Paper checks have been the cornerstone of business payments for decades. They are tangible and familiar, and for a long time they seemed like the most reliable way to exchange funds. But the reality in 2025 is very different.

Today, paper checks are the most fraud-prone payment method in business. Malicious actors exploit outdated systems faster than banks and businesses can keep up, and the result is a nationwide surge in check fraud that’s leaving companies of all sizes exposed.

For most MSPs, the complications around paper checks go well beyond basic security risks. It’s not about sending checks or invoices, it’s about waiting for them. When clients still mail physical checks, payments are delayed, harder to track, and exposed to fraud before they ever reach your account.

But the real vulnerability starts with your client. If their check is stolen or altered in transit, they’re the one defrauded, while you’re the one waiting to get paid. When that risk is multiplied across dozens or even hundreds of recurring invoices, those delays can devastate your cash flow.

Why Paper Checks Are Especially Risky

Several features of paper checks make them inherently risky. Understanding these weak points clarifies why so many businesses (and their clients) are moving away from them.

- Sensitive data printed right on the check. Every check carries critical details: your client’s information, your business name, routing and account numbers, and even your signature. It’s everything a fraudster needs to create convincing counterfeits. It’s no surprise that 65% of organizations reported experiencing check fraud in 2024, with criminals using that visible data to forge new checks or drain accounts directly.

- Multiple hands and physical transit. A single check may pass through a dozen hands before it clears (mail carriers, receiving desks, processing centers) each one posing as a vulnerability. Since the pandemic, incidents of check fraud have surged over 385% nationwide, and the U.S. Postal Service continues to warn about organized theft rings targeting business mail for this exact reason.

- Lack of speed and traceability. Once a check leaves your office, tracking it is nearly impossible. Lost or stolen mail now accounts for the fastest-growing share of check fraud with nearly one-third of affected businesses reporting actual financial losses as a result. By the time you notice something’s wrong, the damage is already done.

What Check Fraud Is and How It Happens

Before diving into the risks, it helps to understand precisely how check fraud operates in practice. Sometimes it’s surprising how simple the exploits are and how vulnerable many businesses remain without even realizing it.

Mail Theft

One of the most common and low-tech fraud methods is mail theft. All it takes is someone grabbing envelopes from a mailbox, altering them, or moving them through illicit channels. Studies show stolen mail fraud rose around 10% in the last year, making it one of the fastest-growing types of check fraud. Once a check is intercepted, a malicious actor can steal account and routing information, forge signatures, or change payee names and amounts.

And According to the 2024 AFP® Payments Fraud and Control Survey, fraud linked to interference with the U.S. Postal Service rose by 10 percentage points in the past year, with one in five organizations reporting this type of incident. And it’s not always external actors: the FBI’s Internet Crime Complaint Center (IC3) warns that some theft happens inside the process itself, with insiders obtaining checks from mailrooms or legitimate business channels before they’re even sent. In fact, check fraud has surged nationwide, with mail carrier robberies increasing more than 250% since 2019 and businesses losing billions each year to stolen or altered checks.

As an MSP owner, this might look familiar: a client mails a check that never arrives, and suddenly their payment shows up as late. It’s a high-friction process with countless points of failure: mail delays, misplaced envelopes, or worse, stolen checks.

Even when the fraud happens on the client’s end, you’re the one who feels it in your cash flow while their bank investigates. And when your team follows up on the “late” payment, it can create uncomfortable conversations—especially if the client believes their check was already deposited… somewhere. By the time both sides realize what actually happened, the damage is done.

How Stolen Checks Are Altered

Once a check is stolen, criminals have several ways to turn it into cash. The most common are methods known as “washing” and “cooking.” In both cases, the check is physically manipulated to change key details like the payee name or amount. Washing uses chemicals to remove original ink so new information can be written in; cooking typically involves reprinting or layering new details onto an existing check to make it look authentic.

These techniques are shockingly easy to execute and difficult to detect, especially when checks are passed through multiple hands before deposit. For MSPs handling frequent client payments, one intercepted envelope can become a forged check worth thousands.

4 Ways Check Fraud Affects Your SMB

Even when you’re not the one committing the error, check fraud always leaves someone holding the bill. And it often comes back to you as the owner. Whether it’s a client’s payment that never arrives or a vendor check that gets intercepted, the ripple effects hit your business in multiple ways.

