Credit card chargebacks are a persistent challenge for managed service providers (MSPs) and their finance teams. A chargeback occurs when a client disputes a payment through their credit card issuer, potentially forcing an MSP to refund the charge. These disputes can drain revenue, disrupt cash flow, and consume hours of administrative work.

U.S. consumers disputed over $65 billion in credit card charges in 2023 alone, underscoring how common (and costly) chargebacks have become.

For MSPs, chargebacks often stem from clients contesting recurring service fees or misunderstanding invoice charges—issues that can escalate if not managed proactively.

In this article, we’ll explain what chargebacks are, why MSPs are especially vulnerable to them, and how they impact your business’s bottom line. More importantly, we’ll outline seven proven strategies tailored for MSPs to prevent chargebacks before they happen, and how to respond effectively if a dispute does occur.

By implementing these practices (and leveraging tools like automated MSP payment solutions), MSP owners and financial officers can reduce chargeback risks and maintain stable, predictable payments.

{{toc}}

What Are Credit Card Chargebacks?

A credit card chargeback is a forced reversal of a transaction initiated by the cardholder’s bank. In simple terms, it’s like an “involuntary refund” triggered when a customer disputes a charge on their statement.

The card issuer (usually the bank) investigates the claim and, if it deems the dispute valid, the payment gateway or the bank withdraws the funds from the merchant’s account and returns them to the customer. For MSPs, this means a client has formally challenged a payment for your services through their bank, rather than requesting a refund directly from you.

Chargebacks can happen for a variety of reasons:

- Unrecognized Charges: The client doesn’t recognize the billing descriptor on their statement and believes the charge is fraudulent or mistaken. (This is common—one report from Ethoca and Aite found 73% of customers will contact their bank first upon seeing an unfamiliar charge, often skipping any discussion with the merchant.)

- Service or Product Disputes: The client feels that the service wasn’t provided, did not meet expectations, or was unsatisfactory, so they seek to reverse the charge.

- Unauthorized Use: The client claims the charge was made without their permission (for example, due to a stolen card or an employee exceeding authority).

- Billing Errors: Duplicate charges or incorrect amounts can prompt a client to dispute the transaction.

It’s essential to recognize that chargebacks were initially a consumer protection mechanism – a means to prevent cardholders from being held liable for fraudulent transactions or merchant errors. However, they are increasingly used in scenarios where the purchase was legitimate.

“Friendly fraud,” in which a client disputes a valid charge (often because they don’t remember or recognize it), now accounts for the majority of chargebacks. Visa estimates that friendly fraud can make up up to 75% of all chargebacks. In other words, most chargebacks are not due to actual criminal fraud, but rather misunderstandings or miscommunications.

For MSPs, every chargeback triggers a formal process with strict rules. Once a dispute is filed, the MSP’s payment processor typically pulls the disputed amount from the MSP’s account immediately and levies a chargeback fee.

For example, Mastercard estimates that each dispute incurs operational costs of $15 to $70 for both the issuing bank and the merchant.

The MSP then has a limited window to respond with evidence if they want to challenge the chargeback. If the case isn’t resolved in the MSP’s favor, the client retains the refunded money, and the MSP absorbs the loss, plus any associated fees.

This process is more complex and damaging than a simple refund request made directly to the MSP.

In the following sections, we’ll explore why MSPs are particularly vulnerable to these disputes and the toll chargebacks can take on your operations.

