Section 179 has long been one of the most practical and familiar tax tools for MSPs. If you’ve ever purchased servers, networking gear, laptops, or other internal infrastructure, there’s a good chance Section 179 was doing the heavy lifting when tax season came. It’s the provision that makes it possible to accelerate deductions, reduce taxable income, and keep your cash flow more predictable without waiting years for standard depreciation schedules to catch up.

What’s different under the One Big Beautiful Bill Act (OBBBA) isn’t that Section 179 went away, it’s that it now sits alongside restored 100% bonus depreciation. That combination gives MSPs more options than ever for expensing equipment, but it also adds a layer of complexity. Choosing the right tool for the right asset (at the right time) has become a critical part of tax planning.

As MSPs head into 2026, understanding how Section 179 works, where its limits still apply, and when it makes sense compared to bonus depreciation is critical to optimizing deductions for the next tax year.

In this playbook, we’ll break down exactly what changed under the OBBBA, what stayed the same, and how MSPs can use Section 179 intentionally (not by default) to support smarter financial and operational decisions.

How Section 179 Expensing Works for MSPs in 2026

Section 179 of the Internal Revenue Code allows businesses to immediately expense the cost of qualifying tangible property in the year it is placed in service. Instead of depreciating equipment over a standard recovery period (often five or seven years), Section 179 accelerates that deduction into the current tax year.

For MSPs, this treatment aligns closely with how technology investments actually function. Even though MSPs are service businesses, service delivery depends on physical infrastructure. Servers, firewalls, switches, endpoints, and internal systems all require upfront capital, and Section 179 allows MSPs to recover those costs faster from a tax perspective.

One important distinction, however, is that Section 179 is elective. MSPs must affirmatively choose to apply it, and the deduction is subject to limits that determine how much of the expense can actually be used in a given year, which makes Section 179 more controlled than other deductions.

How did Section 179 Change Under the OBBBA (2026 Update)

Before diving into what changed, it helps to understand where Section 179 stood under prior law. Knowing the limits, phase-outs, and income restrictions MSPs faced before the Big Beautiful Bill makes it easier to see why the new rules matter and how deeply they can impact 2026 planning.

