The One Big Beautiful Bill Act (OBBBA) reshapes how business tax planning works, but one provision stands out for MSPs more than almost any other: the return of 100% bonus depreciation.

For IT service providers and MSPs, capital investments aren’t occasional. Servers, networking gear, endpoints, and internal infrastructure play a central part in the operation. Under the OBBBA, how and when those purchases are made can materially change cash flow, estimated taxes, and long-term planning.

The headline change is straightforward: qualifying assets can now be fully expensed in the year they’re placed in service. The real impact, however, is anything but simple. Timing, asset structure, and cross‑team coordination between finance, tax, and operations have never mattered more.

This blog breaks down what bonus depreciation is, how it changed under the OBBBA, and how MSPs should think about using it strategically heading into 2026.

What Is Bonus Depreciation?

Bonus depreciation allows businesses to deduct a large percentage, now 100% under the OBBBA, of the cost of qualifying assets in the year those assets are placed in service.

Under traditional depreciation, assets are written off gradually over several years. Bonus depreciation accelerates that deduction, pulling future tax benefits into the present. Instead of spreading a server purchase across five years, an MSP can expense the full cost immediately.

Under the OBBBA, this immediate expensing is no longer phased out year by year. It’s restored and extended, creating a clearer planning runway for service businesses, which is a huge leg up for growing MSPs and IT businesses.

What is Bonus Depreciation Under the OBBBA?

Bonus depreciation under the OBBBA allows MSPs to fully expense qualifying assets in the year they’re placed in service.

Why Bonus Depreciation Is Especially Relevant for MSPs

Bonus depreciation applies to many industries, but MSPs feel its impact more directly because of how they’re built. Unlike firms that rely primarily on labor, MSPs deliver services through physical and digital infrastructure. Despite that difference seeming small, it matters under the tax code.

Most MSPs share three defining characteristics that make 100% bonus depreciation especially relevant:

- An asset-heavy delivery model: Servers, networking gear, endpoints, and internal tools are core to service delivery, not optional overhead.

- Ongoing infrastructure refresh cycles: Hardware ages out on a schedule driven by security, performance, and vendor support, not tax timing.

- Hardware purchases tied directly to client growth: New clients, expanded contracts, and higher SLAs often require immediate capital investment.

Technology refreshes aren’t a luxury; they’re a business necessity. Servers age, firewalls must be replaced, and endpoints multiply as your team and client base grow. These are inevitable costs of doing business, but they’re ones that, under 100% bonus depreciation, MSPs can turn into meaningful financial flexibility.

What bonus depreciation does under the OBBBA is change how those unavoidable costs hit your financials. Rather than letting asset write‑offs trickle out over years, MSPs can front‑load tax benefits and turn big infrastructure outlays into a strategic tool.

When used intentionally, 100% bonus depreciation can:

- Reduce the after‑tax cost of infrastructure upgrades: Immediate first‑year expensing lowers taxable income when you make capital purchases, meaning you pay less in taxes up front and improve the present value of your investments.

- Smooth cash flow during growth years when CapEx spikes: By front‑loading deductions in the year assets are placed in service, bonus depreciation can immediately reduce tax liability and free up cash flow to reinvest in growth.

- Support aggressive expansion without creating surprise tax bills later: Accelerating cost recovery allows MSPs to recover capital costs sooner, which can make it easier to budget for expansion and avoid large tax bills that might otherwise materialize when depreciable basis is still being recovered over time.

For MSPs, it’s less like a tax perk and more like better shock absorption for a business that grows in bursts.

What Assets Qualify for Bonus Depreciation Under the OBBBA?

Now that we’ve established the relevance of 100% bonus depreciation for your business, it’s important to get specific about what and how it applies.

Top MSP Assets That Typically Qualify

Most of the equipment MSPs purchase in the normal course of business qualifies for bonus depreciation, assuming it meets standard recovery period and use requirements. Common examples include:

- Servers and storage infrastructure

- Networking equipment such as firewalls, switches, and routers

- Laptops, desktops, and endpoint devices

- Certain technology equipment and software, when structured correctly

In practice, core infrastructure is usually straightforward. Where things get more nuanced is with bundled solutions, cloud-adjacent tools, or software tied to long-term contracts. That’s where classification and documentation matter.

New vs. Used Assets: What MSPs Should Know

One of the most persistent misconceptions is that assets must be brand new. Under bonus depreciation rules, assets must be new to you, not new to the market.

That distinction opens the door for acquired assets from another business, equipment obtained through buyouts or refresh agreements, assets included in acquisitions, or internal reorganizations!

