According to EMARKETER, 32.1% of B2B payments in the U.S. are still made using traditional methods, such as checks and cash. Checks require manual handling, which can often delay payments due to lengthy approval processes at the client's end and prolonged bank payment processing.

Paper checks also expose sensitive financial data to risks of breach and forgery. Digital payments are replacing paper checks, which are slow, costly, and prone to errors. Sticking with checks can leave MSPs at a disadvantage as clients increasingly seek faster and more secure payment methods.

According to a survey by the Association of Financial Professionals, 73% of organizations are switching from paper checks to electronic B2B payments, with 92% prioritizing efficiency.

In this article, we will help MSPs to modernize their payment workflows away from checks. We will examine the hidden costs and operational drawbacks of check-based payments, including time-consuming reconciliation and associated risks of fraud.

We'll also explore alternative payment options tailored for MSPs and provide a step-by-step strategy to transition your MSP to digital payment workflows.

Why MSPs Are Moving Away from Checks?

According to Paystand, processing a single check costs $4 to $20. Collecting large volumes of payments through checks regularly is time-consuming, expensive, and inefficient for MSPs. Therefore, transitioning away from checks can significantly improve business operations and customer satisfaction.

MSPs should transition away from checks as they no longer fit today's fast-paced and digital-first payment needs. Clients expect a variety of payment options, and MSPs need to collect payments securely. Checks, on the other hand, create bottlenecks that can frustrate your clients and their finance (accounts payable) teams.

Paper checks slow down your MSP's cash flow, as they can take an average of 14 days for approval and longer to process, delaying the availability of funds. The unpredictability complicates financial forecasting and strains working capital.

Checks also consume a significant amount of administrative resources and time, as your staff manually processes, deposits, and reconciles payments. Reconciliation and resolving disputes are also costly and require rework.

Checks lack visibility and real-time tracking, making it hard for MSPs to manage receivables and follow up on payments. They also pose security and compliance risks by exposing sensitive bank details to fraud.

Additionally, MSPs risk losing clients and facing financial strain by relying on checks rather than adopting digital payment methods.

The Hidden Costs and Risks of Paper Check Payments

Paper checks may feel like a familiar and straightforward payment method, but they come with hidden costs and risks. Delayed cash flow and fraud vulnerabilities make collecting payments through checks inefficient and costly over time.

For example, an MSP processing 50 checks a month could lose hundreds of hours yearly on manual tasks, face revenue delays, and risk fraud-related losses. As your MSP scales, staying competitive with traditional payment methods in a digital-first world becomes increasingly challenging.

Here is how relying on checks affects your MSPs' efficiency and bottom line:

1. Delayed Payments

According to Treasury Today, check payments may take up to 30 days to clear. Paper checks slow down the payment process at every step. Clients must print, sign, and mail checks, which can take days to arrive. Once received, MSPs need to deposit them, and banks take several business days to clear the payments.

Payment delays disrupt cash flow, making it difficult to cover expenses such as payroll or vendor payments, which can lead to a cash crunch. Payment delays make it hard for MSPs to forecast finances, as unpredictable timelines disrupt revenue planning.

Payment delays compound into significant financial leakage over time. For example, if an MSP processes 50 checks per month, each delayed by an average of 10 days, thousands of dollars can remain tied up and unavailable for business needs. These cash flow constraints interrupt operations and strain client relations.

2. Manual Reconciliation

According to Gitnux, 43% of companies struggle with B2B payment reconciliation. Manually reconciling check payments is time-consuming and prone to errors, as staff must match checks to invoices, verify amounts, and update bank records accordingly.

Matching checks received with invoices and verifying payments is prone to errors in billing. Incorrect amounts or duplicate entries can disrupt financial records. Fixing mismatched invoices or incorrect amounts requires rework, which slows down the payment cycle and strains client relations.

For MSPs handling high volumes of checks, manual reconciliation is a labor-intensive process that requires substantial staff time and resources. It diverts resources from strategic tasks, leading to inefficiency and high operational costs.

Over time, the administrative burden leads to delays in financial reporting, impacts decision-making, and hinders your MSP’s productivity and growth. You can avoid errors and high reconciliation costs by moving away from checks.

