Surcharging is permitted in Vermont (as of[$c-month-year] February 2025[$c-month-year]), allowing managed service providers (MSPs) to pass credit card processing fees to clients who choose to pay with a credit card.

Instead of absorbing these costs into service pricing, surcharges provide an alternative that keeps base service rates competitive while ensuring fair cost distribution.

Vermont MSPs must still follow federal regulations, state consumer protection policies, and card network rules to avoid penalties and maintain transparency.

Visa, Mastercard, Discover, and American Express each have their own surcharge policies, which MSPs must adhere to when implementing fees.

A compliant surcharging strategy includes proper client disclosure, adherence to fee limits, and transparent invoicing. This guide explains Vermont’s surcharge regulations, how MSPs can legally apply surcharges, and how automation tools can help streamline the process.

Disclaimer: This content is for informational purposes only and should not be considered legal advice. Vermont MSPs should consult a qualified attorney to ensure compliance with all applicable laws before implementing surcharging practices.

{{toc}}

What is Credit Card Surcharging for MSPs in Vermont?

Credit card surcharging permits MSPs in Vermont to recover the costs associated with processing card payments, which typically range from 2% to 4% per transaction.

With surcharging, MSPs can pass these costs directly to clients who choose to use credit cards rather than increasing service fees for all clients.

This is particularly beneficial for MSPs with subscription-based billing models or those handling large monthly transaction volumes, where card processing fees significantly impact the bottom line.

Consider an MSP in Vermont, processing $200,000 in monthly credit card payments at an average 3.25% processing rate. It would incur monthly fees of $6,500, totaling $78,000 annually in processing costs.

By implementing a 3% surcharge, the MSP recovers $6,000 per month, offsetting $72,000 per year in credit card expenses. The remaining $6,000 annual difference is either absorbed or adjusted through a slight service fee increase.

Alternatively, if the MSP applies a 1.5% surcharge, clients would cover $3,000 per month, reducing the MSP’s annual out-of-pocket costs by $36,000.

Clear communication and invoicing practices help maintain trust and ensure compliance with Vermont's consumer protection laws and federal regulations. Clients should be notified about surcharges in advance, and each invoice should clearly display the fee.

Example invoice breakdown:

- Managed IT Services: $22,000

- Credit Card Surcharge (2.5%): $550

- Total Due: $22,550

Vermont MSPs must also comply with Visa, Mastercard, Discover, and American Express policies, which set surcharge limits and require MSPs to provide proper disclosure.

Surcharges cannot exceed the actual cost of processing payments and must be capped at the network-imposed percentage limit (e.g., 3% for Visa).

When properly executed, surcharging provides a cost-effective way for Vermont MSPs to manage expenses, maintain competitive pricing, and ensure fair payment options for clients.

{{cal-one}}

Understanding Credit Card Surcharging Laws in Vermont

As of [$c-month-year]February 2025[$c-month-year], Vermont does not impose additional state-specific restrictions on credit card surcharging beyond federal regulations.

This means managed service providers (MSPs) operating in Vermont can pass processing costs to clients who pay with credit cards, provided they comply with federal laws and card network requirements.

Federal law permits a maximum surcharge of 3% to 4%, depending on the card network, but the surcharge must not exceed the actual cost of processing the transaction.

Vermont MSPs can implement surcharges up to these limits, following the policies set by various card networks.

While Vermont law does not directly regulate surcharges, the state has historically taken steps to address credit card processing fees.

In 2010, Vermont became one of the first states to pass legislation limiting debit transaction swipe fees, a move designed to protect small businesses from rising processing costs.

More recently, in 2025, Vermont lawmakers proposed reforms addressing swipe fees and transparency for retailers. While these efforts do not change surcharge rules, they may influence future discussions around credit card processing costs.

Although these reforms do not ban surcharging, they may lead to further discussions about the role of credit card fees in Vermont’s business landscape.

