For many MSPs, paper checks still make up a surprising share of receivables. They feel familiar, tangible, even “safe.” But the reality (one you’ve likely already felt firsthand) is that paper checks are outdated and painfully slow. But they’re also the most fraud-prone way to get paid today.

The 2024 AFP® Payments Fraud and Control Survey found that 63% of organizations experienced check fraud activity, making it the most targeted payment method for fraud. Add that to the average 60-day payment delay many MSPs already experience, and it’s easy to see why paper checks need to be left in the past.

It may seem daunting initially, but moving clients to secure digital payments doesn’t have to be a painful process. In fact, with the right structure and communication, you can migrate your entire client base away from checks in just 90 days and do it while minimizing client frustration.

This practical guide breaks down a three-phase plan to make that shift from paper checks quickly and effectively.

If you want to skip straight to the templates and checklist? Download the Toolkit for Moving Clients Away From Checks.

Why a focused 90-day window works

If you’ve ever tried to roll out a big change (whether it’s a new tool, process, or payment system) you know that open-ended timelines tend to drag on forever. That’s why 90 days is the sweet spot: it’s long enough to plan, communicate, and support your clients through the transition, but short enough to keep urgency (and accountability) alive.

Without a clear end date, even the best-intentioned rollout can lose momentum and start to feel optional, undermining the entire process.

For most MSPs, it also lines up perfectly with three billing cycles. That means you have the opportunity to announce the change, reinforce it mid-way, and then wrap up with final adoption all within a familiar cadence.

Days 1–30: Plan & Announce

Your first month sets the tone for everything that follows. This phase is about alignment: getting your team on the same page and shaping the narrative so clients hear “upgrade” instead of “hassle.”

At its core, Phase 1 comes down to three things: set expectations, educate clients, and give them a reason to care.

Start internally by appointing a single migration owner (like your office manager) someone who will coordinate communication, track adoption, and handle any hiccups that pop up. Then, bring your billing, ops, and account teams together for a quick 90-minute dry run. Walk through the new payment portal, client journey, review your call scripts, and confirm who’s responsible for follow-ups. That way, you’ll spot friction points long before your clients do.

Externally, your announcement should follow three simple rules: lead with benefits, be transparent about timing, and incentivize early action. Clients don’t need a technical explanation, they need to know this change actively benefits them.

- Lead with benefits. Emphasize the faster settlement, fewer disputes, convenience, and improved security. Put those three client benefits up front in every email, invoice footer, and portal banner so it’s undeniable. It may be helpful to lean into the security aspect if your clients are unaware that check fraud has increased 385% since the pandemic, putting their data (signatures, address, checking and routing numbers) at risk. If they’re aware that this change will protect them, they will be more likely to adopt quickly.

- Be transparent about timing and fees. Share the 90-day timeline and explain that mailed checks will incur a handling fee once the migration period ends. Clear deadlines reduce back-and-forth later.

- Offer an early-action incentive. Choose a modest but meaningful reward. For example: a one-time $50–$100 account credit for clients who set up ACH within 30 days, or waived card fees for the first billing cycle. Incentives are often the nudge that’s needed to compensate clients for the small upfront hassle of changing a habit. If you need some ideas, review these easy-to-implement valuable incentives.

Also distribute a short FAQ that tackles the real questions clients are likely to ask, such as:

- “Why are paper checks being phased out?”

- “What’s the benefit of paying digitally versus by mail?”

- “Will I still get a payment confirmation or receipt?”

- “Can I set up automatic payments so I don’t have to log in every month?”

- “What happens if I accidentally mail a check after the deadline?”

Keep the answers straightforward and reassuring with no jargon and link out to longer resources for clients who want more detail.

Days 31–60: Drive Adoption

Once the announcement dust settles, it’s time to turn awareness into action. Most clients won’t switch payment methods on their own, not because they’re resistant, but because they’re busy and comfortable with what’s familiar. This phase is about making the new process too easy (and too beneficial) to ignore.

At this stage, you move from informing to enabling. Your clients already know why the change is happening, now you’re showing them how to make it effortless.