What matters is ownership and when the asset is placed in service. This becomes especially relevant for MSPs acquiring client contracts, internal tools, or even other service providers, where infrastructure changes hands as part of a broader transaction. The key cutoff is January 19, 2025. If your assets were placed in service after that date, they may qualify for 100% bonus depreciation. For many MSPs reading this in January of 2026, that means last year’s investments are already in play as tax filing season begins. If you want to know more about the timelines relevant to the OBBBA, including when the temporary provisions are being phased out, read more in our OBBBA Timeline: Key Dates MSPs Need to Know blog.

How 100% Bonus Depreciation Changes Under the OBBBA

Bonus depreciation isn’t new (MSPs have been using it for years), but the recent changes make it especially important to confirm eligibility and timing before you file.

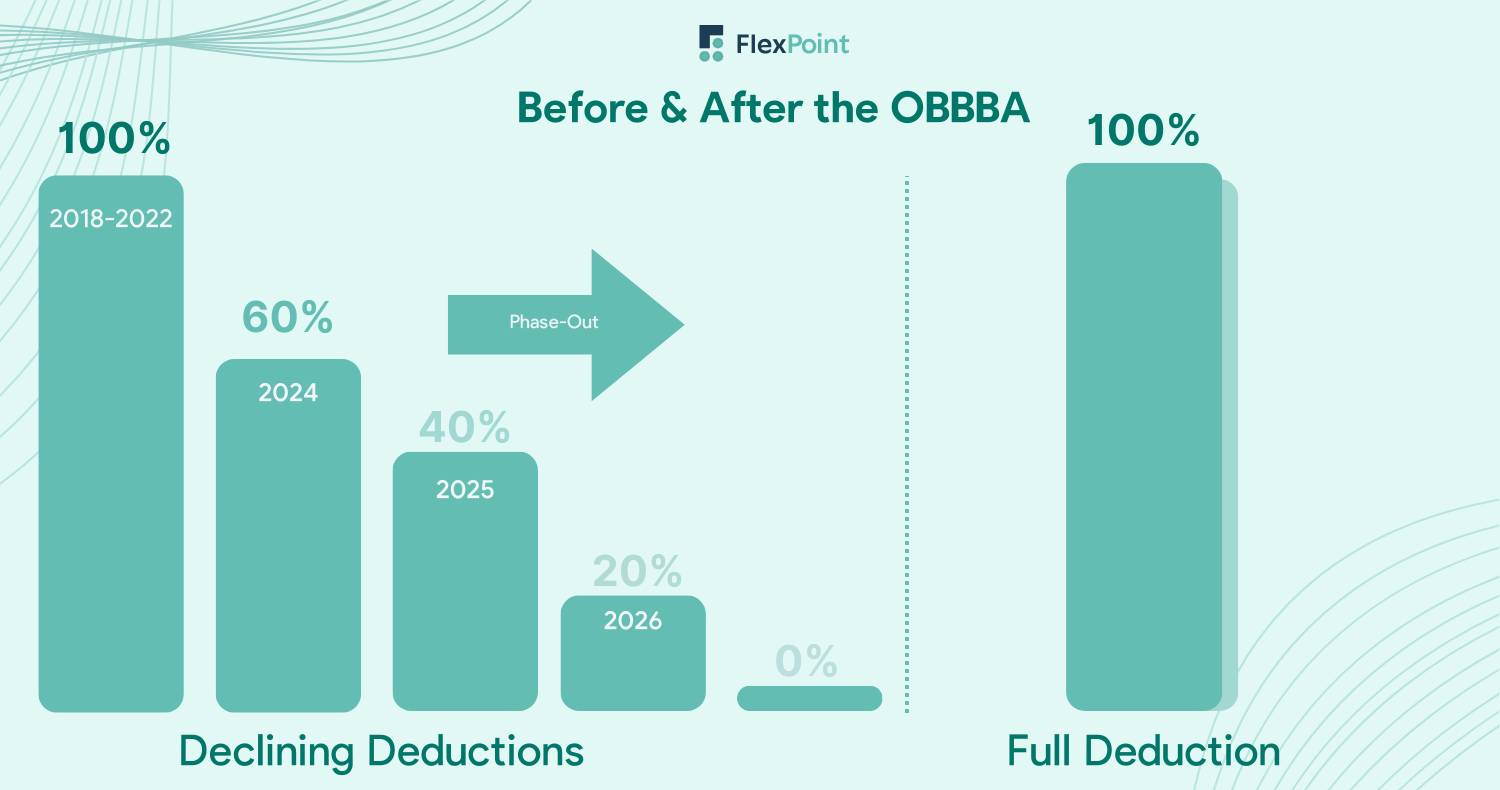

Bonus Depreciation Before the OBBBA

Before the OBBBA, bonus depreciation followed a scheduled phase-out established under the Tax Cuts and Jobs Act of 2017 (TCJA). While the TCJA initially allowed 100% bonus depreciation, it also hard-coded a gradual reduction that began in 2023. Each year, the allowable percentage declined, turning routine infrastructure planning into a moving target for MSPs.

