Many managed service providers (MSPs) utilize surcharging as a way to offset rising credit card processing fees. Passing some or all of these processing costs to clients can protect slim profit margins. However, there is a critical distinction between credit card and debit card payments when it comes to surcharges.

While credit card surcharges are permitted in many U.S. states under specific conditions, debit card surcharging is not legally allowed anywhere in the United States. Federal law and card network rules explicitly prohibit adding fees to debit card transactions, even when a debit card is processed without a PIN (i.e., “as credit”).

In this article, we’ll clarify what debit card surcharging means and why it’s universally banned in the U.S. We’ll discuss the typical cost of processing debit payments, explain the legal background (from the Durbin Amendment to Visa/Mastercard policies), and outline compliant strategies MSPs can use instead of debit surcharges.

Finally, we’ll explore how an MSP-specific billing platform helps implement these strategies, reduce payment costs, and ensure 100% compliance with all relevant regulations.

Disclaimer: This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for, legal advice. Conduct thorough due diligence and consult with a qualified legal professional to address specific questions related to your MSP.

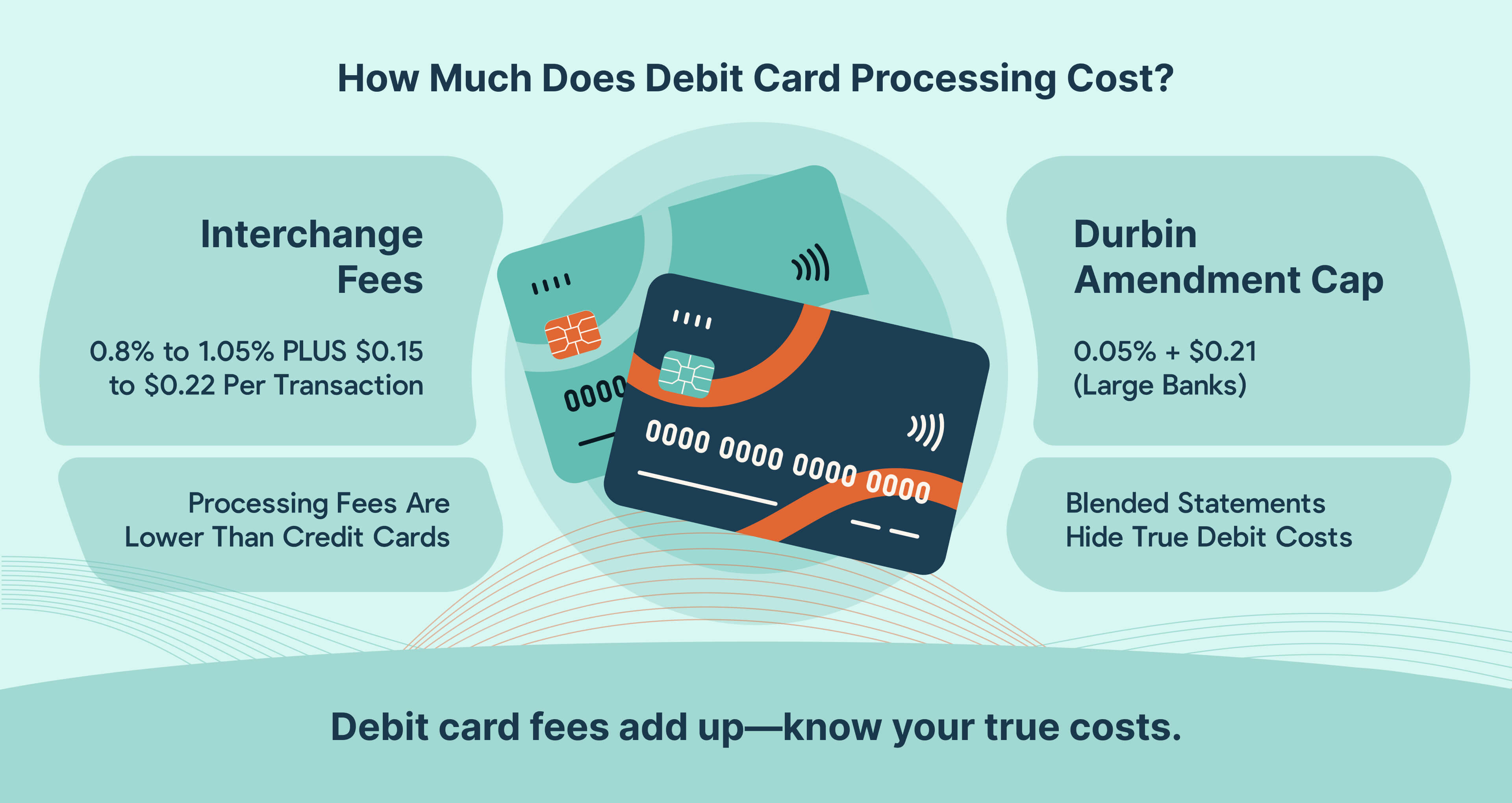

How Much Does Debit Card Processing Cost?

Even without surcharges, debit card payments aren’t “free.” However, the processing fees incurred for debit cards are lower than those for credit cards. Regardless, these fees still add up for MSPs.

Online debit card transactions (such as clients paying invoices via a web portal) are usually routed through credit card networks as signature-based payments (no PIN).

The interchange fees for these transactions typically range from 0.80% to 1.05% of the transaction amount, plus a fixed $0.15–$0.22 per transaction.

For example, a $100 debit payment might incur roughly $0.80–$1.05 in percentage fees and an additional $0.15–$0.22 in fixed costs.

These rates are generally lower than those for credit cards, which typically range from 2% to 4% per transaction. However, they can still eat into MSP profit margins, especially on high-volume recurring billings or multiple small-ticket transactions. Want to learn more about credit cards and how to save your margins? Watch this video:

According to data from the Federal Reserve, the average debit transaction costs about $0.34 in interchange fees.