Section 179 Before the Big Beautiful Bill

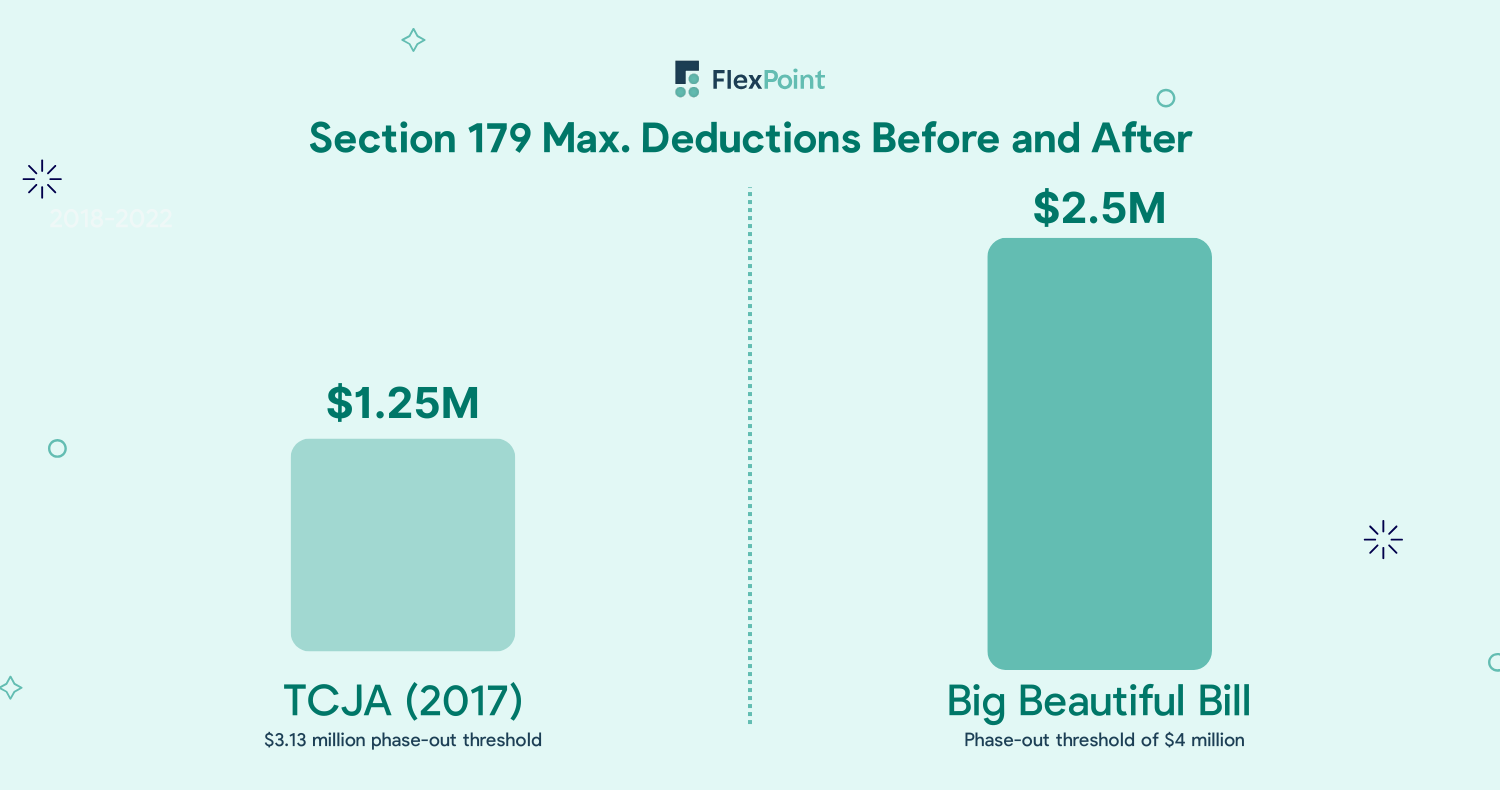

Before the OBBBA, Section 179 was already shaped heavily by the Tax Cuts and Jobs Act (TCJA). TCJA expanded Section 179 by increasing deduction limits and broadening the definition of qualifying property, making it far more relevant for service-based businesses like MSPs. Specifically, in 2017, the TCJA raised the cap of Section 179 to $1 million, and the phaseout threshold was set at $2.5 million.

Despite those expansions, Section 179 retained two core constraints: a dollar-based spending cap that phases out once total equipment purchases exceed a threshold, and an income limitation that prevents the deduction from exceeding taxable business income.

As bonus depreciation began phasing down after 2022, many MSPs leaned more heavily on Section 179, often not because it was the optimal choice, but because it was the only way to accelerate deductions. That dynamic introduced uncertainty, especially for growing MSPs investing heavily in infrastructure to support new clients, expanded SLAs, or internal growth.

In practice, MSPs found themselves navigating questions like whether equipment purchases would push them into a phase-out range or whether income would be sufficient to fully use the deduction at all.

Section 179 After the BBB (2026 and Beyond)

The One Big Beautiful Bill Act (OBBBA) did not eliminate Section 179 or fundamentally change how it works. Instead, it clarified where Section 179 fits in the broader tax landscape by restoring 100% bonus depreciation while keeping Section 179’s existing framework intact.

Under the Big Beautiful Bill, Section 179 continues to operate with a cap at $2.5M and phase-out thresholds reaching $4M that are indexed for inflation. Just as importantly for MSPs, it remains fully available to service-based businesses, including asset-heavy managed service providers that rely on regular equipment investment to deliver services.

The most meaningful change isn’t in the mechanics of Section 179 itself, but in how it now interacts with bonus depreciation. With both tools available at the same time, Section 179 shifts from being a default expensing choice to a more targeted planning tool. It is best used in situations where predictability and income alignment matter more than maximizing total deductions.