Start by segmenting your client base: flag your top 20% by revenue and the handful still sending checks most frequently. Those accounts deserve the most direct and proactive outreach. A personal call, quick walkthrough, or even a screenshare can strengthen your relationship with these clients despite the fact that they may have the most reservation to changes in operation. The rest can be nudged with automated reminders and clear, one-click setup links.

These are the tactics that work including the way they should be approached:

- One-to-one outreach for priority accounts. Account managers or the migration champion should call high-value clients. Use a script focused on benefits and offer to walk them through setup in five minutes. Live walkthroughs close more quickly than emails.

- Automated reminders for everyone else. Send follow-up email nudges and use invoice footers that show ACH as the “preferred, no-fee method.” Small UX choices (labeling ACH first, pre-selecting it in the portal) to increase conversion.

- Make setup frictionless. Pre-fill forms where you can, provide a 60-second how-to video, and offer a scheduled setup call. The less cognitive load equals higher adoption.

- Publicize early adopters. With permission, highlight clients who switched in a newsletter, quick testimonial, or internal shoutout. When other clients see their peers adopting successfully, it builds confidence and creates gentle social pressure to follow suit.

Days 61–90: Enforce and optimize

By the final month you either have momentum or you don’t. This phase converts momentum into policy and systems.

First, issue a final notice: remind clients that the handling fee takes effect on Day 91 and clarify any exceptions (for example, legacy contracts that you’ll grandfather or manual payment channels you still accept temporarily). Then, begin applying fees consistently. Consistency is crucial. Enforcement without follow-through ultimately undermines your credibility.

Concurrently, tighten reporting and measure impact. Key KPIs to report internally:

- ACH adoption rate (percentage of invoices paid digitally)

- DSO changes (average days to receive payment)

- Number of manual deposits/checks processed per billing cycle

- FTE hours reclaimed from reconciliation tasks

These metrics translate into real operational wins: less staff time tied up in deposits and reconciliation, fewer late or missing payments, lower fraud exposure, and smoother month-end close. Share the before-and-after with leadership so everyone sees the impact, not just the effort.

Finally, codify the new normal. Update your client onboarding, contract language, and internal SOPs so future clients are enrolled on day one and checks are the exception, not the rule. Paper checks shift from “default” to a documented exception, which prevents backsliding and protects the work you just established.

Handling the predictable objections (and the scripts that close them)

Some objections always recur. Below are short, effective responses that your account team can use:

- “We’ve always paid by check.” Reply: “We completely understand! Checks are familiar. But the switch takes five minutes and will save you time every month after that. We can set it up together now and you’ll be done in under five minutes.”

- “I don’t trust online payments.” Reply: “Our portal uses bank-level encryption and tokenization. If you want, we can walk through the security together or show you the audit receipt immediately after a test payment.”

- “It’s too complicated.” Reply: “We’ll handle the setup for you. Most clients are set up in under five minutes and get instant confirmation afterward.”

If you need, we have full templates and scripts available in our Moving Clients Away From Checks toolkit for consistent messaging. Ensure your tone is calm and helpful, not defensive or aggressive.