MSPs in Vermont cannot apply surcharges to debit or prepaid cards, even when processed as credit transactions. This rule aligns with the Durbin Amendment of the Dodd-Frank Act and applies universally.

{{debit-cta}}

Any surcharge must also be disclosed to clients in advance, with clear, visible notices at the point of sale and within online transactions. Transparent billing practices help maintain trust and ensure compliance.

Receipts and invoices must explicitly list the surcharge amount to prevent confusion or disputes. Failure to do so can lead to chargebacks and potential non-compliance with payment network policies.

Additionally, merchants cannot profit from surcharges—the fee must accurately reflect the actual credit card processing cost and must be communicated clearly to clients.

Vermont MSPs looking to implement surcharging should ensure complete transparency in their billing structure.

An example breakdown might look like this:

- Service Fee: $8,000

- Credit Card Surcharge (2.8%): $224

- Total Due: $8,224

Surcharging is an effective tool for Vermont MSPs to offset processing fees, but it must be applied carefully to remain within legal and card network requirements.

With ongoing state efforts to reform swipe fee policies, MSPs must stay informed about potential regulatory changes that could impact surcharging in the future.

For further guidance, consulting a legal professional ensures compliance with state, federal, and card network policies. Proper implementation helps Vermont MSPs maintain transparent, fair, and legally sound payment structures.