Key takeaways for MSPs planning for 2026 and beyond:

- Section 179 remains in place under the OBBBA and continues to be a viable expensing option

- Spending caps and phase-out thresholds are updated and indexed for inflation

- Service-based businesses, including MSPs, remain eligible to use Section 179

Overall, this means Section 179 merely becomes one tool in a broader expensing strategy that should be aligned with income expectations, cash flow needs, and long-term growth planning.

What MSP Assets Qualify for Section 179 Expensing

Common MSP Assets That Qualify

Most MSPs already purchase assets that qualify for Section 179 as part of normal business operations. While MSPs are service-based companies, delivering those services still depends on owning and operating significant physical infrastructure. When those assets are purchased outright and placed in service during the tax year, they often meet Section 179 eligibility.

Common qualifying assets for MSPs typically include:

- Servers and storage systems used to support client workloads or internal operations

- Networking equipment, such as firewalls, switches, routers, and access points

- Laptops, desktops, and workstations used by employees or deployed to clients

- Endpoint devices purchased and owned by the MSP as part of managed or bundled service offerings

- Backup appliances and on-premise security hardware used to support client environments

- Non-residential building improvements like roofs, HVAC (heating, ventilation, and air-conditioning) systems, fire protection and alarm systems, and security systems

There is a primary overlap between what is eligible for 100% bonus depreciation and what is eligible for Section 179; however, notably, improvements to nonresidential real property is relevant for Section 179 only.

In addition to hardware, certain off-the-shelf software may also qualify for Section 179. To be eligible, the software must generally be purchased outright (not subscribed to), subject to depreciation under MACRS, and placed in service during the same tax year. For MSPs that still operate on-premise systems or internally hosted tools, software deductions can represent a meaningful and often overlooked tax opportunity.

As always, eligibility hinges on ownership, business use, and proper classification. Not every technology expense qualifies simply because it supports operations, which makes careful asset tracking and coordination with a tax professional especially important.

Ineligible MSP Assets for Section 179

While Section 179 can be a powerful tool for MSPs, not all assets are eligible. Understanding what does not qualify is just as important as knowing what does, especially as service models evolve.

Key exclusions for MSPs include:

- Assets used primarily for personal or non-business purposes: equipment or devices that aren’t used in delivering MSP services cannot be deducted.

- Cloud-only or subscription-based software, most SaaS, platform subscriptions, or recurring cloud services do not qualify for Section 179 because the MSP does not own the underlying property.

- Land improvements: leased office space improvements and landscaping are generally ineligible.

- Vehicles not used predominantly for business. Passenger vehicles must meet strict business-use thresholds to qualify.

- Assets exceeding taxable business income. Even if an asset technically qualifies, the deduction is limited to the MSP’s net taxable income for the year.

This is particularly relevant for MSPs offering Hardware-as-a-Service (HaaS) or Device-as-a-Service (DaaS). In these models, the tax benefit depends on legal ownership, how the asset is used, and when it is placed in service. Simply purchasing technology for client delivery does not automatically make it eligible for Section 179.

By keeping these exclusions in mind, MSPs can avoid common mistakes, ensure proper planning, and focus deductions on assets that truly qualify under the law.

Disclaimer: We are not tax professionals. This content is for general informational purposes only. Always consult a licensed tax advisor for guidance specific to your MSP or IT business before making financial decisions.

Section 179 vs. Bonus Depreciation

When it comes to accelerating deductions for capital investments, MSPs have two main tools at their disposal: Section 179 expensing and bonus depreciation. Understanding the differences between them is key to making strategic tax and cash flow decisions.

Should MSPs Use Section 179 or Bonus Depreciation?

For most MSP owners, the decision between Section 179 expensing and bonus depreciation comes down to profitability, scale, and intent. While both provisions allow accelerated deductions, they behave very differently in practice, and the right choice depends on what your MSP is trying to accomplish in a given year.

