%2520(1).jpeg)

Debt is a common growth tool for MSPs. Whether you are acquiring another provider, investing in infrastructure, or supporting a HaaS model, financing often plays a role. What many MSPs underestimate is how much tax rules around interest deductions can affect real cash flow.

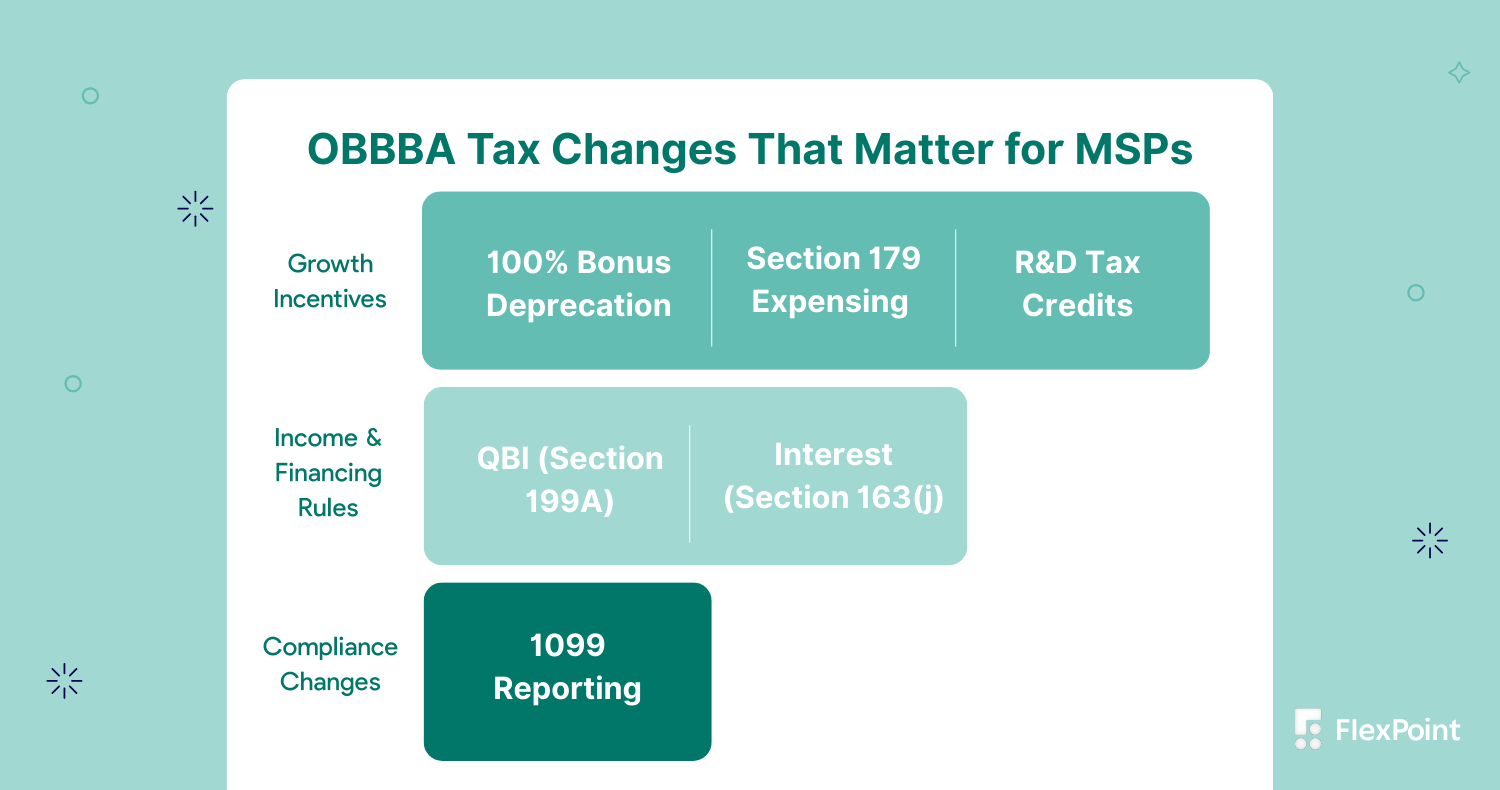

Section 163(j), also known as the business interest limitation, directly impacts how much of your interest expense you can deduct each year. With updates under the One Big Beautiful Bill Act, or OBBBA, these rules have changed again. Some of those changes are helpful. Others require closer attention.