For example, a $200,000 infrastructure refresh placed in service in 2024 qualified for just 60% bonus depreciation, with the remaining cost spread over future years. The same purchase made a year later was scheduled to qualify for only 40%. Nothing about the technology changed, just the tax math.

That reality forced MSPs to ask increasingly tactical questions as they scaled:

- Should purchases be accelerated before the next drop?

- Should upgrades be delayed and depreciated over time?

- Should Section 179 be used instead, and if so, on which assets?

For MSPs planning multi-year infrastructure investments, the rules kept shifting underfoot. That uncertainty made long-range planning much more complex and pushed many MSPs into reactive, calendar-driven decisions rather than choices based on operational needs, security posture, or growth strategy.

100% Bonus Depreciation Under the OBBBA (2026 and Beyond)

As noted earlier, the OBBBA permanently restores 100% bonus depreciation, reversing the uncertainty baked into the TCJA phase-down and bringing clarity back to capital planning. For qualifying assets, the rules are now straightforward:

- Assets must be acquired and placed in service after January 19, 2025

- The change applies to taxable years beginning after December 31, 2025

- Qualifying assets are fully deductible in the year they’re placed in service, unless the MSP elects out

The contrast matters. Under the old rules, an MSP planning a $200,000 infrastructure refresh had to weigh whether buying in 2024 (60% bonus depreciation), waiting until 2025 (40%), or delaying further would materially change the tax outcome. Under the OBBBA, that same MSP can plan a refresh in 2026 or 2027 and know (before a single PO is issued) that the full cost will be deductible in the year the equipment is placed in service.

For MSPs, this restores something more valuable than a deduction: predictability. Infrastructure investments can now be planned around operational needs, security requirements, and growth timelines without worrying that the tax benefit will quietly shrink year over year.

Phase-Down Rules MSPs Should Still Watch

Even though the OBBBA permanently restores 100% bonus depreciation for qualifying assets acquired and placed in service after January 19, 2025, MSPs shouldn’t treat tax planning as “set it and forget it.” Some rules are now permanent, but others still hinge on contract timing, asset structure, and interactions with other tax provisions.

Here are the key exceptions MSPs still need to watch and why they matter:

1. Older contracts can still fall under the TCJA phase-down

If your MSP signed a binding contract before January 20, 2025, those assets may still be subject to the old TCJA phase-down (40% in 2025, 20% in 2026, 0% in 2027), even if the equipment goes live later. In other words, a server you expected to fully expense could end up only partially deductible based purely on contract timing.

2. Section 179 and bonus depreciation don’t always stack cleanly

Bonus depreciation has no dollar limit, but Section 179 still does ($2.5M deduction with a $4M phase-out in 2025, indexed). How you combine (or choose between) the two can materially change your taxable income. Ignoring the interaction often means leaving deductions on the table. =

3. Big deductions can affect QBI and create NOL timing issues

Even with the QBI deduction now permanent, large bonus depreciation deductions can reduce taxable income enough to shrink QBI benefits or create net operating losses that push value into future years. Without modeling, MSPs may shift tax benefits instead of maximizing them.

4. State tax rules don’t always follow federal law

Federal bonus depreciation doesn’t guarantee state conformity. Some states disallow it entirely or require add-backs, creating unexpected state tax bills or timing mismatches. This is a common (and costly) surprise for growing MSPs.

Bonus Depreciation vs. Section 179: What’s Better for MSPs?

Both bonus depreciation and Section 179 accelerate deductions, but they behave very differently in practice.

Bonus depreciation has no spending cap and applies automatically unless elected out, but it also can create a net operating loss. Meanwhile, Section 179 is capped (currently around $2.5M), limited by business income, and must be affirmatively elected.

When Bonus Depreciation Makes More Sense

Bonus depreciation is usually the better tool when MSPs are making large infrastructure investments or growing faster than profits stabilize.

If you’re upgrading servers, networking, or client hardware at scale, bonus depreciation matters because it has no spending cap under IRC §168(k). Whether you invest $250,000 or $2 million, the deduction isn’t limited the way Section 179 is.