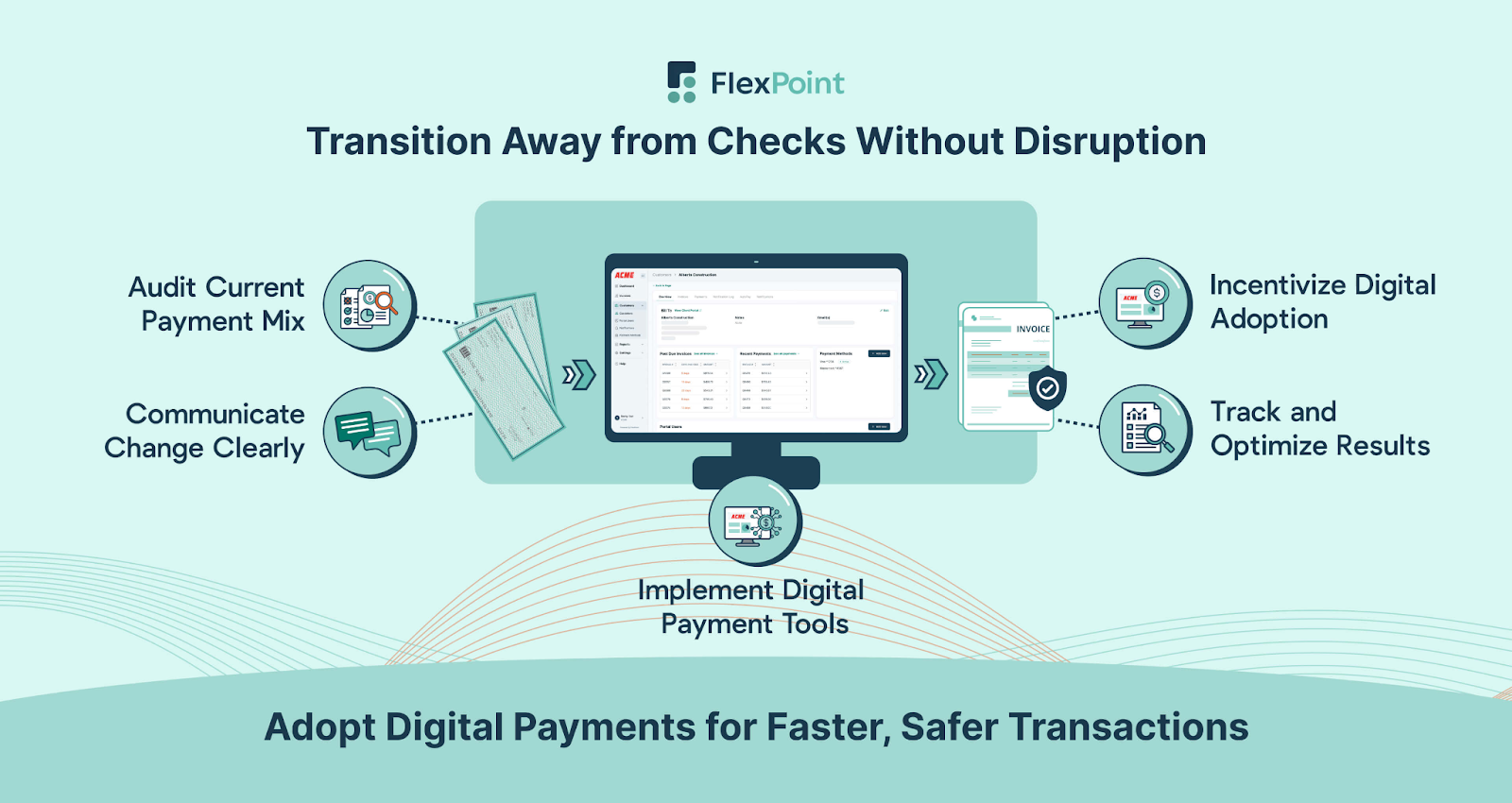

The Right Platform Makes Adoption Easier for Everyone

Before you send out that first client email, make sure the experience you’re promoting actually works. The platform you choose will make or break your migration. It needs to be secure, easy for clients to use, and flexible enough to fit your internal workflows. I

For MSPs, the right payment platform is your foundation for growth and good client relations. But if they encounter friction, confusion, or security concerns during setup, adoption will stall before it even begins.

Before you introduce anything to clients, make sure your payment platform checks these boxes:

1. Bank-grade security and compliance

Your system must meet or exceed PCI DSS standards for card payments and follow NACHA rules for ACH transfers. Make sure the platform you’re using to capture digital payments meets standard compliance certifications and reassure them their payment data is encrypted, verified, and protected.

Clients already trust you with their money and their systems. The payment process should reinforce that trust, not introduce doubt. A platform that clearly demonstrates security makes it easier to answer the inevitable question: “Is this safe?”

If the security story isn’t straightforward and documented, keep looking.