It’s important to note that U.S. law caps the interchange on many debit cards issued by large banks. Under the Durbin Amendment of the Dodd-Frank Act, regulated debit card fees are limited to 0.05% + 21¢ (plus a one-cent fraud prevention fee) per transaction.

However, this cap doesn’t apply to the cards of smaller banks (with assets below $10 billion), so some debit transactions fall within the ~1% + $0.15 range noted above.

Many MSPs unknowingly absorb debit card fees because their processing statements don’t always distinguish debit vs. credit cards.

Some providers charge a blended rate for all “card” payments, and standard reports might not break out how many were debit vs credit. This lack of visibility makes optimization a challenging task. MSPs might not realize that a sizable chunk of fees (often 0.8%–1% on certain client payments) came from debit cards.

Without transparent reporting, it is difficult to identify opportunities to reduce costs or encourage alternative payment methods.

In short, debit card processing is not free, and MSPs need strategies to manage these fees since directly surcharging them is off the table (legally).

What Is Debit Card Surcharging?

Debit card surcharging refers to adding an extra fee to a client’s bill when they opt to pay with a debit card.

In other words, the MSP would add a surcharge (such as 1% or a fixed amount) at checkout or when making an invoice payment to offset the processing fee for a debit transaction.

The idea is similar to credit card surcharges (shifting the cost of the processing fees to the client). However, with debit cards, surcharging is not permitted.

MSPs may be tempted to surcharge debit payments to reduce costs, but doing so is prohibited by U.S. regulations.

It’s important to distinguish debit card surcharges from other fee models. Some MSPs implement credit card surcharges (where allowed by state law) or offer cash/ACH discounts (“pay by cash or bank transfer and save X%”). Those practices, if done correctly, can be legal.

However, a surcharge specifically for debit card payments is prohibited across all states.

Even if the debit card is part of a Visa or Mastercard network and processed as “credit”, it is still a debit card and you cannot impose a surcharge on it. The following section will explain why.

For now, MSPs should understand that any fee added solely for using a debit card is never permitted in the United States. This differs from credit card surcharges, which vary by state.

