According to The Ascent, credit card companies in the U.S. charged merchants $135.75 billion as processing fees in 2023, of which interchange fees account for 70% to 90%.

Credit card interchange fees are a significant expense for MSPs that erode profit margins. MSPs often operate with tighter budgets, and credit card processing fees make expense management complex.

If MSPs are unaware of the actual costs they incur on payment processing, it hinders business growth. Additionally, passing on the fees to clients affects retention and loyalty.

Managing interchange fees effectively is essential for MSPs to remain competitive and financially viable.

This article clarifies interchange fees, their implications for MSPs, and strategies for managing these costs effectively.

What are Credit Card Interchange Fees?

Interchange fees are charges set by credit card networks such as Mastercard, Visa, American Express, and Discover on every electronic payment transaction. They charge a percentage of the transaction amount over a fixed cost.

MSPs must pay interchange fees as a component of transaction amounts when receiving payments from their clients through credit cards.

The interchange fee ranges from 1.29% to 3.5% of the transaction amount in the US. It is compensation paid by the merchant's bank, known as the acquirer, to the cardholder's bank, referred to as the issuer.

MSPs incur these fees when a client pays using a credit card.

Here are the details of credit card interchange fees by prominent credit card networks:

Disclaimer: For the table above, we’ve displayed only the Interchange rates for the type of cards usually accepted by MSPs.

All Card Networks displays have individual interchange rates for different types of credit cards (personal and commercial) and industries.

Credit card interchange fees vary based on various factors, including the type of card used (commercial cards like business cards, corporate cards, or purchasing cards), the nature of the transaction, the merchant’s industry, and the Merchant Category Code (MCC).

MSPs handle high transaction volumes of varying amounts regularly. It is difficult for MSPs to track each credit card transaction and predict the interchange fees.

So, if your client uses a credit card that offers rewards on spending, such as cashback or rewards/points, the interchange fees will be higher as the card issuer needs to cover the cost of the rewards.

Similarly, high-risk industries, such as travel, pay higher interchange fees.

However, if you set up recurring billing for your clients, the interchange fees will be lower than those for one-time payments.

The card networks (VISA, MasterCard, American Express) establish these fees as non-negotiable and an inherent cost of accepting credit card payments.