3. Security and Fraud Risks

According to a survey by the Association of Financial Professionals, 63% of organizations faced check fraud in 2024. Paper checks risk exposing sensitive financial data, such as bank accounts and routing numbers, which can be intercepted during transit or due to mishandling by staff. For MSPs, even a single fraudulent transaction can harm client trust and financial stability.

Additionally, checks require manual handling and physical storage, making them vulnerable to damage or loss from natural disasters or theft. Unlike secure digital payments, stolen checks can be altered or forged. Recovering funds from lost checks is expensive and time-consuming, which impacts your MSP's bottom line.

Paper checks complicate tracking payments or detecting inconsistencies from the clients’ side. There is a risk that the client or their accounts payable team may miss the payment deadline or mention incorrect amounts. Regularly missed or mismatched payments will impact your MSP's profitability in the long run.

4. Labor Costs

Processing paper checks requires a significant amount of staff time, which increases labor costs. MSP finance/accounting teams must open mail, log payments, and, in some cases, visit the bank to present checks, then reconcile accounts with the payment data. According to KlearStack, finance teams spend 30% of their time on reconciliations.

If your MSP processes 50 checks monthly, a finance staff member might spend 10-15 hours a week processing and reconciling paper checks. If the employee works at an average salary of $30 per hour, your MSP bears a labor cost of $450–$600 per month or up to $7,200 per year.

Manual check processing can be a burden for your MSP finance team. Fixing errors and manually reconciling payments leads to employee burnout from repetitive tasks, diverting time away from more strategic or value-added activities. By moving away from checks, MSPs reduce operational costs and enhance efficiency, ensuring that resources are used optimally.

Top 4 Digital Payment Alternatives to Paper Checks

Moving away from checks doesn't mean sacrificing client convenience or complicating payment collections. Instead, it must be a reliable and scalable payment method that aligns with your MSP's operations.

Digital alternatives, such as ACH transfers, credit card payments, client portals, and automated invoicing, enable MSPs to streamline their cash flow, reduce manual work, and enhance security. You must select a payment method that ensures fast and secure transactions to eliminate the inefficiencies associated with paper checks.

Here are the top digital payment alternatives to paper checks that can be tailored to your MSP workflows:

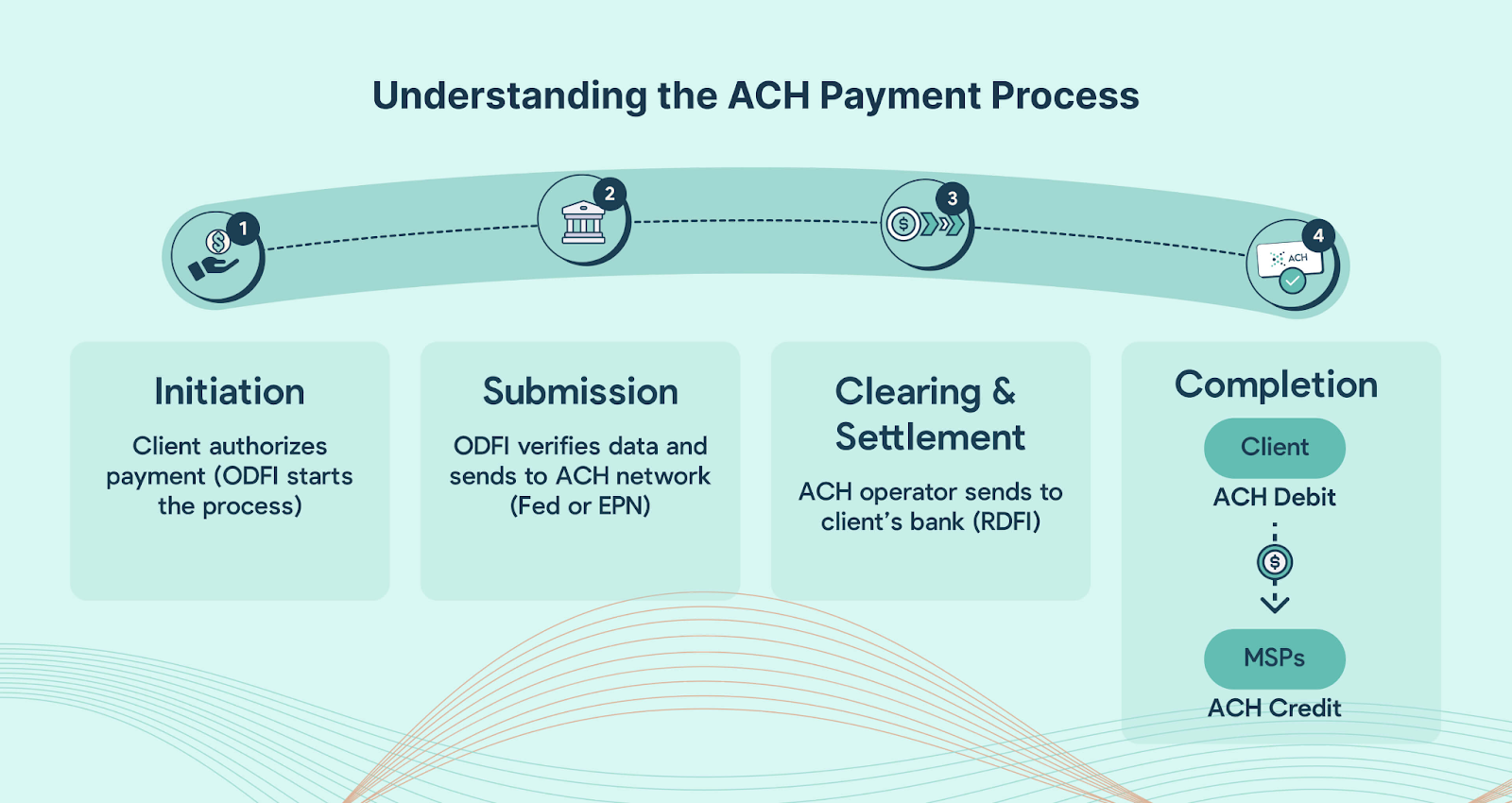

1. ACH Transfers

ACH (Automated Clearing House) transfers are electronic payments that move funds between bank accounts. Clients authorize the MSP to debit their accounts for invoices, either as one-time or recurring payments. ACH payments are processed under strict rules, ensuring reliability and compliance.

ACH transfers are ideal for high-value or recurring payments. They cost less ($0.25 to $1.00 per transaction) than credit card transactions (anywhere from 2% to 4%), as you must pay a flat fee rather than a percentage. They are also secure compared to paper checks, as funds are deposited directly into the MSP's account.

Additionally, Same-day ACH speeds up cash flow, reduces payment delays, and eliminates chances of lost payments.

ACH is best suited for recurring billing scenarios with predictable cash flow. It is ideal for MSPs seeking low-cost and secure payment options that enhance financial stability.

2. Credit Card Payments

Credit card payments offer clients a quick and convenient way to settle invoices using major credit cards, including Visa, Mastercard, and American Express.

MSPs can integrate secure payment gateways to handle transactions, with funds typically deposited within one to three business days. These systems also support features such as securely storing card details for recurring payments, which simplifies the process for clients and MSPs.

Credit cards offer MSPs faster payments, improved cash flow, and enhanced client satisfaction.

Some U.S. states permit MSPs to add surcharges to cover credit card processing fees, thereby helping MSPs recover costs and protect their profit margins.

Credit cards are well-suited for collecting payments for project-based work, recurring payments, or even ad-hoc services. Use credit card payments for clients who value flexibility.

3. Client Payment Portals

Client payment portals are branded payment tools offered as a feature of an MSP-specific billing automation platform. They allow clients to view invoices, select payment methods (ACH, credit card, or flexible financing), select accounts for AutoPay, and manage their billing preferences.

Payment portals help MSPs save time, enhance transparency, and streamline their billing processes. They enable clients to self-manage payments, reduce client queries about payment status, and eliminate the need for manual follow-ups.