{{ebook-cta}}

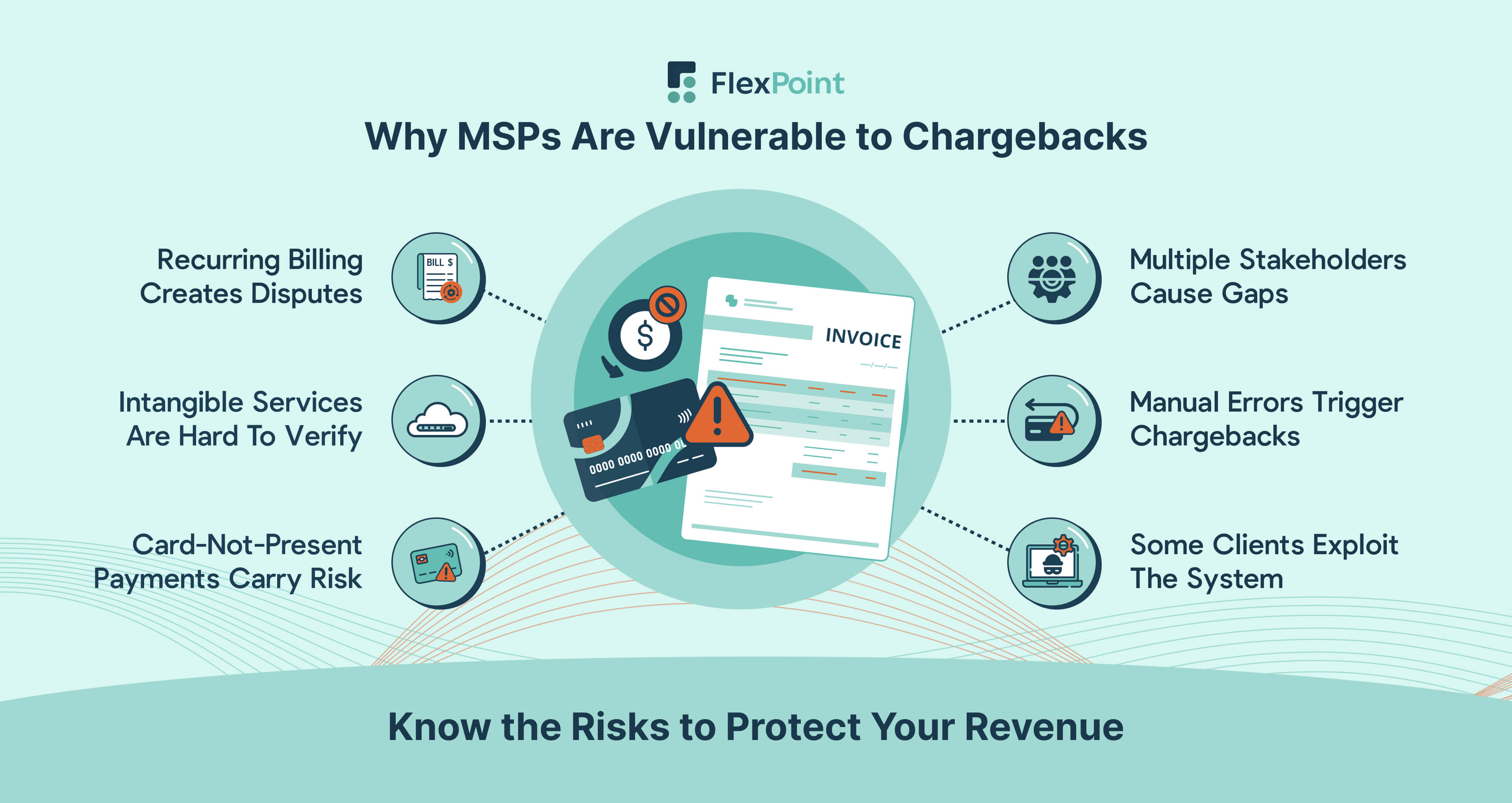

Why MSPs Are Vulnerable to Chargebacks

Chargebacks can hit any business, but MSPs face unique circumstances that make them more susceptible to disputes.

Understanding these factors is the first step to prevention:

1. Recurring and Subscription Billing

Many MSPs charge clients on a recurring payment or quarterly cycle for ongoing services. If a client forgets about an upcoming charge or isn’t clearly reminded, they might see the auto-billed amount on their credit card and panic.

Regular, automatic payments without clear communication can lead to “friendly fraud” disputes (“I don’t recall approving this charge, so it must be wrong”).

2. Intangible Services and Long Service Cycles

Unlike a product that the client holds in hand, IT services or software updates are not always immediately visible. A client might not fully understand or remember the value delivered in a given month.

This intangible nature means that if there is any dissatisfaction or misalignment of expectations, a client could file a chargeback, claiming that services weren’t delivered as promised. MSP contracts can be complex, and any service misunderstanding can quickly escalate to a dispute if not managed.

3. Card-Not-Present Transactions

MSP payments are typically taken online or via stored cards (card-not-present), rather than swiped in person.

Card-not-present transactions inherently carry a higher risk of fraud and chargebacks compared to card-present sales. There’s no physical signature or chip verification, so banks tend to side with the customer if they claim fraud.

As a result, even a totally legitimate MSP charge can be reversed if the issuer isn’t convinced by the evidence.

According to some data, the fraud rate for in-person card-present transactions is estimated to be 0.06% of the transaction value, and card-not-present fraud rates are estimated at around 0.93% of the transaction value, which is almost 90% higher.

The rise of ecommerce-style payments for services has coincided with a surge in chargeback rates.

For instance, according to Chargebacks911, ecommerce chargeback rates increased by 222% between early 2023 and 2024, reflecting the higher risk of disputes in remote transactions.