Section 179 expensing generally works best for MSPs with steady, predictable profits that want deductions to closely align with current-year taxable income. Because Section 179 cannot exceed business income, it naturally limits how much can be deducted in a single year. That constraint can actually be a benefit. It allows MSPs to reduce tax liability without pushing the business into a net operating loss, which helps preserve clean financial statements, consistent owner distributions, and lender-friendly profitability.

This makes Section 179 particularly well-suited for MSPs making smaller, recurring hardware purchases (things like routine server replacements, networking upgrades, or endpoint refreshes) where the goal is tax efficiency rather than aggressive deduction acceleration.

On the other hand, 100% bonus depreciation is built for large capital expenditure years. With no spending cap and no income limitation, bonus depreciation allows MSPs to expense significant amounts of equipment even if doing so creates a net operating loss (NOL) that carries forward to future years. This flexibility is valuable during periods of rapid growth, major infrastructure investments, or business transitions where upfront deductions matter more than short-term profitability.

Ultimately, the choice between Section 179 and bonus depreciation is about aligning your expensing strategy with how your MSP grows, invests, and generates cash. In many cases, the most effective approach isn’t choosing one over the other, but intentionally coordinating both to match income, manage tax exposure, and support long-term growth planning.

If you’d like to know more about 100% bonus depreciation and if it’s the right fit for you, read more here.

Section 179 Mistakes to Avoid

Most Section 179 mistakes MSPs make don’t come from aggressive tax planning; they come from reasonable assumptions that turn out to be wrong. Because Section 179 has existed for so long, many MSP owners assume it’s simple. Under Trump’s new tax law framework, however, Section 179 is more conditional than it appears.

One of the most common errors is assuming all technology purchases qualify. While many types of tangible equipment are eligible, not every expense that supports service delivery qualifies for Section 179 expensing. As briefly mentioned above, cloud-based and subscription software generally does not qualify, even though it’s central to many MSP operations.

Another frequent issue is ignoring the income limitation. Unlike bonus depreciation, Section 179 deductions cannot exceed taxable business income. For MSPs with fluctuating profitability or heavy reinvestment, this limitation can significantly reduce the usable deduction, often forcing a portion of the expense to be carried forward and limiting near-term tax savings.

Poor coordination between Section 179 and bonus depreciation is also common. Because Section 179 requires an affirmative election while bonus depreciation applies automatically, failing to plan how the two interact can lead to deductions being applied inefficiently. Under the OBBBA, where 100% bonus depreciation has been restored, this coordination matters more than ever.

Finally, some MSPs use Section 179 reactively rather than strategically. Accelerating deductions without modeling future income can reduce flexibility in later years when profitability or capital needs change.

How MSPs Can Use Section 179 Strategically for 2026 Tax Planning

Section 179 remains a powerful tax planning tool under the OBBBA, but it delivers the most value when it’s used intentionally. With 100% bonus depreciation restored under the Big Beautiful Bill, MSPs now have more options for expensing equipment, which also means more opportunity to get it wrong if decisions aren’t coordinated.

Strategic use of Section 179 starts with proactive income modeling. Understanding how much taxable income your MSP expects to generate, how much equipment you plan to place into service, and how those decisions affect future years is far more effective than making expensing elections at filing time. Section 179 works best when it supports cash flow, preserves financial flexibility, and aligns with how your business is actually growing.

Just as importantly, MSPs should not make Section 179 decisions in a vacuum. Hardware-heavy service models, HaaS or DaaS offerings, financing structures, and growth investments all influence which expensing strategy makes the most sense. That’s why working with tax professionals who understand MSP business models is critical. Generalist advice often misses the nuances that matter most in managed services.

Under the Big Beautiful Bill, the MSPs that benefit most from Section 179 aren’t the ones taking every available deduction; they’re the ones taking the right deductions, at the right time, for the right reasons.

If you’re planning for 2026, now is the time to get organized. A clear picture of upcoming equipment purchases, projected income, and expensing options will make tax season far less reactive. To help, we recommend starting with a 2026 MSP Tax Prep Checklist, designed to make conversations with your tax advisor more productive and ensure your expensing strategy supports your long-term growth, not just short-term tax savings.