The AutoPay feature enables faster payments, reduces disputes, and provides a professional client experience while minimizing administrative workload and errors for MSPs.

Client portals enable MSPs to enhance the client experience and streamline their operations. They are most suitable for recurring or complex billing for multiple clients. It also supports multiple payment methods, allowing clients to pick a preferred method.

4. Automated Invoicing & Payment Reminders

Automated invoicing systems simplify billing by creating and delivering invoices on a schedule based on client contracts or in real-time upon project milestone completion, when integrated with time tracking tools and a PSA system.

Automated invoicing platforms also send payment reminders and often integrate with accounting tools (such as QuickBooks Online, QuickBooks Desktop, Xero) for real-time data syncing.

Automation reduces payment delays by minimizing errors, streamlining invoicing, and eliminating manual tasks. It standardizes billing and provides real-time visibility into payment status, helping MSPs manage their accounts receivable better and forecast revenue.

Automated invoicing and reminders help MSPs scale by reducing admin work and ensuring consistent cash flow. They are helpful for MSPs delivering recurring services, handling high volumes of invoices, or managing complex billing scenarios.

How to Seamlessly Transition Away from Checks as an MSP

Transitioning away from checks is crucial for MSPs to stay competitive in a digital-first world. However, you shouldn’t instruct clients to stop paying by check abruptly. A phased and well-communicated transition is crucial to maintaining trust and minimizing disruption.

By transitioning to digital payments, such as ACH or credit cards via secure client portals, MSPs can reduce the delays, costs, and risks associated with checks while meeting client expectations for fast and secure transactions.

A well-planned transition preserves cash flow, reduces manual work, and positions MSPs for growth without alienating clients or overwhelming staff.

Here is a step-by-step guide for MSPs to transition away from checks effectively:

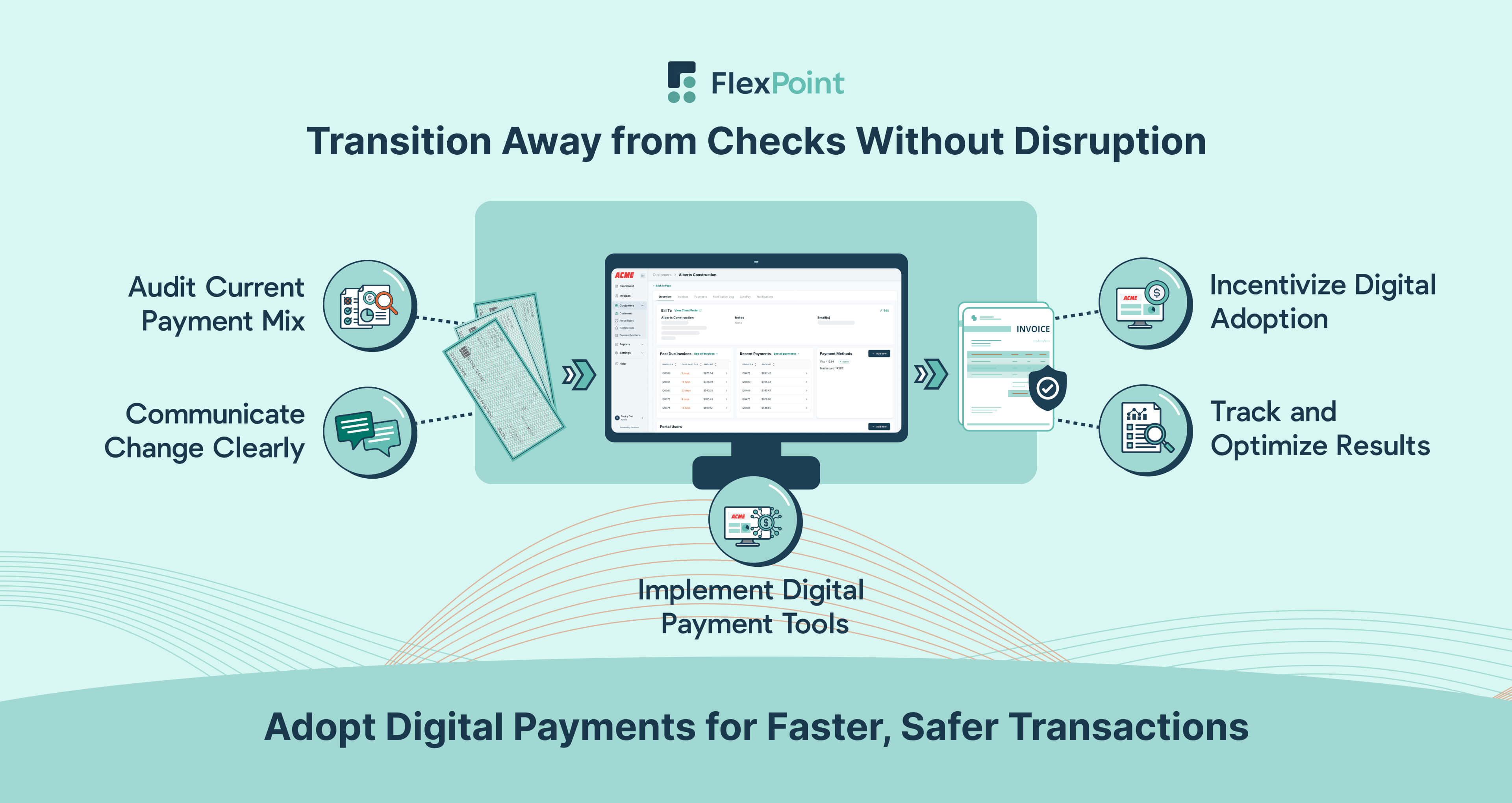

Step 1 – Audit Your Current Payment Mix

Review your current payment methods to determine how much you rely on checks and the associated processing costs. Study your client behavior to identify who pays by check, how often, and for what services.

For example, labor costs from processing checks would be higher compared to ACH transactions.

Utilize your PSA (such as ConnectWise, Autotask, SuperOps, HaloPSA) or accounting software to extract payment data and identify inefficiencies. The audit will help you prioritize which clients to transition first and set a benchmark for measuring progress.

Step 2 – Communicate the Change Clearly

Inform clients early and clearly about the shift to digital payments to maintain trust and encourage adoption.

Utilize multiple communication channels, such as email, messaging, or phone calls, to explain the benefits of transitioning away from checks. Clear communication will help clients transition smoothly while maintaining trust in your MSP.

Speed up transitions to alternatives to paper checks by showing the clients how it will lead to faster payment processing, enhanced security, and greater convenience for them.

Share a clear timeline and be transparent about any potential impacts on the client's current payment routines.

Support clients during payment method changes by providing them with resources and information to facilitate adjustments.

Answer common objections and questions, arrange walkthroughs, and address client concerns to prevent dissatisfaction or churn due to a change in payment method.

Step 3 – Implement Digital Payment Infrastructure

A robust infrastructure minimizes disruptions and facilitates easy digital payments for clients. Set up the tools needed to enable secure, efficient, and user-friendly transactions before phasing out checks.

Ensure the payment collection system supports multiple payment options, including credit cards, ACH, and flexible financing via white-label client portals, to cater to the diverse needs of clients. Select a unified platform that integrates with your PSA, such as ConnectWise, or an accounting software like QuickBooks Online, to streamline onboarding and ensure a seamless data flow.

Test the system with a small group of clients to identify and resolve any issues that may arise.

Train your staff to handle inquiries and troubleshoot common problems related to the new payment system.

Step 4 – Incentivize the Shift Away from Checks

Providing a smooth and rewarding transition experience will help build trust and drive adoption rates. Encourage clients to switch to digital payments by offering incentives that make the change appealing. These could include discounts on their next invoice, waived fees, or enhanced service features.

For example, you can offer a 1-2% discount on ACH payments, which are less expensive than paper checks, or waive setup fees for clients who enroll for AutoPay.

Additionally, consider emphasizing the cost benefits, ease, and security of paying through the new system to further persuade hesitant clients.

Communicate the incentives clearly through emails, newsletters, or direct calls with account managers, ensuring clients understand the value of making the switch.