4. Multiple Stakeholders and Communication Gaps

In B2B settings, such as MSP-client relationships, the person approving the work (e.g., an IT manager or office admin) may differ from the person authorizing the invoice (e.g., a CFO or accounts payable).

If there is poor internal communication on the client’s side, the finance person may not recognize a charge and initiate a dispute. An MSP might also find that a client’s employee who authorized a project left the company, and their replacement questions the invoice.

This lack of continuity can trigger chargebacks simply because the new approver is unaware of the prior agreement.

5. Slim Margins and Manual Processes

Many MSPs are lean operations without dedicated billing specialists or advanced payment systems. A small mistake, such as billing the wrong amount or using an outdated card on file, can prompt a client dispute.

Because MSP teams are busy focusing on service delivery, they may not notice warning signs of client dissatisfaction or confusion about bills until a chargeback occurs.

Manual invoicing errors or failing to address client billing questions promptly can lead to increased dispute rates.

6. Opportunistic Clients

Unfortunately, MSPs can sometimes encounter clients who know how to game the system.

For example, a client might receive extensive support or project work, then file a chargeback to avoid payment (essentially getting free services). While this isn’t the norm, it can be financially devastating to an MSP when it does happen.

Service businesses often lack physical proof of delivery, making it challenging to contest “chargeback fraud” cases without thorough documentation. Every MSP should be aware of this worst-case scenario and take steps (like written approvals and logs) to protect themselves.

The Financial and Operational Impact of Chargebacks on MSPs

Every chargeback is more than just a refund; it’s a direct hit to your MSP’s financial health and efficiency.

Here’s how chargebacks can hurt your business:

1. Revenue Loss and Fees

When a chargeback occurs, you risk losing revenue from the disputed service and incurring additional fees.

Not only is the original payment (say, a $3,000 project fee) pulled out of your account, but you’ll also be charged a non-refundable chargeback fee by your payment processor.

2. Cash Flow Disruption

Chargebacks introduce uncertainty into your cash flow.

Once a chargeback is initiated, the funds are in limbo (essentially gone) until the case is resolved, which can take weeks or even months. For an MSP, that might mean missing money to pay your technicians or cover your own vendor bills this cycle.

3. Operational and Administrative Costs

Handling chargebacks is labor-intensive. Your team must review contracts, service logs, emails, and any other relevant evidence to contest the claim, all within a tight deadline. This time could have been spent on billable work or improving your services.

4. Processor Relationship and Reputation

Payment processors/gateways and banks track your chargeback ratio (the percentage of transactions that result in chargebacks). Too many disputes and you’ll earn an unwelcome label: “high-risk merchant.”

Typically, card networks consider a chargeback rate above ~1% of transactions as a red flag. Exceeding this threshold can trigger warnings, higher processing fees, or even formal monitoring programs by Visa or Mastercard.

For example, PayPal considers merchants with over 1.5% chargebacks (and at least 100 disputes) as “high volume” dispute merchants and doubles their dispute fee from $15 to $30.

In extreme cases, acquiring banks can terminate your ability to process credit cards if chargebacks remain excessive. Losing card processing privileges would be a devastating blow to any MSP’s operations.

5. Client Relationship Damage

A chargeback typically indicates that the client was unable to resolve the issue directly with you. That’s a sign of eroded trust.

Once a client goes to their bank, the relationship often deteriorates – you may lose the client entirely, even if you win the dispute.

7 Proven Strategies to Prevent Credit Card Chargebacks in Your MSP

Chargebacks might seem unpredictable, but in many cases, they’re avoidable with the proper practices.

Below are seven proven strategies for MSPs to prevent chargebacks before they happen.

Each strategy targets common causes of disputes, helping you safeguard your revenue and keep clients informed and satisfied.

1. Use Clear and Detailed Billing Descriptions

One of the simplest yet most effective ways to prevent “friendly” chargebacks is to ensure your billing is crystal clear.

Many disputes occur simply because a client doesn’t recognize a charge on their card statement or invoice.

To avoid this, use explicit, detailed descriptors for every billing entry:

a. Identify Your Business Prominently

Make sure the name that appears on clients’ credit card statements is obviously associated with your MSP.

If your legal business name is different from your trade name, consider adding an identifier.

For example, instead of “ABC LLC,” use “ABC Tech Services” on the descriptor so clients instantly recall who you are.

b. Add Details about the Service or Period

Include specifics like the service period, contract name, or project reference on invoices (and in any description that goes to the client). “Monthly IT Support – March 2025” is far more informative than “Service Fee 3/1.”

c. Avoid Abbreviations and Codes

Don’t make clients decipher cryptic billing codes.