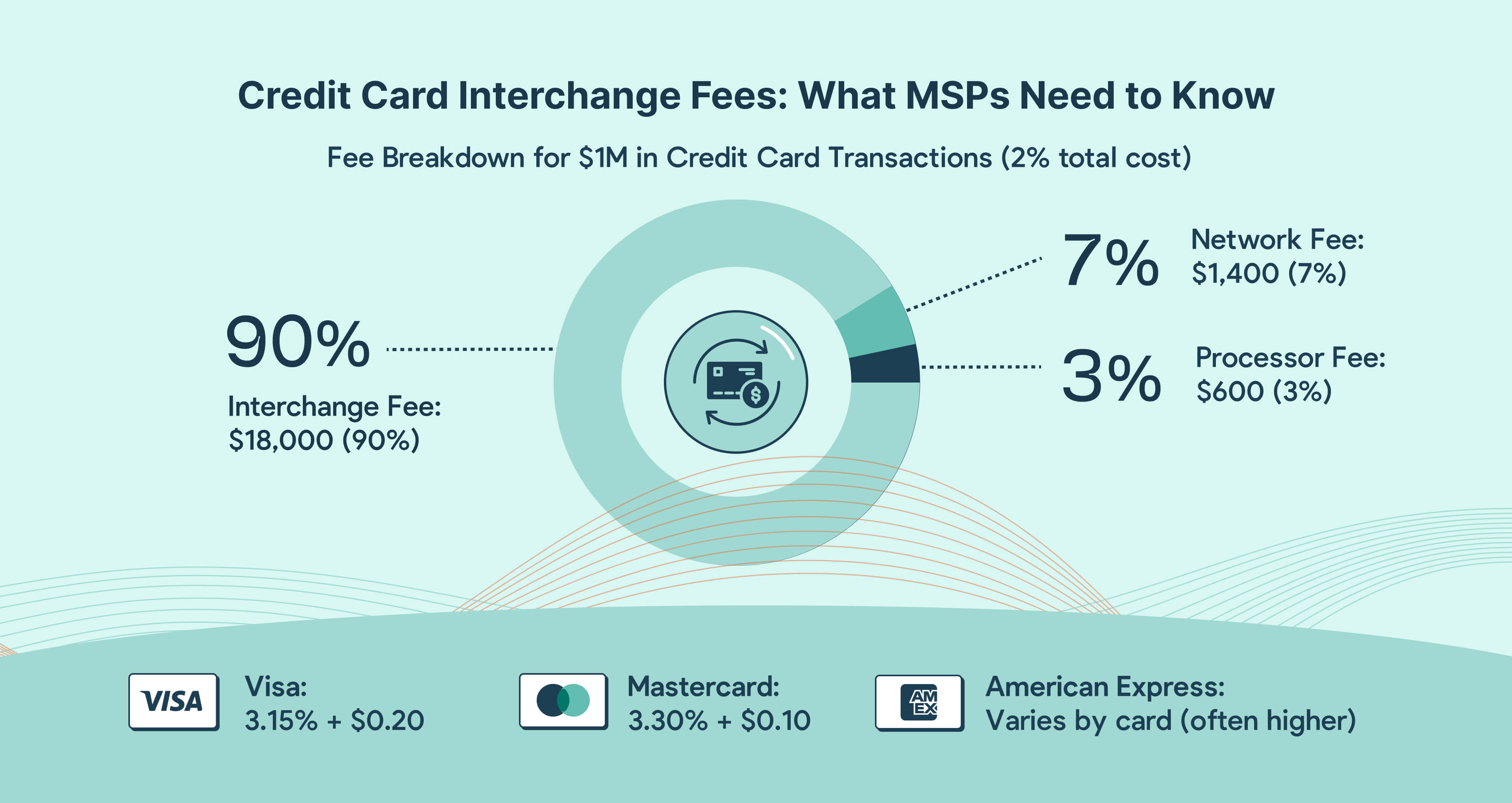

For example, let us consider a scenario where an MSP processes $1 million per year in credit card transactions at an average interchange fee of 2%. They would incur $600 in processor fees, $1,400 in network fees, and $18,000 in interchange fees alone.

Breakdown of fees for $10,00,000 credit card transaction

Assuming the merchant has a 2% cost of transacting the payment

It is a substantial amount that could otherwise be allocated towards essential areas such as hiring staff, investing in growth initiatives, funding marketing campaigns, or upgrading technology and infrastructure.

As these funds are diverted to cover payment processing costs instead of being reinvested into the business, it stifles MSP business growth and reduces competitiveness.

Understanding the impact of these unavoidable costs helps MSPs anticipate expenses and strategize cost management.

9 Implications of Interchange Fees for MSPs

Interchange fees drive up operational costs for MSPs. They increase as you process high volumes of credit card payments and even affect your profit margins.

Since credit card networks decide interchange fees, they are non-negotiable.

Despite the convenience of accepting credit card payments, the high interchange costs cut through profit margins. As a response, MSPs even encourage clients to use check payments instead.

However, it poses challenges, such as potentially slower payment cycles and additional costs in processing paper payments. According to PYMNTS, limiting instant payment options impacts customer satisfaction.

These challenges have prompted MSPs to find ways to manage interchange fees effectively.

MSPs must factor these costs into their pricing strategies while maintaining transparency. These must accurately calculate interchange fees to maintain profitability without deterring clients.

The fee fluctuates based on risk and card types, so proper calculations help manage cash flow, set realistic budgets, and forecast expenses.

With informed cash flow management, you can maintain a competitive edge and invest in growth opportunities.

Here are the critical implications of interchange fees that MSPs must consider:

1. Cost Burden:

According to Evolve Payment, interchange fees account for up to 90% of the credit card processing costs. These fees burden your MSP as they are tied directly to the volume and amount of credit card transactions processed.

If your MSP handles large transaction amounts or volumes, these costs will escalate steeply.

For example, if your MSP’s monthly recurring revenue (MRR) is $100,000 per month at a 2% credit card transaction processing fee, you would pay around 90% of the cost as interchange fees, amounting to around $1800.

That amounts to around $21,600 annually.

Note: This is an illustration. In most cases, the total credit card processing fee for MSPs ranges anywhere from 2.5% to 4%.

It is a considerable amount that reduces the available capital for your MSP’s operations.