1. Financial Loss and Cash Flow Strain

When a check is stolen or altered, the financial impact can be immediate and significant. Your client may have funds pulled from their account, leaving you unpaid while they try to resolve it with their bank. While they do that, you are expected to continue your usual operations but one payment short. If it was a big project your client was paying you for, you may have been depending on that income for reinvestment into your business.

And the risk extends in both directions: if you pay vendors or technicians by check, they could become targets too. When fraud happens, someone inevitably eats the cost. In most cases, you either forgive the balance to preserve the client relationship or the client issues a replacement payment. Both outcomes stall your cash flow, inflate your receivables, and quietly eat away at the trust you’ve built with your customers.

2. Administrative Burden and Wasted Time

Fraud creates a paperwork avalanche. Your finance team has to identify the issue, dig through records, contact the bank, and report the incident all while trying to keep regular operations running.

Each investigation requires attention from finance, leadership, and sometimes even legal. That’s time your team isn’t spending on service delivery, let alone scaling. For a growing MSP, even a single incident can throw off reporting cycles and create cascading delays across payroll and client billing.

3. Client Relationship Damage

When a client believes they’ve paid you, but their check was stolen or cashed fraudulently, it’s an uncomfortable conversation. They are victimized; you’re still unpaid.

This dynamic can quickly break trust. Most MSPs know that client retention matters far more than any single invoice, so they often eat the loss just to avoid damaging the relationship. But over time, these situations add up. Repeated check-related issues can make clients question your systems, even when you’ve done everything right, slowly chipping away at the credibility and confidence you’ve worked so hard to earn.

In some cases, it’s also possible that not receiving a payment from one client becomes a regular thing if they realize you will cover the cost. When that happens, it is easy to become suspicious of anyone who cries "check fraud" as the culprit to their late payments... equally damaging your trust in them.

Even if it’s not your fault, it’s your relationship that takes the hit.

4. Internal Reputation and Team Friction

Lost funds also create internal tension. When money goes missing, someone gets blamed: accounting, operations, or whoever last handled the check. It’s rarely fair, but the uncertainty creates mistrust and stress across teams.

Loss of funds can easily make people turn on each other. That kind of vulnerability can reveal bigger control gaps, forcing uncomfortable internal reviews. Even if no one inside your business is responsible, the perception of poor controls can shake confidence among staff and leadership alike.

In short: a single compromised check can turn into a team-wide morale issue faster than you’d expect.

Why SMBs Still Send and Accept Paper Checks (and Why That’s a Problem)

So if the risks are so clear, why do so many businesses still use checks? If you are still using paper checks for sending and receiving payments, it may be helpful to consider where your biases may be holding you back.

Common Reasons

- Habit and familiarity: For many businesses, checks are how things have always been done. It’s what bookkeepers, accountants, and vendors expect. Changing behavior feels risky, disruptive, or burdensome.

- Perceived control: Some believe that signing and mailing a paper check gives more oversight. You physically review, sign, seal it. With that there is a tangible sense of control.

- Concerns about digital security: Surprisingly, some businesses hesitate to go digital because they believe electronic methods are more vulnerable. They worry about hacking, data breaches, or unfamiliar technology.

- Client preferences and legacy systems: Certain clients or partners insist on checks or haven’t adopted digital payment acceptance. Some businesses feel locked into using paper checks for fear of upsetting their clients.