{{usa-cta}}

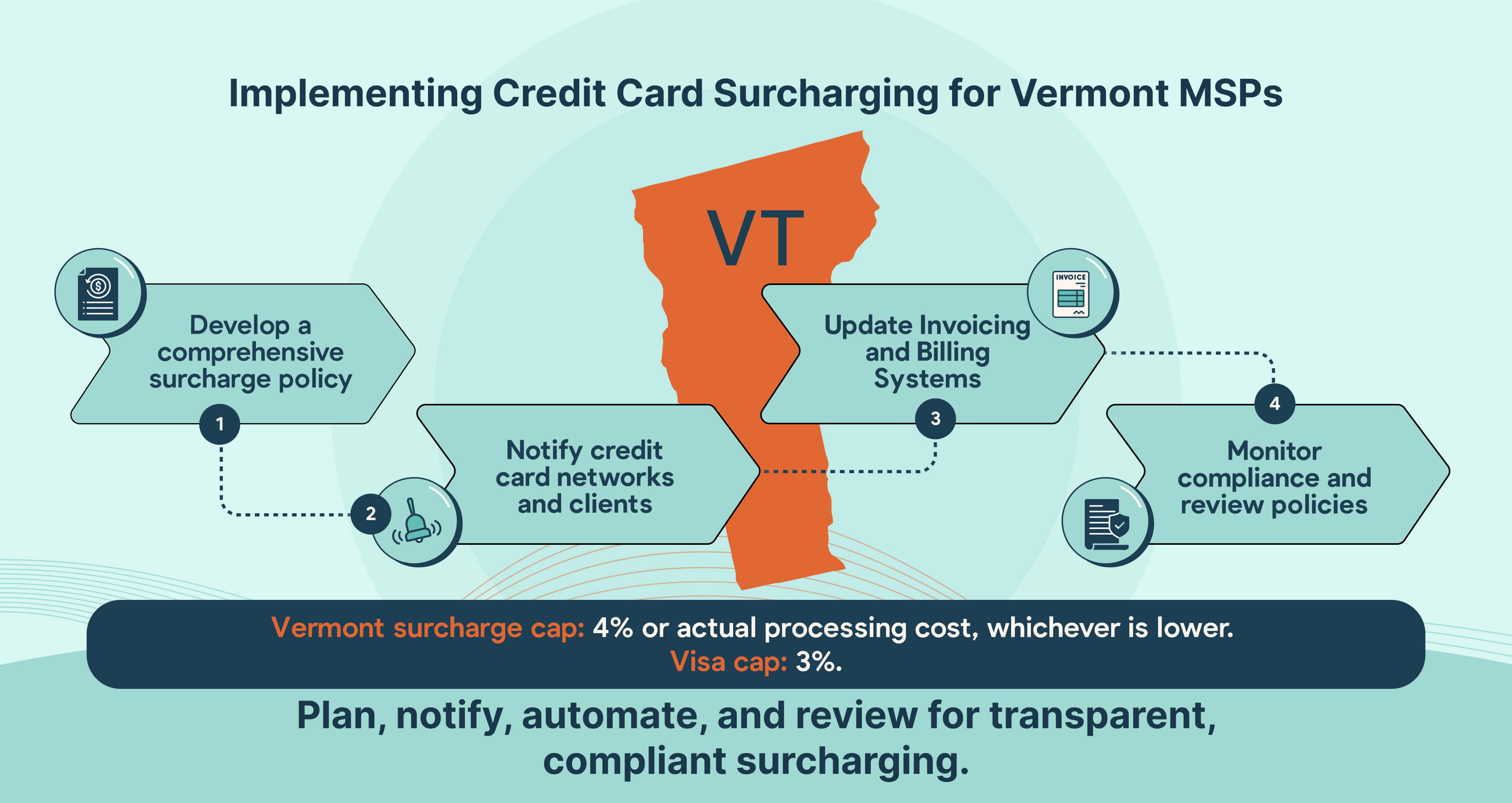

Implementing Credit Card Surcharging for Vermont MSPs

Establishing a surcharging policy in Vermont requires careful planning and clear communication to ensure a smooth transition. Failing to notify clients properly or structuring fees incorrectly can lead to payment disputes, chargebacks, or loss of client trust.

For instance, an MSP applying a surcharge without proper disclosure might face rejected payments or unexpected disputes.

To avoid these issues, here are four essential steps Vermont MSPs can follow to implement surcharging while maintaining compliance.

Step 1: Develop a Clear Surcharge Policy and Structure

A surcharge policy should clearly define how and when fees will be applied, reducing confusion and disputes. This includes specifying the percentage, how the fee is calculated, and how it will appear on invoices.

Vermont MSPs can choose from several surcharge structures based on transaction volumes and business needs.

a. Fixed Percentage Surcharge

A consistent percentage is applied across all transactions, ensuring compliance with Visa’s 3% limit or the actual processing cost, whichever is lower.

Example: An MSP applies a 2.9% surcharge.

- Service Fee: $12,500

- Surcharge (2.9%): $362

- Total Due: $12,862

This method is simple and works well for MSPs with predictable processing costs.

b. Flat Fee Surcharge

A fixed fee is added to all credit card transactions. However, it must remain within actual processing costs to comply with federal and card network guidelines.

Example:

- A Vermont MSP charges a $45 flat fee per credit card transaction.

- For a $4,000 invoice: Total Due: $4,045

- For a $600 invoice: The flat fee exceeds 3% ($18 max), requiring an adjustment to $618 total.

While easy to apply, this method may not be suitable for MSPs with widely varying transaction sizes.

c. Tiered Surcharge

Different surcharge rates are applied depending on the transaction amount. This approach benefits MSPs with variable invoice sizes.

Example:

- 2.2% surcharge for invoices below $5,500

- 3% surcharge for invoices $5,500 and above

For a $4,700 payment:

- Surcharge (2.2%): $103

- Total Due: $4,803

For a $6,800 payment:

- Surcharge (3%): $204

- Total Due: $7,004

Regardless of the structure, Vermont MSPs must keep surcharges within processing cost limits and ensure compliance with Visa, Mastercard, and federal policies.

Step 2: Notify Credit Card Networks and Clients

Before applying surcharges, Vermont MSPs must notify card networks such as Visa, Mastercard, American Express, and Discover. Visa, for example, requires 30-day advance notice, which can be submitted through an online form.