2. Cash Flow Management:

Interchange fees complicate cash flow for MSPs due to their variable nature. In addition to the fixed percentage, these fees fluctuate based on the transaction amount, MCC (merchant category code), and client card types.

For instance, when you send an invoice to a client, you have no control over the type of credit card they will use to make payment.

These factors are difficult to predict, so the MSP finds it challenging to forecast future expenses accurately.

Cash flow management becomes tough without a robust financial tracking system that considers all factors related to interchange fees.

3. Pricing Transparency:

MSPs struggle to maintain transparency in their pricing due to interchange fees' fluctuating nature.

According to PYMNTS, Visa’s interchange adjustment can increase merchant card processing costs by $768 million, and the increase in Mastercard’s fee would cost them $383 million annually. So, the fees vary across card processor networks.

MSPs find it challenging to account for the variability of interchange fees and the variety of credit cards clients use for different transactions.

According to SpendMatters, Visa claims the U.S. credit interchange structure has stayed the same in the past ten years, whereas the published rates are higher, ranging from 2.5% to 4%.

Reports presented by the Merchants Payments Coalition show that though the cost of processing for these transactions has been reduced to half, the fees paid by merchants have not reduced.

Therefore, it is difficult to keep track of fee revisions and even know whether they have been applied to payments. Unexpected changes in MSP charges result in confusion and client dissatisfaction.

4. Profit Margins:

Interchange fee variations impact MSPs’ profit margins. According to MSP360, MSPs have an average profit margin of 8%, while it may go up to 18% for best-in-class MSPs.

The impact of interchange fees becomes greater with such slim profit margins. Every dollar is vital for your MSP's sustainability and growth, as even small fluctuations in these fees can significantly affect profits.

Each credit card payment by a client comes with an interchange cost that directly hits your profitability.

These expenses are unavoidable, and the most effective way to manage interchange fees is to include them in your prices.

However, you need to communicate this clearly to your clients to avoid hidden charges or sudden price hikes that may lead to dissatisfied clients.

5. Competitive Disadvantage:

High interchange fees reduce your MSPs’ competitive edge.

Let’s take the example of surcharging or passing through credit card processing fees to clients.

For instance, if an MSP charges 2.9% in processing fees, a client processing $100,000 a year would incur $2,900.

If a competitor MSP offers a fee of 2.5%, the same client would only pay $2,500, saving $400. This financial incentive can prompt clients to switch providers.

As explained below, you can pass on interchange expenses to clients through surcharging to avoid margin pressures. However, it is essential to remember that clients may switch to an alternative MSP if your pricing model is too high.

Therefore, you must work to lower the impact of interchange fees on your pricing.

6. Client Relations:

High costs due to interchange fees can impact your relationship with clients. The impact for MSPs is higher as most clients have a long-standing arrangement with you.

For example, increasing a client’s fee by 2% to cover the rising interchange costs will lead to an unexpected burden of $2,000 for a client processing $100,000 in a year.

If the expense remains unexplained, it can threaten your existing contract and the possibility of working together.

Sudden changes in pricing due to fluctuations in interchange fees can lead to misunderstandings and damage the client’s trust. Therefore, MSPS must communicate transparently about pricing structures and prioritize client relationships.

7. Regulatory Compliance:

Payment regulations and interchange fees vary across jurisdictions. Using payment solutions from large vendors does not guarantee PCI-DSS compliance to protect cardholder data.

Non-compliance leads to significant penalties, higher interchange fees, and damages to your reputation.

MSPs must monitor developments in PCI-DSS or changes in interchange fees for a jurisdiction to ensure adherence to compliance requirements.

Pick a payment software that ensures PCI compliance by completing the minimum level SAQ-A (Self-Assessment Questionnaire A).

8. Technological Requirements:

MSPs need robust payment processing systems to manage digital transactions and provide clients with payment options.

The system must accurately track and report interchange fees to help MSPs manage cash flow and forecast income.

It must also ensure compliance with PCI-DSS for credit card transactions to protect sensitive cardholder data and reduce the risk of breaches that can lead to increased fees or penalties.

9. Financial Forecasting Difficulties:

Card networks like Visa and Mastercard frequently adjust interchange fees. These changes can lead to potential cash flow issues and budget overruns for MSPs with large monthly transaction volumes.

Interchange fee structures include a percentage of the transaction amount plus a fixed fee, making it difficult for MSPs to forecast transaction costs accurately.