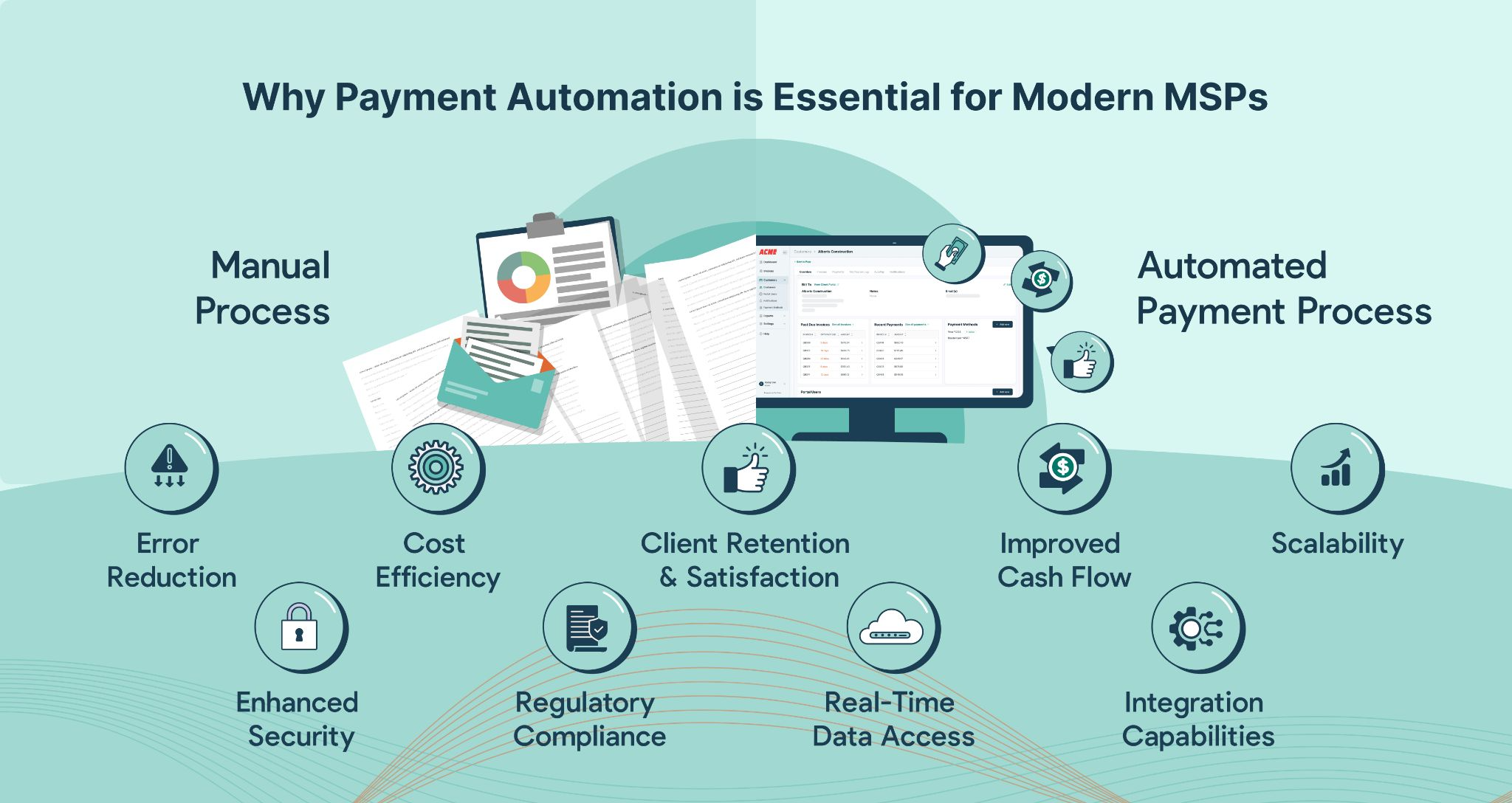

But ultimately, those reasons don’t hold up under consideration. The comfort of routine isn’t worth the cost of fraud, delays, and endless reconciliation headaches that come with paper checks. The control you think you have by mailing a physical payment disappears the moment it leaves your office. It’s quite literally out of your hands. Meanwhile, digital payment security has evolved far beyond what most businesses realize, with modern platforms using encryption, authentication, and audit trails that make ACH and electronic transfers far safer than handling paper. And the rest of the industry has already moved on; most vendors now accept ACH, eChecks, or credit cards, and those still insisting on checks increasingly look inefficient.

The good news? Making the switch isn’t complicated. Once you move payments online, you’ll wonder why you didn’t do it sooner.

It’s Time to Change: Why Transition to ACH

Modern alternatives like ACH are easier to adopt than most MSPs realize. ACH payments create a direct, encrypted connection between bank accounts, eliminating the risks of mail theft and check alteration, while remaining one of the simplest and most secure ways to transfer funds.

What ACH Offers

- Lower fraud exposure: Because ACH doesn’t require physical transport of sensitive information, many of the theft or alteration risks inherent in checks are eliminated.