If your MSP relies on debt to grow, this is one tax rule you cannot afford to ignore.

What is Section 163(j) and Why You Should Care

Section 163(j) limits how much business interest expense you can deduct in a given year. If your interest expense exceeds the limit, the extra amount is not lost. It is carried forward to future years.

That sounds manageable. In practice, it can create cash flow pressure, especially for MSPs that grow through financing.

Why MSPs Should Pay Attention to Section 163(j)

MSPs often take on debt for reasons like:

- Acquisitions and roll-ups

- Server, network, and infrastructure investments

- Hardware as a Service programs

- Smoothing cash flow during rapid growth

When interest deductions are limited, taxable income can increase even though cash is going out the door to service debt. That gap is where surprises happen.

How the OBBBA Changes Interest Deductibility in 2026

The OBBBA updated how adjusted taxable income is calculated for Section 163(j). For many MSPs, this means interest deductibility is more predictable than it was in recent years. But the math is still complex, and the impact varies based on how your business is structured.

TL;DR: How does Section 163(j) affect MSPs under the OBBBA?

Under the OBBBA, many MSPs can once again calculate adjusted taxable income using EBITDA instead of EBIT. This generally allows for larger interest deductions, especially for MSPs with depreciation-heavy investments or acquisition-related amortization.

What Is the Business Interest Limitation in 2026?

Under Section 163(j), your deductible business interest expense is limited to:

- the taxpayer's business interest income for the taxable year;

- 30% of the taxpayer's adjusted taxable income (ATI) for the taxable year; and

- the taxpayer's floor plan financing interest expense for the taxable year.

Any interest above this limit is carried forward.

How Interest Deductions Are Limited

The key factor is adjusted taxable income, often shortened to ATI. ATI is meant to reflect your ability to service debt, but it does not always line up with actual cash flow.

When ATI is lower, your allowed interest deduction shrinks.

Impact on Debt-Funded Growth

For MSPs using debt to grow, this can mean:

- Paying interest today

- Taking the tax deduction later

- Managing higher tax bills in the meantime

That timing difference matters, especially for growing teams.

Check out our timeline of key dates around the Big Beautiful Big.

Section 163(j) Before the OBBBA

EBIT vs EBITDA Limitation

Before recent changes, many MSPs were subject to an EBIT-based limitation. This excluded depreciation and amortization from ATI.

For MSPs investing heavily in technology or acquiring other businesses, this significantly reduced deductible interest.

Cash Flow Challenges for Leveraged MSPs

The result was frustrating but common. MSPs showed taxable income on paper while cash was being used to pay interest and fund growth. This was especially painful for PE-backed or acquisition-driven providers.

Section 163(j) Under the OBBBA

Restored EBITDA Treatment

The OBBBA restores EBITDA-based calculations for adjusted taxable income for many taxpayers. For MSPs, this often means a higher ATI and more interest deducted in the current year.

This change is especially helpful for businesses with:

- Significant depreciation from infrastructure

- Amortization from acquisitions

- Consistent interest expense tied to growth

Changes to Carry-forward Rules

Disallowed interest can still be carried forward indefinitely. What changes is how quickly those carry-forwards may be used now that EBITDA treatment is back in play.

Planning Implications for MSP Financing

The OBBBA improves how much interest many MSPs can deduct, but it also adds technical details that matter when planning financing.

Recent IRS guidance clarified the ordering rules under Section 163(j). For tax years beginning after 2025, the business interest limitation is generally calculated before most interest is capitalized into assets, with limited exceptions. This is particularly relevant for MSPs that capitalize interest tied to infrastructure, equipment, or long-term technology investments.

As the IRS explains:

“For taxable years beginning after Dec. 31, 2025, section 163(j) is applied before any mandatory or elective interest capitalization provisions, except for sections 263(g) and 263A(f). Accordingly, business interest expense excludes any interest capitalized under section 263(g) and 263A(f) and includes all other business interest expense.”

This ordering can change when and how interest expense becomes deductible and should be evaluated as part of upfront tax planning.