Client communication is equally important. Before implementation, MSPs should disclose surcharges in contracts, invoices, and service agreements.

A Vermont MSP might use language like this in client notifications:

"Effective [date], a 2.7% surcharge will be applied to all credit card payments to cover processing fees. This charge is not a profit-generating fee but a way to maintain service pricing while offering multiple payment options. You will see this surcharge clearly listed on your invoices."

Consider a Vermont MSP issuing a $7,200 invoice with a 2.9% surcharge.

If the client expects a $7,200 total but sees a $7,408 charge, they may dispute the payment. A chargeback could lead to refunds, administrative costs, and penalties, reducing the MSP’s revenue.

The average chargeback cost is estimated by Swipesum at $190 per dispute, including lost revenue and fees. Transparent surcharge communication helps reduce disputes, maintain cash flow, and strengthen client relationships.

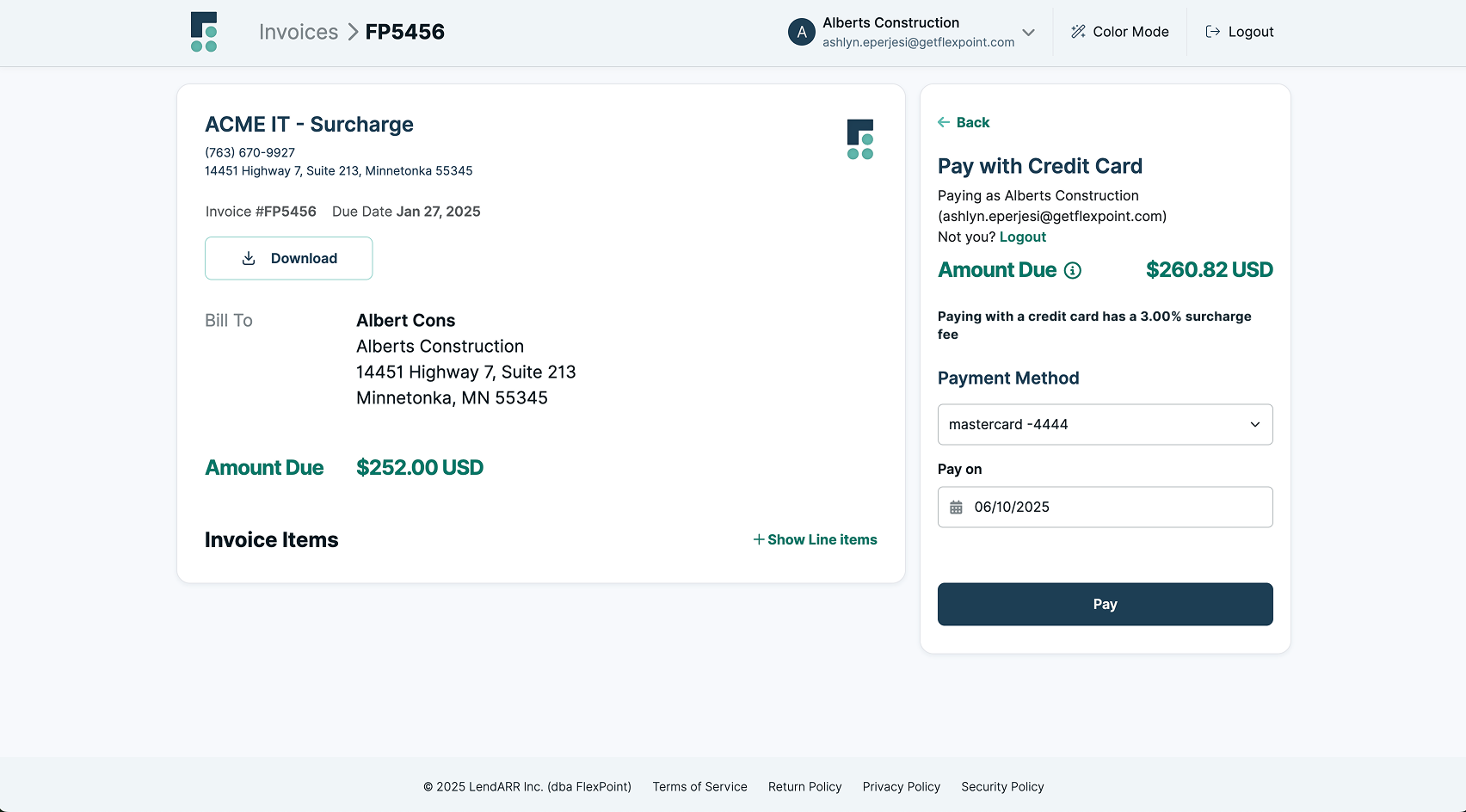

Step 3: Update Invoicing and Billing Systems

Invoices must clearly show surcharges as separate line items to ensure clients understand their charges. This helps prevent disputes and ensures compliance with Vermont’s consumer protection laws and card network rules.

Using automated billing systems like FlexPoint can simplify surcharge management for Vermont MSPs. These systems calculate fees automatically, ensuring accuracy and transparency.

For example, an MSP issuing a $10,500 invoice with a 2.8% surcharge would see the following breakdown:

- Service Fee: $10,500

- Surcharge (2.8%): $294

- Total Due: $10,794

Step 4: Monitor and Review Compliance

Vermont MSPs should regularly review surcharge practices to ensure compliance with card network rules and evolving regulations.

For instance, if an MSP’s actual processing cost is 2.6%, they cannot apply a 3% surcharge—even if Visa allows it. If an MSP overcharges, they risk fines, forced refunds, or loss of surcharging privileges.

Example:

- An MSP with a 2.5% processing cost applies a 3% surcharge.

- This violates Visa policies and could result in penalties or legal action.

Conducting quarterly compliance reviews ensures that surcharge rates align with actual costs and avoids potential violations. Keeping records of client communications and card network approvals is also essential in case of disputes.

Proper documentation allows Vermont MSPs to respond efficiently to complaints and maintain regulatory compliance.

By following these best practices, Vermont MSPs can implement surcharging legally, transparently, and effectively, helping them control costs while maintaining client trust.