It’s also valuable in years where CapEx is high, but income is uneven, which is common during growth spurts, major client onboarding, or pre-expansion buildouts. Because bonus depreciation can create a net operating loss (NOL), it allows MSPs to capture deductions now and apply them against future income under IRC §172, rather than losing the benefit altogether.

So for MSPs pursuing aggressive growth, bonus depreciation removes tax friction from necessary spending. You invest when the business needs it, not when deductions are convenient.

When Section 179 May Be Better

Section 179 often works best for MSPs with smaller, predictable purchases and consistent profitability.

Because Section 179 deductions are limited by both a dollar cap and business income (IRC §179), they’re useful when you want deductions to offset income, but not push the business into a loss. That can be appealing for mature MSPs prioritizing stable tax outcomes and clean financials. You might benefit most from Section 179 if you’re making moderate, predictable equipment purchases, expect consistent profitability, and want to reduce taxable income without creating a net operating loss.

In practice, many MSPs use both Section 179 and bonus depreciation in the same year. The key is making that mix intentional instead of accidental.

What 100% Bonus Depreciation Means for MSP Capital Investments

The return of 100% bonus depreciation changes how MSPs should think about capital investments, from routine refresh cycles to long-term infrastructure planning.

Infrastructure Upgrades and Refresh Cycles

With the permanent restoration of 100% bonus depreciation under the OBBBA, MSPs have a major planning lever to revisit infrastructure upgrades they may have delayed under the TCJA. Prior to this law, bonus depreciation was gradually declining year over year and was set to reach 20% in 2026 and then disappear in 2027, which disincentivized waiting on capital purchases.

Now, the qualifying tangible property we discussed above is eligible to be fully expensed in the year it’s placed in service, as long as it was acquired and placed into service after January 19, 2025.

That change does several significant things for MSPs:

- Reduces the after-tax cost of modernization: Immediate expensing can dramatically lower taxable income in the year of purchase, improving cash flow and freeing up capital for further investment.

- Encourages accelerated refresh cycles: Instead of extending the life of aging equipment to capture multi-year depreciation deductions, MSPs can take a full deduction up front, making it economically attractive to refresh infrastructure more frequently.

- Shifts risk calculus: Newer infrastructure often brings better performance, reliability, and security hardening, reducing operational risk and minimizing exposure to outages or vulnerabilities from outdated hardware.

In effect, the tax code no longer penalizes MSPs for keeping infrastructure current; it rewards timely legitimate capital investment.

Hardware-as-a-Service (HaaS) Considerations

When MSPs structure offerings like Hardware-as-a-Service (HaaS), depreciation tax benefits hinge critically on who legally owns the asset and when it’s placed in service. Under Section 168(k) of the Internal Revenue Code, 100% bonus depreciation is available only to the owner of qualifying property, not just the user.

So for HaaS bundles:

- Ownership matters: If the MSP retains ownership of the hardware, and the asset is both acquired and placed into service after January 19, 2025, then the MSP can take advantage of full bonus depreciation on that asset in the year of service.

- Placement and billing timing: Contracts negotiated but not executed until after the key date may unlock full expensing; those with binding contracts before January 20, 2025 may remain subject to the old phase-down rules.

- Billing structure can affect tax treatment: Leasing structures, finance agreements, and service bundles must be carefully documented so the IRS can clearly see whether the MSP or the customer holds the asset for tax purposes. Misalignment here could inadvertently transfer depreciation rights or eliminate them.

Preserving bonus depreciation in HaaS setups typically requires tight coordination between: finance teams, tax advisors, service delivery, and sales.

Failing to coordinate can lead to unintended consequences, such as MSPs giving up deductions they could have claimed or customers capturing tax benefits that were never intended for them. Clear documentation, thoughtful contract language, and advanced tax planning help ensure that the full financial advantage of 100% bonus depreciation is preserved as part of HaaS business models.

Timing Purchases Strategically Under the OBBBA

When an Asset Is “Placed in Service” Matters

Under federal depreciation rules, bonus depreciation hinges on when an asset is “placed in service”, not just when it’s purchased. An asset is considered placed in service when it is installed, configured, and ready and available for its intended use, even if it isn’t yet actively used in revenue-producing operations. That readiness condition determines the tax year in which bonus depreciation applies.

With the OBBBA permanently restoring 100% bonus depreciation for qualifying property placed in service on or after January 19, 2025, this timing becomes even more important for MSPs ordering computers, servers, networking gear, or qualified software late in the year.

Common mistakes MSPs make around this include:

- Buying equipment late in the year but not deploying it until the next year, leading to depreciation on the following year’s tax return instead of the intended current year.