Highlight convenience perks, such as easy access to payment history in a branded portal or being notified of upcoming payments.

Step 5 – Track and Optimize Adoption

Monitor the adoption rates closely to identify trends and potential barriers faced by clients. For example, if only 60% of clients switch after 30 days, follow up with non-adopters via personalized emails or calls, offering support or additional incentives.

Utilize analytics to monitor adoption rates, including the percentage of clients using ACH or credit cards. These insights will help you design client-friendly payment processes and incentive strategies to improve the adoption of your new payment system.

Consider implementing periodic surveys or feedback forms to collect direct input from clients. Continuously optimize messaging and workflows based on client feedback, such as simplifying portal login steps.

How FlexPoint Supports MSPs in Moving to Digital Payments

FlexPoint offers an all-in-one platform designed specifically to help MSPs streamline their payment collection.

By integrating ACH, credit card processing, branded client portals, and invoice automation into a single system, FlexPoint streamlines the transition from checks, enhancing efficiency and client satisfaction.

The platform's robust features address the key pain points of check-based payments, including manual processes, tedious reconciliation, and delayed cash flows.

FlexPoint empowers MSPs to meet client expectations for fast, secure transactions. Its user-friendly design ensures quick onboarding, making it easy for your staff and clients to adopt digital payments without disruption.

Here are the key capabilities of FlexPoint that help MSPs transition to a no-checks future:

- ACH and Credit Card Processing: FlexPoint enables MSPs to accept both ACH and credit card payments within one system, eliminating the need to manage multiple processors. FlexPoint helps MSPs comply with surcharging regulations and PCI-DSS requirements, reducing financial and legal risks.

- Client Portals: FlexPoint's branded client portals help reduce payment friction by allowing clients to view invoices, choose payment methods, and set up AutoPay with ease. Client portals enhance transparency and the client experience by allowing clients to manage their payments independently. It also reduces the number of inquiries that need to be handled by the finance team.

- Automation and Reminders: FlexPoint automates invoicing and payment reminders, generating invoices based on contracts and sending them on schedule. Overdue payments trigger automated reminders, nudging clients to pay without staff intervention. Automation ensures consistent cash flow and frees staff to focus on strategic tasks.

- Integrated Reconciliation: FlexPoint synchronizes transactions with PSA (such as ConnectWise, Autotask, HaloPSA, and SuperOps) and accounting platforms (including QuickBooks Online, QuickBooks Desktop, and Xero); thereby eliminating the need for manual data entry and ensuring seamless integration. Payments are automatically matched to invoices, reducing errors and the time required for reconciliation. The integration provides real-time visibility into receivables, enhancing accuracy and forecasting capabilities.

FlexPoint simplifies and modernizes payments for MSPs by consolidating all your payment needs into one platform. The scalable and growth-focused digital payment platform streamlines cash flow management, enhances visibility, and increases control over payment workflows.

Conclusion: Build a Future Without Checks for Your MSP

Paper checks are outdated and costly for modern MSPs. They slow cash flow, require manual reconciliation, and risk data fraud. These inefficiencies, combined with high labor costs, hinder your MSP’s growth and frustrate clients expecting fast and secure payment options.

Digital payment methods are crucial for MSPs seeking to streamline operations and improve client satisfaction. With features like ACH transfers, credit card payments, and automated invoicing, they offer faster, safer, and more efficient solutions. These tools reduce admin tasks, improve cash flow visibility, and meet client demands for convenience, making them crucial for scaling and staying competitive.

Switching to modern payment processes doesn't have to be overwhelming. With the right tools and strategy, you can upgrade without disrupting clients or overloading your team.

FlexPoint makes it easy for MSPs to transition from traditional billing to modern payment methods.

With features such as secure digital payments, client portals, invoicing automation, and automated deposit reconciliation, FlexPoint streamlines billing workflows, saves time, and enhances accuracy. It’s an all-in-one platform that integrates with your MSP's PSA system and accounting software to build a scalable, future-ready payment solution that improves efficiency and client satisfaction.

Ready to stop chasing paper checks?

Schedule a demo and take the first step toward eliminating checks from your workflow.

%20(1).jpg)