Why Debit Card Surcharging Isn’t Allowed: Laws and Network Rules

Debit card surcharging isn’t just discouraged; both federal law and the rules of all major payment networks explicitly forbid it. MSPs must be crystal clear on this point to avoid hefty penalties.

Let’s break down the key reasons and regulations behind the ban on debit surcharges:

1. Federal Regulations

At the federal level, debit surcharging is banned by law. The cornerstone here is the Durbin Amendment of the Dodd-Frank Wall Street Reform Act (2010).

The Durbin Amendment is best known for capping debit interchange fees, but it also prohibits merchants from circumventing these caps by passing fees on to their clients.

In practice, the Durbin Amendment flatly prohibits merchants from adding a surcharge to any debit card transaction.

This applies to all debit cards, including:

- Personal debit cards

- Business debit cards

- Prepaid debit (reloadable) cards

The logic was to protect consumers. Congress capped what banks can charge retailers for debit processing, and in exchange, retailers can’t directly charge consumers extra for using debit.

Unlike credit cards, where no federal law outright bans surcharges (leaving the states and card networks to set rules), debit cards have a nationwide ban on surcharging written into federal statute.

This means no state can “legalize” debit surcharges. Even if a particular state has laws allowing credit card surcharges (or no laws against them), it does not change the fact that debit surcharges are illegal everywhere in the United States. MSPs should treat this as a hard rule with no exceptions.

2. Card Network Policies

In addition to federal law, the major card networks (Visa, Mastercard, American Express, and Discover) have their own rules prohibiting debit surcharges.

Visa’s official surcharge guidelines state it plainly: merchants may surcharge credit card purchases (under certain conditions), but “The ability to surcharge only applies to credit card purchases, and only under certain conditions. U.S. merchants cannot surcharge debit card or prepaid card purchases.”

This policy applies to all networks. Surcharges are only allowed on credit cards, never on debit or prepaid.

The determining factor is the card type (debit/prepaid vs credit), not the technical processing method. Modern payment systems can identify card types by their BIN (the first six digits of the card number), so the networks will know if a fee was applied to a debit card.

In summary, Visa, Mastercard, Amex, and Discover all ban surcharges on debit and prepaid cards, reinforcing what U.S. law already mandates.

We recommend consulting with a lawyer or qualified legal professional if you are unsure of your surcharging options.

3. Enforcement & Penalties

The prohibition on debit surcharges is backed up by enforcement measures that can be severe. If an MSP were to attempt surcharging a debit card, they are risking fines, chargebacks, and even the loss of their merchant account.

Card networks have been increasing enforcement efforts in recent years, actively monitoring transactions for improper surcharges. Non-compliant merchants can face substantial fines and penalties that accumulate quickly.

For example, Visa may issue violation fees through an acquiring bank if a managed service provider (MSP) surcharges a debit card. These fines can range in the thousands of dollars, depending on the size and frequency of the violation.

Beyond direct fines, MSPs could also have transactions reversed. Clients might dispute a surcharge on a debit payment, leading to chargebacks that an MSP is unlikely to win (since the surcharge clearly violates network rules). Excessive chargebacks or rule violations can lead to an MSP being flagged as high-risk.

Payment processors often reserve the right to terminate an account if the account holder breaks network rules or laws.

Some payment service providers or payment gateways will immediately suspend or terminate a merchant's account if they detect a debit card surcharge, to protect themselves from potential network penalties.

The consequences of surcharging debit can snowball:

- Lost revenue from refunds/chargebacks

- Fees for each violation

- Damage to your relationship with processors

- Losing the trust of your clients

Simply put, it’s not a minor infraction; it’s treated as a serious compliance breach.

4. Misconceptions About Signature-Based Debit

One of the biggest misunderstandings among merchants is the idea that running a debit card as a credit transaction makes it acceptable to surcharge.

Let’s dispel that myth clearly: if the client’s card is a debit card, an MSP cannot add a surcharge, regardless of whether the client enters a PIN or not.