Aite Group research data, published by Corepay, found that unclear shorthand on statements (e.g., ##MSP*093 instead of a readable name) leads consumers to assume a charge is fraudulent.

When transaction descriptions were clarified, some banks saw a 30% reduction in customers disputing charges they initially thought were illegitimate.

d. Leverage Client Portals

If you use a client billing portal (like the FlexPoint platform’s branded client portal), encourage clients to log in and view full invoice details and history. A portal provides a clear record of what was billed and when, reducing confusion.

FlexPoint’s brand client payment portals ensure comprehensive documentation of all charges for both you and the client, so there’s less room for “I didn’t know what this charge was” disputes.

By providing detailed and transparent billing information, you preempt many chargebacks.

2. Set Transparent Payment Terms and Communicate Proactively

Ensure every invoice you send is accurate and detailed. Billing errors or vague descriptions can easily trigger payment disputes.

Implement a quality control step (or utilize automated invoicing tools) to minimize payment errors.

According to data from the Institute of Finance & Management, 12.5% of manual invoices contain errors.

Each invoice should clearly itemize the services provided, including the dates and charges, so clients can immediately recognize what they’re paying for.

Providing this level of detail makes it much less likely that a client will question a bill.

Additionally, maintain organized records (such as contracts, work orders, and approvals) for each account. If a chargeback is filed, this documentation becomes your evidence to refute the claim.

3. Obtain Explicit Authorization for All Charges

One of the most compelling pieces of evidence in a chargeback dispute is proof that the client authorized the charge.

Authorization is key to preventing disputes, especially for recurring or one-time hefty charges. Require signed contracts or payment authorization forms that outline approved billing methods and schedules.

For recurring payments, obtain written consent (or digital acceptance) stating the client agrees to automatic billing.

For ad hoc charges, such as project fees or hardware purchases, confirm by email or ticket comment that the client agrees to the cost before charging. Documented approval makes it much easier to win chargeback disputes and discourages clients from disputing charges they knowingly authorized.

4. Maintain Thorough Service Logs and Documentation

Detailed documentation is an MSP’s best friend when it comes to preventing and fighting chargebacks, especially those claiming “services not provided” or “not as described.”

By keeping meticulous records of the work you perform and the communications you have, you create a factual trail that can avert disputes or swiftly resolve them in your favor.

Use your PSA (Professional Services Automation) or ticketing system (such as ConnectWise, Autotask, SuperOps, or HaloPSA) to log every service event, including support tickets, maintenance visits, software deployments, and more. Include timestamps, the service technician's name, and a description of the action taken.

Suppose a client ever questions whether a service was provided. In that case, you can refer to a log that shows, for example, “Backup configuration completed on 4/10 at 3:00 PM, confirmed by client via email.”

This level of detail can discourage a client from even attempting a “service not rendered” claim once they are reminded of the records.

5. Offer a Clear, Client-Friendly Dispute Resolution Process

Encourage clients to come to you first with any billing questions or concerns. Having a well-defined and easy-to-access dispute resolution process can prevent many chargebacks from being filed.

Display contact information clearly on invoices and payment portals so clients know where to go with any issues. Make it easy for them to reach out, and respond promptly and professionally when they do.

Often, clients initiate chargebacks out of frustration or feeling unheard; resolving disputes internally retains revenue and builds trust. This approach allows you to clarify charges, correct errors, or offer solutions before the bank becomes involved.

6. Monitor for Fraud and Use Secure Payment Processing

Not all chargebacks are “friendly.” Some are the result of actual fraud. For example, a stolen credit card is used to pay an MSP’s invoice, which the actual card owner later disputes.

Additionally, poor security practices can lead to data breaches or unauthorized charges, which can result in chargebacks. MSPs must stay vigilant about payment security and fraud prevention to avoid these scenarios.

Use a payment processor or gateway that offers fraud screening. Tools like Address Verification Service (AVS) and Card Verification Value (CVV) checks on transactions add an extra layer of validation.

AVS compares the billing address given with the one on file with the card issuer, while CVV verifies the 3-4 digit code. Enabling these can dramatically reduce fraudulent transactions and chargebacks.

Many modern payment solutions (including FlexPoint) integrate such checks by default for online payments.

7. Track Your Chargeback Ratio and Act on Warning Signs

What you don’t measure, you can’t manage.