{{ebook-cta}}

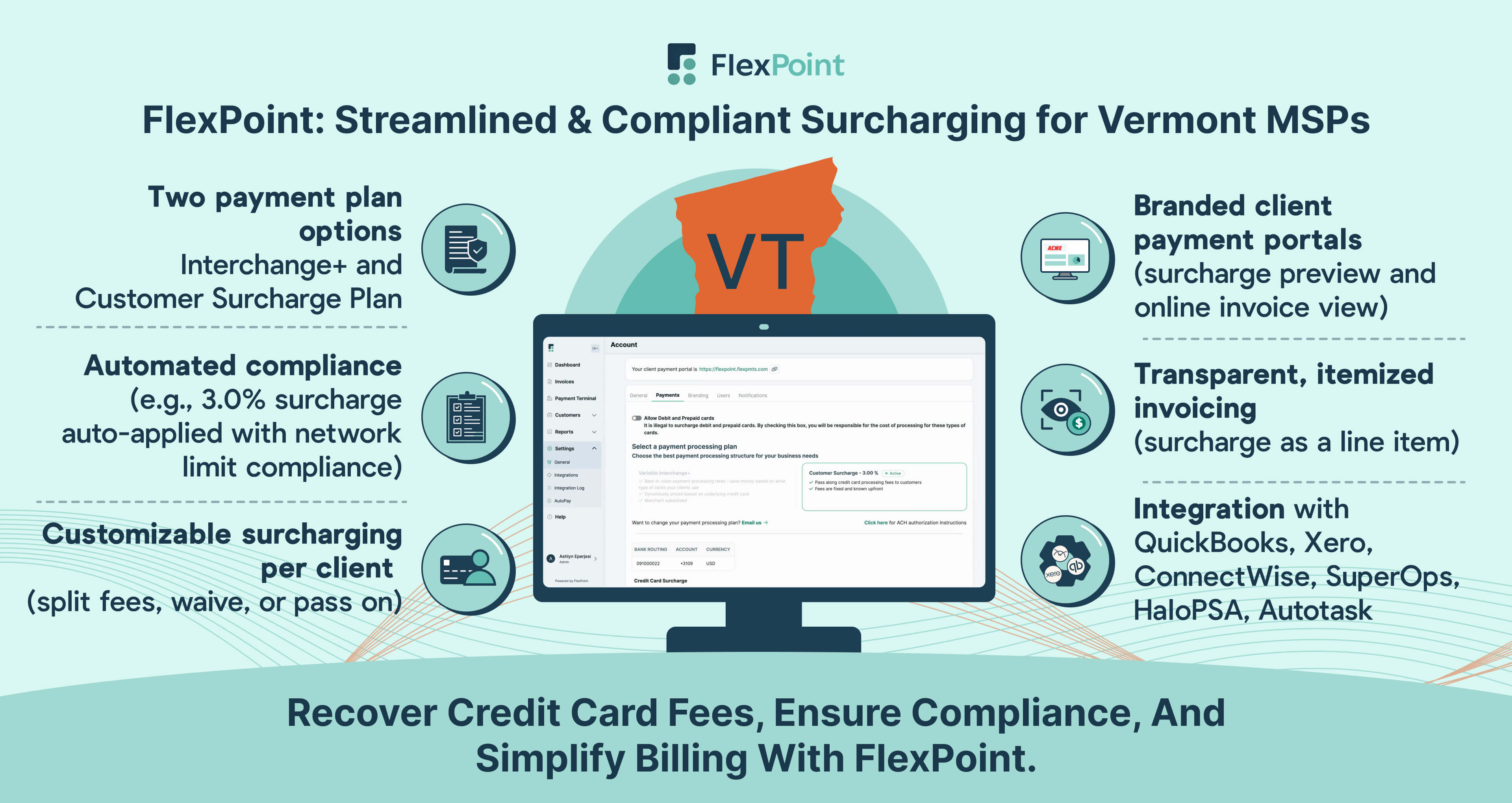

The Role of FlexPoint in Streamlining Credit Card Surcharging for Vermont MSPs

FlexPoint provides Vermont MSPs with versatile payment processing solutions that help them manage credit card fees efficiently.

With customizable surcharge settings, MSPs can absorb, share, or pass on transaction fees to clients, ensuring their pricing strategies align with their business goals while maintaining client trust and transparency.

Using FlexPoint, Vermont MSPs can control payment processing costs, automate billing, and comply with state and federal surcharge regulations, making payment collection more streamlined and predictable.