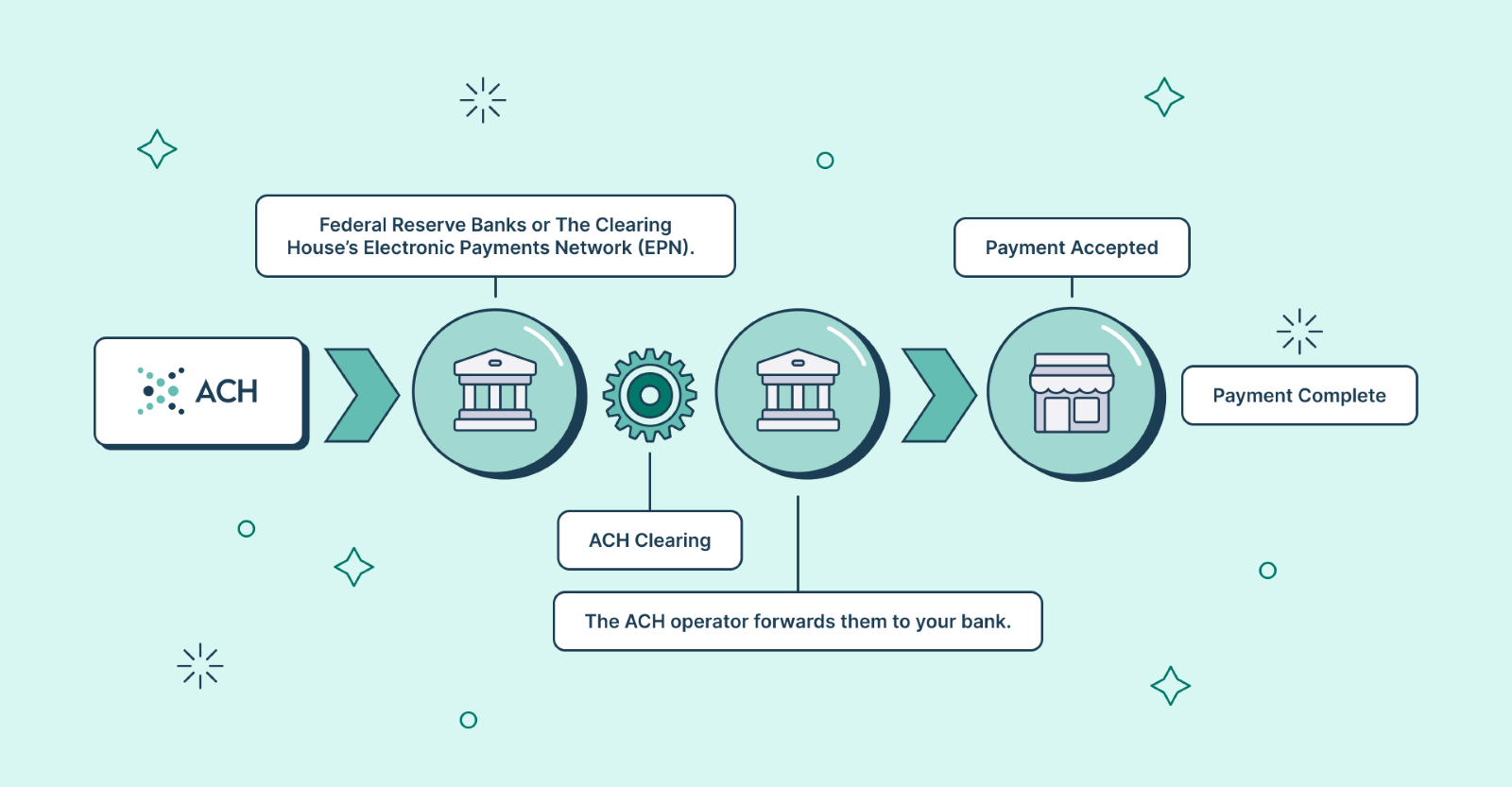

2. ACH with Same-Day capability

ACH is already the most cost-effective and fraud-resistant way to manage recurring revenue — no fluctuating card fees, no physical exposure, and no multi-day float from mailed checks.