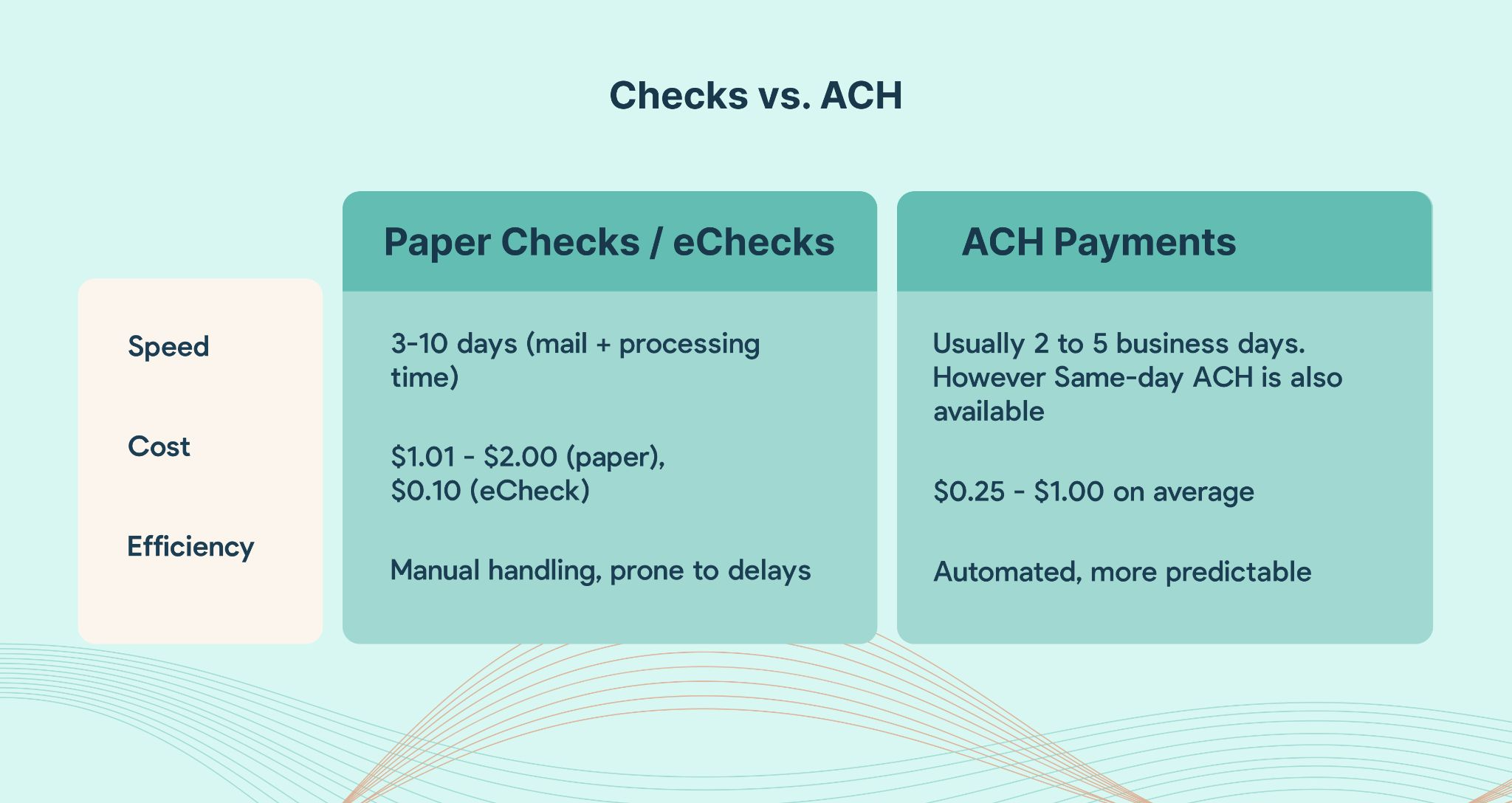

- Faster settlement: Standard ACH payments often clear in 3-5 business days; same-day ACH speeds this up further. Compared to checks that may take a week or more to clear (when mailing, processing, clearing are factored in), the difference is dramatic.

- Lower cost & less manual effort: No printing, ink, postage, manual mailing, or physical supervision. Automation allows you to send invoices in real-time, schedule recurring payments, all while saving labor costs.

- Better traceability & audit trails: Electronic records mean you can track who initiated payment, when, details of bank accounts, etc. That way it’s much easier to detect anomalies, reconcile statements, and investigate fraud.

How FlexPoint Helps MSPs Get Paid Securely and On Time

FlexPoint is built to give MSPs a safer, faster, and more reliable way to get paid without the risk, headaches, or cost that come with paper checks.