For example, Visa’s merchant Q&A clarifies that even if a debit card is processed on the credit network, it still cannot be surcharged.

The processing system might label the transaction as “Visa credit” (meaning it went through Visa’s network), but Visa knows from the card number that it was actually a debit card.

As mentioned, card network rules (such as Visa) explicitly state that even a signature debit transaction (a debit card processed without a PIN) cannot be surcharged.

Sometimes MSPs assume they can slip in a surcharge on an invoice if the client’s debit card is “run as credit.” This is a dangerous misconception. The card networks have sophisticated BIN recognition and compliance checks in place.

If you attempt to surcharge and the card used is a debit card, it will be detected as a violation. From the client’s perspective, they might not even realize a surcharge on their debit card is illegal until their bank or an informed colleague flags it.

You never want to be in the position of trying to explain an unlawful fee to a client or to a card brand.

The bottom line is that a debit card is a debit card. There is no technical workaround to make surcharging legal. The safe and professional approach is never to apply surcharges to debit or prepaid transactions, period.

Summary: Financial & Legal Consequences for MSPs

For MSPs, attempting to surcharge debit cards is truly a no-win scenario. Legally, it’s prohibited across all 50 states (federal law preempts any state laws), and contractually, it violates card network agreements.

If an MSP were to add a debit surcharge, it would expose itself to significant risks, including fines from networks, payment disputes and chargebacks, forced refunds to clients, and possibly termination of its merchant account. These outcomes can easily cost far more than the few percentage points of fees the MSP was trying to save.

According to Visa, surcharging violations may result in penalties ranging from $50,000 to $1 million, depending on the severity and frequency of the infractions. Network enforcement is serious. Repeated violations can result in the permanent loss of card acceptance privileges.

Even if penalties weren’t an issue financially, alienating clients with improper fees would permanently damage the MSP. If a client discovers they were charged an unlawful fee, trust would be broken, and you could lose their account.

And since debit card fees are already capped (for big-bank cards) and lower than credit fees, the “savings” from surcharging debit are relatively small, whereas the potential costs are enormous. As such, every MSP in the U.S. must treat debit surcharges as off-limits.

Fortunately, an MSP can still optimize payment costs in other ways without breaking the law.

Next, we’ll explore these alternatives, including strategies that encourage clients to use lower-cost payment methods and tools that automate compliance.

Alternatives to Debit Card Surcharging for MSPs

Just because surcharging debit cards is not an option, that doesn’t mean MSPs are powerless against payment processing costs. There are smart, legal ways to reduce or recoup these fees.

Here are some alternative strategies to consider:

1. Promote ACH Payments

One of the most effective ways to cut payment costs is to shift more client payments to ACH (Automated Clearing House) transfers. ACH payments (bank-to-bank electronic transfers) tend to be cheaper than card payments.

Instead of paying ~1% on a debit transaction (or ~3% on a credit card), ACH fees are often a few dollars.

For example, the typical ACH transaction averages between $0.25 and $1.00 per transaction. Depending on the vendor you choose, ACH transactions have no percentage-based interchange fees like credit and debit cards do. This means whether a client pays a $200 invoice or a $20,000 invoice via ACH, the fee to the MSP is only a negligible flat amount.

Because ACH is so low-cost, many MSPs find it beneficial to incentivize ACH usage. MSPs could offer a small discount for paying via ACH or bank transfer (the inverse of a credit card surcharge). Some MSPs frame this as an “ACH discount” or simply make ACH the default payment method on their invoices.

By highlighting the ACH option (e.g., “Pay by ACH transfer (no fee)” prominently, versus “Pay by credit/debit card (3% fee may apply)” in smaller text), an MSP gently steers clients to the lowest-cost channel.

Over time, moving a substantial portion of payments to ACH can save an MSP thousands in processing fees.

A robust MSP payments platform, such as FlexPoint, can help you offer ACH payments seamlessly for clients. FlexPoint also supports same-day ACH, so MSPs can benefit from faster bank transfers without switching to more expensive card rails. This gives you the speed of card processing with the low cost of ACH.