The OBBBA also clarifies how certain income items are treated when calculating adjusted taxable income, including:

- Subpart F income

- Net CFC tested income

- Section 78 gross-up amounts

- Deductions under Section 245A(a)

- Section 956 inclusions

- Net tested income under Section 951A

These details matter most for MSPs with complex ownership or international structures. For those businesses, interest deductibility should be modeled alongside entity structure and financing decisions, not handled as a year-end cleanup exercise.

EBIT vs EBITDA

Here is a simplified comparison to show why this change is important.

What Section 163(j) Changes Affect MSPs the Most

Acquisitions

Debt-financed acquisitions are where Section 163(j) shows up fast. Limited interest deductions can reduce post-acquisition cash flow and complicate integration plans.

Infrastructure-Heavy Scaling

MSPs investing in internal systems, servers, and platforms benefit more from EBITDA-based calculations, since depreciation no longer works against interest deductibility.

HaaS Financing Structures

Hardware-as-a-Service models often involve layered financing. Without planning, interest limitations can quietly eat into margins.

TL;DR: What are the interest deduction limits for MSPs in 2026?

In 2026, most MSPs will be limited to deducting business interest up to 30 percent of adjusted taxable income under Section 163(j), with ATI generally calculated using EBITDA under current OBBBA rules.

Strategies to Manage Interest Limitations

Entity Structuring

How your entities are structured and grouped can change how Section 163(j) applies. That’s because the limitation is calculated at the entity level, and disallowed interest can stay trapped at that level or flow through differently depending on how your business is organized and taxed.

For example, partnerships allocate excess business interest expense to partners, while S corporations carry it forward at the entity level only. Planning entity structure with 163(j) in mind can ensure you do not lose deductions unnecessarily or create unexpected cash flow timing issues.

Coordinating Depreciation and Interest

Depreciation elections and interest expense should be planned together because depreciation affects adjusted taxable income (ATI) under Section 163(j). When depreciation or amortization reduces ATI, it can shrink your interest deduction ceiling under the old calculation method, and even under the updated rules you still need to think about timing.

Considering depreciation strategy alongside interest planning helps ensure you are not shooting yourself in the foot with competing tax priorities or missing opportunities to optimize ATI.

Evaluating Financing Options

Interest rate is only part of the story. MSPs should evaluate financing based on cash flow impact, flexibility, and tax treatment because the amount of interest that can be deducted may be limited by Section 163(j) regardless of how much you pay.

Choosing between term debt, equity financing, lease structures, or capital leases can all have different implications for cash flow and taxable income.

Common 163(j) Mistakes MSPs Make

Ignoring Interest Carry-forwards

Untracked carryforwards lead to missed deductions and inaccurate forecasts, especially since disallowed business interest can be carried forward indefinitely until it can be used. If you do not track carryforwards carefully each year, you can overlook deductions you are entitled to in future years, which can inflate your tax bill.

Poor Coordination With Lenders

Loan terms can unintentionally worsen tax outcomes if tax considerations are not part of the conversation. For example, certain capitalized interest may become taxable income timing challenges, and lenders may not be aware of how the debt terms interact with 163(j) limitations.

Talking to lenders and tax advisors together ensures you are negotiating terms that work for both cash flow and tax strategy, not just one or the other.

Underestimating Long-Term Impact

Section 163(j) affects more than one tax year. It influences growth strategy, valuation, and exit readiness because the timing of interest deductions can change taxable income profiles over time. Missing the long-term impact can distort forward-looking models and lead to decisions that look good this year but weaken financial flexibility later.

Key Takeaways: Section 163(j and MSP Tax Planning in 2026

Section 163(j) has a real impact on MSP cash flow, especially for businesses that rely on debt to grow. Interest deductibility is not just a tax line item. It influences how much flexibility you have to invest, acquire, and scale.

The OBBBA brings more predictability by restoring EBITDA-based calculations for many MSPs. That said, the rules are still nuanced. Interest limitations need to be modeled before taking on new debt, not after tax season is over.

The MSPs that handle this best treat tax planning as part of their broader financial strategy. That means aligning financing decisions with long-term profitability and making sure finance and tax teams are working from the same playbook.

If you want help pressure-testing your approach for 2026, FlexPoint has you covered. Our 2026 Tax Readiness Checklist walks through the key areas MSPs should review before the year is underway.

Smart tax planning does not have to be complicated. It just needs to be intentional.