Same-Day ACH & Faster Fund Access

Paper checks slow everything down. Funds are tied up in the mail, and your team ends up waiting days (or weeks) to see cleared payments. FlexPoint eliminates that lag. With Same-Day ACH, your MSP can receive payments the same day clients post them. No chasing deposits, no wondering when money will hit.

For most businesses, standard ACH means waiting 3-5 business days for transfers to clear. FlexPoint’s Same-Day ACH closes that gap, giving you predictable cash flow and immediate visibility into your receivables.

Multiple Secure Payment Options

One of the biggest flaws with paper checks is that they leave you with no flexibility. Your clients either mail it or they don’t.

With FlexPoint, clients can pay you however works best for them: ACH, credit card, or even flexible financing for larger jobs. That flexibility means fewer delays, faster payments, and happier clients.

You get real control over your receivables without needing to chase checks or manually process deposits.

For clients who need extra runway, FlexLine financing allows them to pay larger invoices over time, helping you get paid upfront while still making those larger projects obtainable for them.

It’s a win on both sides: steady cash flow for you, flexibility for them, and none of the uncertainty that comes with paper.

AutoPay, Scheduled Payments & Predictability

With AutoPay, clients can set up recurring payments that run automatically each billing cycle. No envelopes, no signatures, no “the check is in the mail” messages that leave you questioning whether or not that is true. Payments happen on time, every time, and your team can finally stop chasing down invoices.

For more control, Scheduled Payments let you choose exactly when payments are processed. That way, your business gets paid on a reliable schedule that aligns with your budget and cash inflows, giving you better forecasting and peace of mind.

It’s the kind of predictability paper checks could never offer. And once you experience it, you’ll never want to go back.

Virtual Payment Terminal

Checks were never designed for speed, but MSP work often moves fast. Whether you’re billing for an urgent on-site project or a one-time hardware purchase, you likely need a way to collect payment in the moment.

FlexPoint’s Virtual Payment Terminal makes that possible. You can collect a payment on the spot, no waiting for invoices or physical checks. Generate a secure payment link, share it instantly, and accept ACH or card payments in seconds. Each transaction syncs automatically with your accounting system, so there’s no manual entry or reconciliation later.

It’s the easiest way to stay current with your clients and keep revenue flowing without ever touching a check.

Security & Compliance

One of the biggest misconceptions about going digital is that it introduces more risk. In reality, it’s the opposite. Paper checks expose your routing numbers, signatures, and banking info every time you send or receive one. FlexPoint keeps that data protected.

Built with PCI compliance and modern encryption standards, FlexPoint securely handles all payment information while meeting the highest data protection benchmarks in the industry. New features like Same-Day ACH also include intelligent risk scoring to identify and prevent fraudulent activity before it happens.

That means your business gets the speed and flexibility of modern payments without sacrificing security or compliance. When you move off checks with FlexPoint, you’re not trading one risk for another, you’re eliminating the problem.

ACH and Digital vs. Paper Checks: Side-by-Side Comparison of Payment Methods

The Bottom Line

Paper checks are both outdated and an increasing security risk that slows down your MSP. And every time a check goes through the mail, it exposes your clients.

But even if we ignore the security risks completely, paper checks overall disrupt cash flow and make it harder to plan ahead. Those unpredictable deposits force you to keep extra cash on hand or borrow short-term just to stay covered. Over time, that lag snowballs quickly.

Switching to ACH, credit card, or flexible financing through FlexPoint solves both of those problems at once. You get predictable deposits, faster settlement, and the confidence of knowing your payments are secure from start to finish. No envelopes or manual tracking.

With FlexPoint, the transition is seamless.

It’s time to leave paper checks in the past and protect your business with payments built for today.

What You Can Do Next

- Review your payment flow. How many checks do you still receive or send each month? How often do they arrive late, get lost, or raise fraud concerns?

- Talk with your clients. Most are ready for digital payment options. You just have to make them available and be willing to be transparent about any potential switch.

- Evaluate payment tools. Platforms like FlexPoint combine security, automation, and flexibility so you can move away from paper without adding extra work.

Are you ready to eliminate paper check risks and modernize your payments but are overwhelmed by the work it would take? That's why we built the Moving Clients Away from Paper Checks Toolkit with everything you, your internal teams, and clients would need for a seamless transition to secure payments.