For instance, a $5,000 transaction with an interchange fee of 1.43% plus $0.10 costs approximately $71.60, which must be factored into financial projections.

However, since each client may use different credit cards, you must estimate the cash flow by calculating the exact percentage and fixed fee for each transaction.

9 Strategies to Minimize the Impact of Interchange Fees on MSPs

Interchange fees affect MSP's cash flow while impacting pricing transparency, profit margins, and client relations.

To overcome the financial hurdle, MSPs must adopt effective strategies that mitigate the influence of interchange fees on their overall operations.

Maintaining competitive pricing and positive relationships with clients while ensuring compliance with regulatory requirements is critical for MSPs.

Here are nine strategies to minimize the impact of interchange fees on MSPs

1. Opt for Payment Gateways Optimized for B2B:

Optimized B2B payment gateways facilitate secure digital transactions by eliminating the hassle of manual payment processing and ensuring PCI compliance.

These integrate with your accounting tools like QuickBooks Online, QuickBooks Desktop or Xero to streamline payment collection.

B2B payment gateways collect more detailed and secure transaction data to support Level 2 and 3 data. MSPs using these gateways improve cash flow by managing interchange fees.

For instance, IT Vortex, a NJ-based MSP, shifted from PayPal to FlexPoint’s passwordless branded client portal to eliminate the hassle of manually sending invoices and payment links.

PayPal complicated the client payment experience by redirecting them to a different website, which was time-consuming and confusing.

With FlexPoint, IT Vortex offered clients the convenience of the AutoPay feature via a secure payment portal. This allowed the company to save 60 hours per year and start receiving payments 30 times faster.

2. Encourage ACH Payments:

ACH (Automated Clearing House) payments provide a cost-effective alternative to credit card transactions as they typically have a flat fee.

According to PYMNTS, B2B ACH adoption in the US has grown by 12%, reaching 30 billion payments worth $77 trillion. They are suitable for automating recurring billings and subscription-based services.

According to GoCardless, ACH transactions have the lowest payment processing costs. If your business has a high sales volume, the savings from ACH transactions can improve your company’s bottom line.

For example, while credit card fees might cost 2.5% per transaction, ACH fees range from $0.20 to $1.50 per transaction.

For example, FlexPoint typically charges a flat fee of $0.25 per ACH transaction.

The fee does not depend on the transaction amount. A $1,000 transaction can save you money, as you pay $0.25 instead of an average of $30 on credit card payments.

While a transactional saving of around $30 may seem negligible, it is significant for MSPs that facilitate numerous transactions throughout the month.

The consistent savings from lower fees can accumulate quickly and be used for essential operational expenses.

3. Incorporating Surcharge Policies:

MSPs can opt for a surcharge on each credit card transaction to mitigate the impact of interchange fees on their profitability.

You can pass either the complete or partial interchange fee to your clients. It is important to notify your clients and leading credit card networks about the surcharge program.

Credit card surcharge regulations vary across the United States. Before considering this approach, it is essential to understand the legal implications in each respective state.

Some states like Connecticut, Maine, Massachusetts, and Puerto Rico completely prohibit surcharging. Others are lenient and states like Colorado permit surcharges of 2% or even the actual cost of processing.

Failure to comply with local surcharge regulations can lead to penalties and damage customer trust.

4. Set Up Recurring Billing Efficiently:

Recurring billing ensures consistent revenue, so your payment systems must facilitate the automatic processing of scheduled payments. It ensures uninterrupted service delivery and convenience, which enhances client satisfaction.

These systems must have stringent security measures, like PCI-DSS, to protect cardholder data. This prevents the risk of higher processing fees due to data breaches.

5. Implement Advanced Fraud Detection Tools:

Chargebacks occur when a customer disputes a transaction or due to credit card processing issues.

According to The Payments Association, 75% of chargebacks are accidental, and 34% are due to clients considering certain transactions fraud.

High chargeback rates can be damaging to your MSP. They impact your revenue and categorize your MSP as high-risk to payment processors and card networks.

The interchange fees for high-risk businesses are higher, so deploying sophisticated fraud detection systems helps reduce chargebacks.

For instance, you can use AVS (Address Verification Service) and CVV (Card Verification Value) to lower fraud risk and interchange fees. It offers encryption and tokenization, ensuring that sensitive information like CVV and billing addresses are securely transmitted and stored.