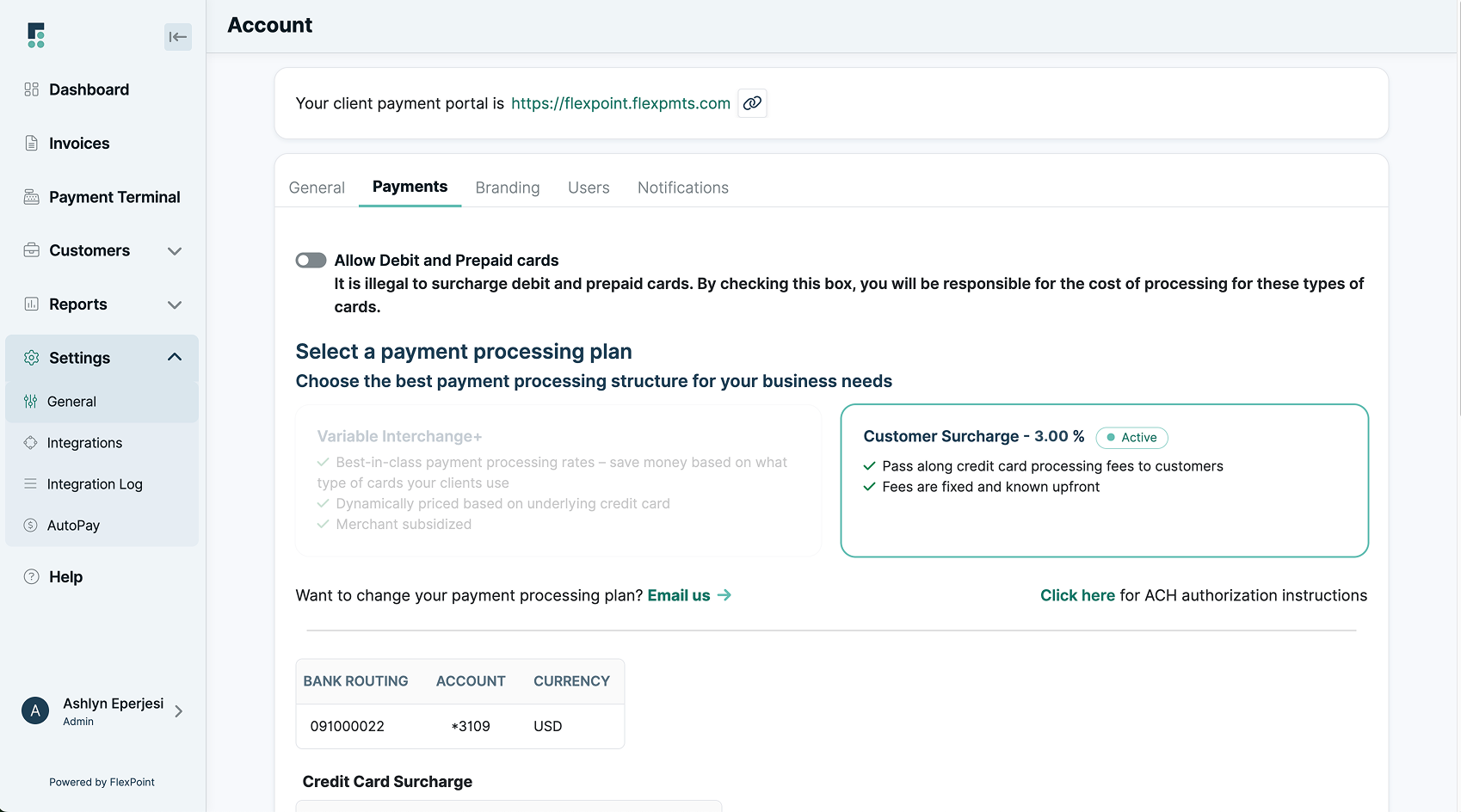

Payment Processing Plans

To help MSPs in Vermont handle transaction fees effectively, FlexPoint offers two structured payment plans:

- Interchange+ Plan

- Customer Surcharge Plan

a. Interchange+ Plan

For MSPs that prefer consistent pricing without passing processing fees to clients, the Interchange+ Plan ensures predictable costs while maintaining a seamless client experience.

Different credit cards come with varying interchange rates.

For example, processing a Visa consumer card typically costs less than handling a Mastercard corporate credit card, which carries higher interchange fees. This plan allows MSPs to gain insight into real transaction costs, allowing for better budgeting and financial forecasting.

Vermont MSPs leveraging FlexPoint’s Interchange+ Plan only pay the direct processing costs, avoiding unnecessary markup fees. This allows them to optimize their pricing strategy without increasing client charges.

b. Customer Surcharge Plan

For MSPs that want to recover processing costs from clients, the Customer Surcharge Plan allows them to apply a surcharge on credit card payments while ensuring compliance with Vermont's regulatory landscape and federal guidelines.