Same-Day ACH strengthens this even further by reducing waiting time for funds to clear, which makes your cash flow more predictable month to month. And predictable cash flow is how you plan staffing, renewals, hardware purchasing, and service delivery without guesswork.

So when evaluating platforms, make sure ACH is simple to set up and Same-Day ACH is supported. Otherwise, you’re leaving one of the biggest advantages of digital payments on the table.

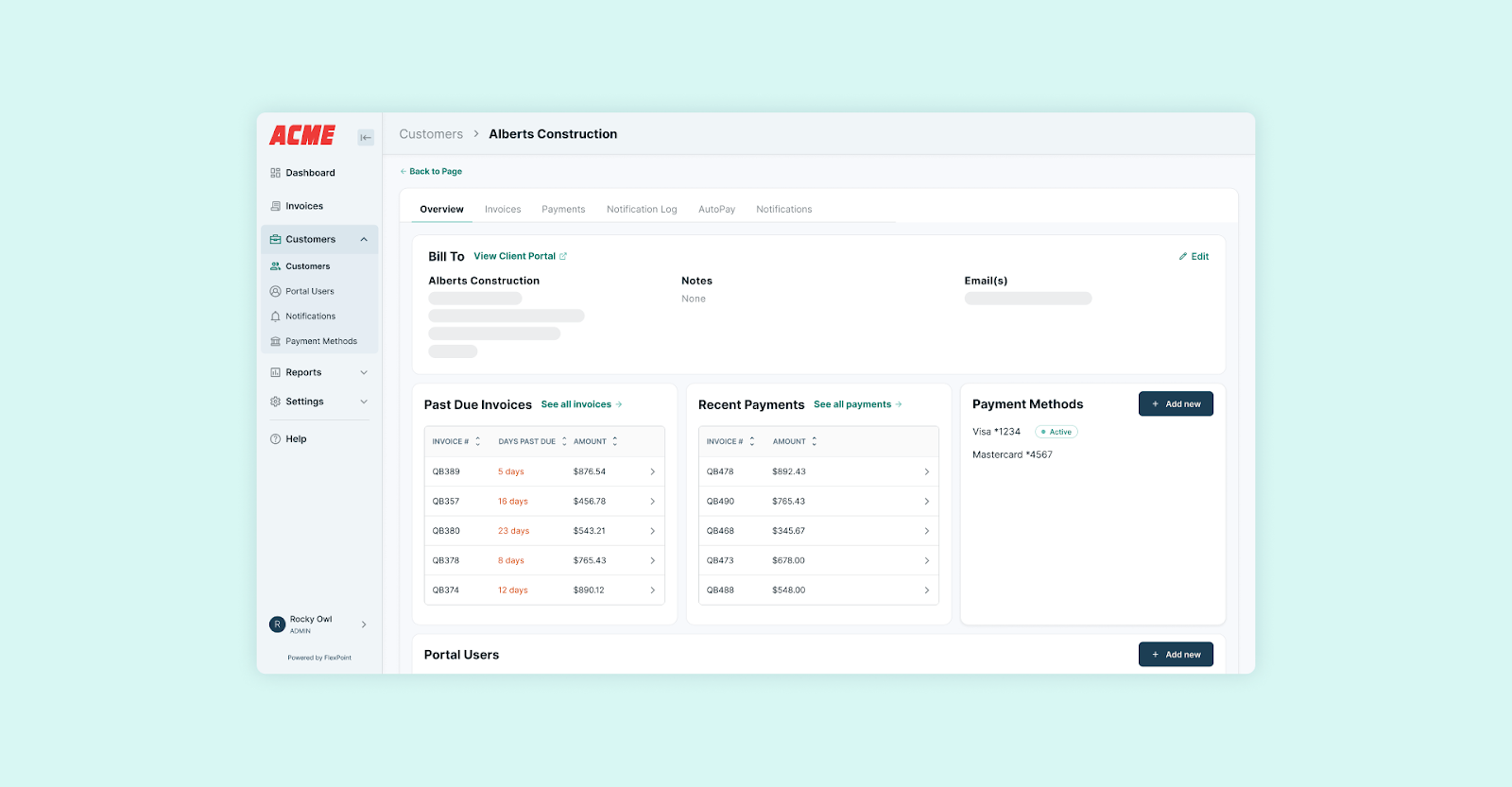

3. Branded client experience

Your payment portal should look and feel like your MSP, not a generic third-party site. A branded portal and verified sender domain make invoices and payment links instantly recognizable, which reduces phishing confusion and builds trust. When clients feel confident they’re in the right place, adoption is faster and support tickets drop.