Improving chargeback management is a proactive approach that protects revenue and business relationships.

By maintaining lower chargeback rates, you keep your MSP's risk and interchange fees lower.

6. Educate Clients About Payment Impact:

Offer different payment methods and inform clients about the impact of each on the overall costs of the services you provide.

For instance, if you choose the surcharging option to pass on the burden of interchange fees, you must inform clients about the surcharge amount.

You must also explain the fees they must pay for convenience when using credit card payments.

By offering transparency regarding transaction fees, you can encourage clients to consider lower-cost alternatives to credit cards such as ACH.

Highlighting the differences in processing fees can help clients make informed decisions.

Providing a breakdown of costs associated with various payment methods improves the reliability of your MSP.

7. Negotiate Terms Based on Volume:

MSPs process high volumes of monthly credit card transactions and represent a significant revenue stream for payment processors. The transaction volume can help you negotiate for reduced interchange fees.

While interchange fees are not negotiable, MSPs can significantly reduce their overall payment processing costs by focusing on the markup imposed by payment processors.

For instance, if an MSP processes a substantial volume of transactions, it can be used to negotiate a more favorable markup.

Interchange fees are a percentage of the credit card transaction amount, so even a small decrease in interchange rates can save thousands of dollars annually.

You can also provide additional information about transactions, such as item descriptions and tax rates, known as Level 2 and Level 3 data, to qualify for lower interchange fees.

8. Use an Integrated Payment Processing Solution:

Implementing an MSP-specific integrated payment processing solution streamlines the payment workflow and provides deep insights into cash flow. It consolidates accounting, invoicing, payment, and reconciliation functionalities to speed up payment processing.

An integrated payment processing solution also optimizes card-accepting procedures to reduce processing costs. With automated invoicing features, MSPs can ensure timely payments and minimize the risk of late fees, which result in additional interchange fees on the transactions.

These systems also help implement surcharging by automatically adjusting the surcharge to the transaction amount. It also considers the applicable regulations for each state, ensuring compliance with local laws.

Advanced payment processing solutions also help securely collect Level 2 and Level 3 data, which can help your MSP qualify for lower interchange fees.

9. Offer Payment Incentives:

Incentivizing clients to use lower-cost payment methods can help reduce processing fees.

For instance, offering discounts to clients who choose bank transfers instead of credit card payments can motivate them to choose this more cost-effective method.

MSPs could implement a pricing model in which clients receive a percentage off their monthly bill if they pay via ACH, direct debit, or other lower-cost options.

Providing small discounts for payments made through direct bank transfers encourages customers to pay faster and eliminates interchange fees.

Conclusion: Managing Interchange Fees for Better Financial Health

MSPs cannot avoid interchange fees but must manage them to reduce their financial burden. This is necessary to improve cash flow, maintain competitiveness, and ensure better business relationships with clients.

You can reduce interchange fees through strategies such as:

- Negotiating terms (processor markup fees) based on credit card transaction volume

- Implementing fraud detection tools

- Educating clients about alternate payment options

- Setting up efficient recurring billing systems

By incentivizing clients to use lower-cost payment methods, you can reduce processing fees and maintain transparency in pricing. It allows clients to select their preferred payment method while safeguarding your MSP against potential losses caused by chargebacks.

An integrated payment processing solution streamlines the billing process and cash flow. It helps you proactively manage interchange fees through advanced payment processing and reconciliation tools.

FlexPoint’s payment solution offers a suite of tools to effortlessly manage client payments. The advanced payment processing technology helps maintain fee transparency with surcharge automation.

FlexPoint's fee structure helps MSPs pass on interchange fees as a whole or as a percentage to their clients. Thus, MSPs get the best credit card processing pricing without compromising quality.

FlexPoint manages recurring billing by offering clients low-fee options like ACH payments. The customer-centric solution helps your clients choose flexible payment options, AutoPay, and one-click payments for added convenience.

With our PCI-DSS-compliant solution, you can reduce the risk of fraud, save time from manual payment processes, and increase client satisfaction by providing a seamless payment experience.

Optimize your payment processes with FlexPoint's advanced solutions. Reduce the impact of interchange fees and enhance your MSP's financial efficiency.

Visit our website or schedule a personalized demo today to learn how we can help you manage costs and improve your bottom line.