Staying on top of your chargeback ratio (the percentage of your transactions that result in chargebacks) is crucial for early detection of problems and maintaining a healthy merchant account. Make it a habit to monitor and respond to chargeback trends in your Managed Service Provider (MSP).

Most processors or merchant portals will show you this, but you can calculate it easily:

(Number of chargebacks in a month) ÷ (Number of total transactions in that month) * 100%.

For example, two chargebacks out of 400 transactions is a 0.5% ratio.

Keep a log of this each month so you can spot upward trends. Even a subtle increase from 0.2% to 0.5% is worth investigating before it gets worse.

How to Respond to a Chargeback Dispute as an MSP

Even with the best preventive strategies, you may still occasionally encounter a chargeback. How you respond can make the difference between recovering your revenue or permanently losing it (along with the client).

Here are practical steps for MSPs to respond to a chargeback dispute effectively:

1. Identify The Chargeback Reason Code

Receiving a chargeback notification can be frustrating, but it’s important to approach it methodically.

First, note the chargeback reason code and any details provided by the customer’s bank. The reason code (like “Service not as described” or “Unauthorized charge”) will tell you why the client claims they disputed the charge.

This information guides your response. Also, check the date and amount of the transaction in question – identify which client and invoice this pertains to in your system. Keep emotions out of it; treat it as a business process that now needs your attention.

2. Collect Relevant Documentation

Refer back to your records for that client and transaction:

- Refer to the contract or service agreement to confirm the terms agreed upon for the disputed charge.

- Locate any authorization form or correspondence where the client approved the charge or the work.

- Gather service logs, emails, meeting notes, delivery receipts – anything that proves the service was delivered as promised. For example, if the reason for the dispute is “services not provided,” assemble evidence like ticket logs, reports sent, or confirmation emails from the client that acknowledge the work.

- If the dispute is regarding an “unauthorized charge,” then find proof of authorization, such as the signed agreement, the email where they sent you their card details for the payment, or login records from your portal showing that the client paid the bill themselves.

Collect these into a folder. This will form the backbone of your rebuttal. Having thorough documentation (as emphasized in Strategy #4) really pays off here – you’ll feel much more confident if you can quickly compile concrete evidence.

3. Submit a Professional Rebuttal

Your payment processor will have a procedure (usually through an online portal or via email or fax) for you to respond to (or “represent”) the chargeback. Time is of the essence here. You often have a deadline of 7-10 days to acknowledge and maybe ~30 days to submit evidence, depending on the card network.

Write a clear rebuttal letter or statement. Keep it professional and factual. State the transaction details (date, amount, last four digits of the card, etc.), and succinctly argue why the charge is valid. Refute the reason code with your evidence.

For example: “The client claims services were not provided; however, attached are the service logs and client emails confirming completion of work on the dates in question, demonstrating the services were delivered as contracted.”

Attach all relevant evidence in a neat, organized manner. Include copies of the signed contract, authorization, invoices, communications, and any other supporting documents compiled in step 2.

Submit the rebuttal through the designated channel and ensure you receive confirmation that it has been received.

4. Follow Up with the Client

After you’ve submitted your response, the issuing bank will review the evidence and make a decision (this can take several weeks).

Keep an eye on the case status via your processor’s portal. If the decision comes back in your favor, the chargeback is reversed, and you receive the funds (minus any applicable fees). If it comes back not in your favor and the chargeback stands, consider the following:

You may have the option for a second round or arbitration. In many cases, if you still strongly dispute the outcome, you can escalate to arbitration (where the card network mediates).

Be cautious: Arbitration involves additional fees (hundreds of dollars) and is generally only worthwhile for large disputes or matters of principle.

Decide if arbitration is worth it. For a small amount, it’s probably better to accept the loss and focus on preventing it from happening again. For a large amount, you may pursue it, but weigh the cost and potential damage to your relationship.

Reach out to the client one more time if appropriate. If you lost, perhaps the client truly felt justified (rightly or wrongly). It may be salvageable to have a conversation to understand their perspective and see if any resolution or lesson can be drawn. Or it may be the end of the road with that client.

5. Review Your Internal Processes

Whether you win or lose the case, use the experience to strengthen your billing workflows.

- Was there a communication gap?

- A billing surprise?

- Is there duplication?

Fixing those pain points helps prevent repeat disputes.

Importantly, every chargeback is an opportunity to refine your prevention strategies so that you won’t even get that notification email next time.

Conclusion: Reducing Chargeback Risk for Long-Term Payment Stability

Credit card chargebacks don’t have to be an inevitable cost of doing business for MSPs.

By understanding why they happen and ta