4. Automated reporting and deposit reconciliation

Your payment platform should reduce admin effort, not shift it around. Look for automated reconciliation that syncs directly with your PSA and accounting tools and gives you clear visibility into adoption and days-to-payment trends.

Your finance team should be able to see (at a glance) who has switched to digital payments, who hasn’t, and which invoices need attention. If you still need spreadsheets to track any of this, the platform isn’t doing enough.

5. Native integrations with your PSA and accounting systems

Your payment system should sync directly with your PSA and accounting tools so your team isn’t stuck doing duplicate data entry or manual matching. When transactions flow automatically into ConnectWise, Autotask, HaloPSA, SuperOps, QuickBooks, or Xero, your invoices reconcile cleanly, reporting stays accurate, and you maintain real-time visibility into receivables. No swivel-chair work, no extra spreadsheets, just clean, connected billing.

Before committing, test the full client journey yourself: send an invoice, set up ACH, save payment details, and check the confirmation flow. If it feels confusing to you, it will absolutely frustrate your clients.

At this point, you have the framework, the timeline, and the tools to lead a smooth transition. But even the best rollout plans come with questions from your team and from clients. That’s normal. But the key is being prepared with clear and confident answers.

Here are some of the most common questions MSPs face when moving clients off checks.

FAQ: What MSPs Need to Know Before Moving Away from Paper Checks

1. What if some clients refuse to switch?

Start with your high-value or easiest-to-convert clients first. That momentum builds social proof. For the rest, use a combination of clear communication, time-bound incentives, and gentle enforcement (like a small check handling fee). Over time, even resistant clients typically switch once they see others benefit.

2. Will digital payments actually save me money?

Yes, significantly. Between postage, manual processing, and reconciliation time, paper checks can cost $4–$6 per payment on average. Digital payments (especially ACH) not only eliminate those costs but also accelerate cash flow and reduce fraud risk.

3. How do I make clients feel safe using a new system?

Transparency is key. Use verified, branded payment portals (like FlexPoint) so clients know exactly where their money is going. Communicate the platform’s security standards and provide a clear FAQ or onboarding guide for reassurance.

4. Should I charge fees for paper checks right away?

Not immediately. Announce the upcoming change, explain the reasoning (security, speed, efficiency), and pair it with an incentive for early adopters. After 60–90 days, you can confidently introduce a small handling fee for mailed checks, clients should understand and respect the transition.

5. How do I measure success?

As mentioned above during days 60-90, it's helpful to track three key metrics:

- ACH adoption rate (%) — how many clients have switched

- Days Sales Outstanding (DSO) — how quickly you’re getting paid

- Manual payment volume — how much time your team spends handling checks

The Key to Long-Term Success

Moving away from paper checks isn’t just a one-time project, it’s a lasting upgrade to how your MSP operates. The goal isn’t only to get clients migrated; it’s to make digital payments the default going forward. That means every new client starts with your payment platform, every renewal reinforces the process, and every billing cycle runs without worry or waiting on the mail.

Keep reinforcing the benefits. Celebrate clients who adopt early, reward consistency where it matters, and continue reminding your team how digital payments protect both cash flow and trust. Small touches go a long way here: a quick “we appreciate you” credit for clients who stay on autopay, quarterly check-ins on payment experience, or simply acknowledging how seamless things have become compared to check handling.

The good news is that you don’t have to start from scratch. The Moving Clients Away From Checks Toolkit includes everything you need to build and sustain a 90-day migration plan, complete with checklists, scripts, templates, and tracking tools to make your rollout smooth and effective.