or profit-sharing arrangements.

Smart MSP planning spots these sunsets early, rather than rediscovering them during tax season. Knowing which benefits are scheduled to disappear (and when) allows owners to act while opportunities are still available, whether that’s accelerating certain income, timing distributions, or locking in favorable personal tax positions before the end of 2028.

January 1, 2029: SALT Cap Reversion and Key Phase-Outs

January 1, 2029 is a significant long-term date for service companies. The temporary increase to the State and Local Tax (SALT) deduction cap, which allowed taxpayers to deduct roughly $40,000 during the OBBBA window, is scheduled to expire and revert closer to its previous $10,000 level. For MSP owners in high-tax states like California, New York, or New Jersey, this is significant: the higher cap provided an opportunity to reduce both business and personal tax liability, and the reversion may meaningfully increase taxable income if not planned for in advance.

In addition, other temporary credits and bonus expensing provisions that applied under OBBBA will begin phasing out around this year. Bonus depreciation on certain types of property and temporary energy or R&D credits may begin returning to pre-OBBBA thresholds or sunset entirely, making 2029 a natural “cutoff” for several tax-sensitive strategies.

For MSPs, the implication is clear: any strategy that relies on the elevated SALT cap, accelerated depreciation, or temporary credits should be executed before 2029. Owner-level modeling becomes essential, especially for businesses with substantial pass-through income. Decisions about owner compensation, profit distributions, and even timing of capital expenditures should take this date into account to lock in benefits while they still exist. Without proactive planning, owners could face higher tax bills or miss out on deductions they could have claimed with minimal adjustments.

Beyond 2029: Long-Term MSP Tax Strategy Horizon

After 2029, the OBBBA largely settles into its long-term posture. While most core business reforms like permanent QBI deductions, Section 179 expensing, and established bonus depreciation rules remain in place, MSPs should continue monitoring:

- Future tax reform cycles, which could adjust rates, deductions, or credits.

- Inflation indexing effects on key thresholds, including QBI limits, estate and gift tax exemptions, and Section 179 caps.

- IRS guidance and court interpretations, which may refine how the OBBBA is applied in practice, particularly for pass-through entities.

At this stage, tax strategy shifts from short-term compliance to longer-term business planning. MSPs can use the stability of a largely settled law to make decisions about scaling operations, pursuing mergers and acquisitions, and planning exits or succession. An MSP owner evaluating whether to reinvest profits into a second location or sell the business can model outcomes more confidently, knowing that the major OBBBA changes have already been absorbed and most temporary provisions have expired.

The multi-year framework created by the OBBBA gives MSPs a rare advantage: fewer moving pieces to manage, and a clear horizon for strategic growth and personal tax planning. Properly aligned, this clarity lets MSPs make investment, compensation, and expansion decisions with confidence, rather than reacting each year to sudden legislative shifts.

How MSPs Should Use This OBBBA Timeline

The true value of the OBBBA timeline comes from actively using it as a multi-year planning tool. Each stage of the timeline shapes decisions that directly affect your business. Missing or skipping a step can create ripple effects, from higher estimated taxes to lost deductions or mis-timed capital expenditures.

Here’s a practical way to approach it:

- Now: This is the preparation phase. MSPs should ensure accounting and AR systems are ready for the new rules, consult trusted tax advisors, and model how 2026 changes could impact cash flow, depreciation schedules, and QBI deductions. Even small adjustments made now can have outsized effects.

- Early 2026: Implementation year. This is when the law starts to take effect, so accurate record-keeping and strong documentation are critical. Track every qualifying purchase, update 1099 and vendor reporting processes, and confirm that bookkeeping reflects the new depreciation and expensing rules. The better the data collected in 2026, the fewer surprises you’ll face in your first OBBBA-era filing.

- Early 2027: Filing and review. Submit 2026 returns and use the results to revisit projections. Compare actual QBI deductions, SALT deductions, and bonus depreciation benefits against your models. This is also a good time to evaluate whether entity structure or compensation strategies need adjustment based on the first full year under OBBBA rules.

- 2027–2028: Optimization window. Now that the first OBBBA return is filed, MSPs can refine strategies. Rebalance capital expenditures to maximize depreciation benefits, review AR processes and billing cadence, and make adjustments to estimated taxes to reduce cash-flow surprises.

- Before 2029: Execute SALT-sensitive strategies and lock in deductions. With the temporary SALT cap set to revert, any planning that relies on the higher $40,000 threshold must be completed before 2029. Similarly, review any remaining temporary credits or expensing opportunities that could affect 2028 filings, and ensure owner-level tax planning aligns with these deadlines.

Each phase builds on the previous one, creating a layered, cumulative planning approach. Skipping steps or waiting until filing season can leave MSPs paying more taxes than necessary or missing key deductions entirely.

Conclusion: The OBBBA Timeline Is a Multi-Year Tax Roadmap

The OBBBA is a strategic framework that unfolds over several years. For MSP owners, the difference between reacting at tax time and planning proactively can mean thousands (or even tens of thousands) of dollars in deductions, credits, and cash-flow advantages.

Understanding the timeline allows you to see the dominoes before they fall. Every asset purchase, owner distribution, or change to your entity structure made in 2025 or 2026 affects what you report in 2027. Similarly, decisions in 2027 and 2028 shape the opportunities available before the SALT cap reverts and temporary provisions expire in 2029. Working with this roadmap, rather than against it, transforms compliance from a yearly scramble into continuous, predictable planning.

For service providers, this clarity translates into more than just avoiding errors, it enables smarter cash-flow management, optimized capital spending, and long-term flexibility. Coordinating with tax professionals who specialize in service company strategy isn’t optional under the OBBBA; it’s a key part of running a healthy, scalable business that can grow, adapt, and plan exits confidently.

By understanding the OBBBA timeline and planning proactively, MSPs can take control of cash flow, deductions, and long-term strategy instead of reacting at filing time. To make it even easier, you can follow along with our 2026 Tax Prep Checklist for MSPs, which walks through the key steps to align your assets with these multi-year changes. Using this, you make decisions on your own terms, not the IRS’s.