Clients appreciate quicker payment confirmation, and your team gets faster cash flow, often within hours instead of days.

2. Offer Payment Options Strategically

How an MSP presents payment options to clients can influence their choices. Rather than outright banning cards (which could frustrate clients), an MSP can design its invoices and payment portals to encourage the most cost-efficient option.

To do so, start by offering multiple payment methods, like bank ACH and credit/debit cards, but present them strategically. List the preferred method first (such as ACH) and consider adding a note about it.

For instance: “Prefer to save on fees? Pay via ACH transfer using the details below.”

This type of messaging informs clients that card payments incur additional costs.

Another approach is to implement a cash/ACH discount program, where you advertise two prices: the regular price (which includes card processing costs) and a lower price for payment by cash or bank draft. This is permitted as a “discount” rather than a surcharge on cards.

It achieves a similar outcome (clients have a financial incentive to avoid using a card), but it’s compliant in all states. Communicate any such differences upfront, as clients should never feel misled by fees.

Client communication can be as simple as a line on the invoice: “Paying by card? A 3% processing fee is applied. To avoid this fee, you can pay via ACH at no additional cost.” This allows the client to decide, and many will opt for the fee-free method if it’s easy to do so.

3. Use Tools That Support Payment Cost Optimization

Manually policing every transaction and guiding each client can be a burdensome task. This is where the right software can be of great help. Some payment automation and billing platforms can automatically enforce cost-optimizing practices.

For example, advanced payment systems can detect the type of card being used in real time. If a client is about to pay with a debit card, the software could be configured not to apply any surcharge (avoiding a compliance issue by design).

If a client uses a credit card and surcharges are legal in your state, the system can automatically add the appropriate surcharge and clearly label it. Good payment tools also handle the required receipt and invoice disclosures (separating the surcharge line item, etc.) to ensure compliance.

Additionally, an MSP-focused payment platform allows you to set defaults or incentives for payment methods.

For instance, you could set your portal so that the first option a client sees is “Pay by Bank (ACH)”. The software can still offer card payment as an option, but this gentle funneling can significantly increase ACH usage.

The overall idea is to leverage automation to minimize fees: let the system apply surcharges only where necessary, cap those fees to legal limits, steer clients to more affordable methods when possible, and log everything transparently.

By using a tool designed for MSP billing, you reduce the risk of human error (such as accidentally surcharging a debit card) and ensure consistent application of your cost-saving policies.

In the next section, we’ll see how FlexPoint’s payment platform specifically embodies these principles to save MSPs money safely.

How FlexPoint Helps MSPs Reduce Payment Costs Without Breaking the Rules

Navigating payment rules and optimizing fees can be challenging, but FlexPoint is a purpose-built solution that makes it much easier.

FlexPoint is an MSP-centric billing and payments platform that includes features to minimize processing costs without violating any rules.

Here’s how FlexPoint helps in practice:

1. Built-In ACH Promotion

FlexPoint’s platform offers your clients multiple payment options, including credit cards and ACH bank transfers. The system makes ACH payments straightforward for an MSP’s clients (through a secure bank link), encouraging them to use this low-cost method.

With FlexPoint, an MSP can even configure ACH-first workflows. For example, presenting the ACH option prominently or offering an automatic discount for ACH payments.

By shifting more volume to ACH (which often costs under $1 per transaction), FlexPoint helps dramatically reduce your fees without incurring any surcharges.

2. Payment Method Intelligence

FlexPoint uses payment method classification to detect what kind of card a client is using automatically. It determines whether a saved card or incoming payment is associated with a debit card, credit card, or prepaid card. This intelligence is critical because it means the platform will never accidentally apply a surcharge to a debit transaction.

If your MSP enables surcharging for credit cards, FlexPoint will apply those only to actual credit card payments. Debit cards are exempt from surcharges by rule, eliminating the risk of human error.

3. Automated Fee Controls