- Failing to document installation and readiness without clear records showing the asset is ready for use, the IRS may deem the asset placed in service later than intended.

- Assuming delivery equals placed in service, mere delivery doesn’t satisfy the readiness test unless the hardware or software is installed and available for its intended use.

Under bonus depreciation rules, these placement details determine not just if you get a large deduction, but in which year you get it, a critical distinction for cash-flow and tax planning around year-end.

Aligning Purchases With Tax Planning Goals

Strategic timing of capital expenditures still matters under the OBBBA, but it should be integrated with your broader planning goals rather than executed in isolation.

Year-end buying should align with:

- Cash flow forecasts: You want tax timing to help, not hurt, your operating budget; taking a deduction in a low-income year when you can’t fully use it may not be optimal.

- Estimated tax payments: Accelerating deductions affects quarterly estimates and potential underpayment penalties, so coordinate with your tax adviser to adjust estimated payments if needed.

- Broader growth and hiring plans: If you’re scaling headcount or services, shift investments into years where deductions support expanded payroll and operating costs.

Buying just to buy without considering placed-in-service timing, planning goals, and overall tax position often leads to missed deductions or mismatches between tax benefits and business needs.

Common Bonus Depreciation Mistakes MSPs Should Avoid

Even with permanent 100% bonus depreciation under the OBBBA, MSPs frequently trip over a few recurring pitfalls that can significantly reduce or even eliminate the intended tax advantage:

1. Assuming all software automatically qualifies

Only certain computer software qualifies as “qualified property” for bonus depreciation, typically software that must be depreciated under the Modified Accelerated Cost Recovery System (MACRS). If the software doesn’t meet those criteria (for example, custom internally-developed software not subject to depreciation), it may not be eligible.

2. Confusing Section 179 limits with bonus depreciation rules

Section 179 and bonus depreciation both accelerate write-offs, but they differ:

- Section 179 has annual dollar limits and is capped by taxable income, whereas bonus depreciation does not have a dollar limit and can generate a loss.

- Bonus depreciation applies automatically (unless you elect out), whereas Section 179 is elective on an asset-by-asset basis.

Misunderstanding the interplay between these two can lead MSPs to apply Section 179 where bonus depreciation would have delivered a bigger benefit or to miss income limitations that restrict Section 179 usage.

3. Poor documentation of placed-in-service dates

Without clear documentation (dates installed, configured, tested, and available for service), it’s easy to lose a year of bonus depreciation or become unable to substantiate that deduction position if the IRS questions it.

4. Failing to model interaction with QBI, NOLs, and estimated taxes

Bonus depreciation can create or increase a net operating loss (NOL) and interact with the Qualified Business Income (QBI) deduction. A large deduction in one year might reduce taxable income so much that the business isn’t positioned to use other tax attributes efficiently. Comprehensive modeling with tax advisors helps ensure you don’t inadvertently eliminate the benefit you sought.

Key Takeaways: Using Bonus Depreciation as a Strategic MSP Tax Tool

The return of 100% bonus depreciation under the OBBBA gives MSPs one of the most powerful tax-planning levers available, but only when it’s used deliberately. For MSPs making meaningful infrastructure investments, the upside is real: lower after-tax costs, improved cash flow, and the ability to modernize without being punished by timing. The biggest gains go to MSPs that coordinate purchase timing, placed-in-service dates, and income projections as part of a broader financial strategy, not those making last-minute buying decisions in December.

Final Thoughts: Plan Bonus Depreciation Into Your MSP Tax Strategy

Bonus depreciation isn’t just a line on a spreadsheet, it influences purchasing decisions, service delivery, cash flow, and long-term growth. When it’s treated as an afterthought at filing time, much of its value disappears. Planned intentionally, it becomes a strategic lever that helps MSPs modernize infrastructure, manage cash flow through growth cycles, and invest on their own timeline instead of the IRS’s.

The MSPs that capture the full benefit of the OBBBA are the ones that coordinate purchase timing, placed-in-service dates, and income projections as part of a broader financial strategy. That requires working with advisors who understand service-company depreciation rules and embedding tax planning into day-to-day operational and financial decisions, not treating it as a once-a-year exercise.

As 2026 approaches, having a structured plan matters. A dedicated MSP tax prep checklist can help ensure depreciation opportunities don’t slip through the cracks, while deeper OBBBA planning, (such as reviewing timing, eligibility, and tradeoffs with an expert) can prevent costly missteps before purchases are made.

Under the OBBBA, proactive planning isn’t optional. It’s how well-run MSPs stay in control, reduce risk, and turn necessary capital spending into a lasting competitive advantage.