This model adds a small percentage to client transactions to recover processing fees.

For instance, if a Vermont MSP issues a $14,000 invoice and applies a 2.8% surcharge, the total due would be $14,392.

This plan allows MSPs to protect their profit margins while still offering clients multiple payment options.

Some Vermont MSPs prefer a hybrid approach, where they share part of the processing cost while passing a portion to the client.

FlexPoint provides flexibility to customize surcharge structures based on business needs.

For example, on a $7,500 transaction, an MSP may choose to absorb 1.2% of the fee while charging the client the remaining 2.3%, balancing cost recovery and client satisfaction.

FlexPoint’s automation tools ensure these calculations are accurate, eliminating the risk of overcharging while keeping MSPs compliant with Visa’s 3%cap and federal rules.

How FlexPoint Enhances Surcharging Compliance and Transparency

FlexPoint simplifies credit card surcharging by automating calculations, preventing errors, and ensuring Vermont MSPs stay within legal limits.

Below is an example of a Vermont-based MSP issuing a $10,800 invoice with a 2.9% surcharge.

Vermont MSP Client INVOICE

Company Name: Your MSP

Invoice #: 567892

Invoice Date: May 1, 2025

Due Date: June 1, 2025

Bill To:

[Client Company Name]

[Client Address]

[Client Contact Name]

[Client Email]

Services Provided

Subtotal: $10,800.00

Surcharge (2.9% of Subtotal): $313.20

Total Amount Due: $11,113.20

Payment Terms

Payment is due within 30 days of the invoice date. The surcharge complies with Vermont’s surcharge policies, federal laws, and card network requirements.

Notes:

If you have any questions about this invoice or need further clarification, please contact us at [Your Contact Information].

FlexPoint’s Integration with MSP Tools for Seamless Billing

Vermont MSPs can integrate FlexPoint with their preferred financial and operational platforms, allowing for automated payment workflows, real-time reconciliation, and accurate surcharge tracking.

Supported integrations include QuickBooks Desktop, QuickBooks Online, Xero, ConnectWise, Autotask, HaloPSA, and SuperOps.

These platforms help Vermont MSPs simplify surcharging and maintain efficient operations without disrupting their existing financial systems.

For example, by integrating FlexPoint with QuickBooks Online, MSPs can access real-time financial updates, ensuring they accurately track surcharges, processing fees, and payment statuses.

FlexPoint also offers branded client payment portals, ensuring clients can view invoices, surcharge breakdowns, and payment options in one place.

Automated reporting features provide detailed transaction insights, helping Vermont MSPs manage cash flow, compliance, and revenue tracking more effectively.

By reducing manual financial tasks, FlexPoint allows MSPs to focus on business growth while staying compliant with Vermont’s evolving payment regulations.

{{client-portal-gif}}

Offering Flexibility in Surcharging

{{admin-portal-gif}}

Vermont MSPs must balance surcharge flexibility with compliance requirements. FlexPoint simplifies the process, allowing businesses to adjust surcharging strategies while ensuring adherence to Vermont’s regulations and card network policies.

For example, a Vermont-based MSP might waive surcharges for long-standing clients as a gesture of appreciation while applying standard surcharge rates for newer or occasional clients who opt to pay with a credit card.

This level of customization helps Vermont MSPs strengthen client relationships, maintain financial stability, and remain fully compliant with Visa, Mastercard, and federal surcharging guidelines—all while managing processing costs effectively.

Conclusion: Streamlining Payments with Effective Surcharging Strategies

Vermont MSPs can reduce the financial burden of credit card processing fees through surcharging, but compliance remains essential.

Surcharges must be clearly disclosed, properly itemized on invoices, and kept within Vermont’s permitted limits while aligning with federal regulations and card network policies.

To avoid disputes, all surcharges should be transparently displayed on invoices and communicated to clients before payment. Vermont’s surcharge policies, federal laws, and card network regulations—such as Visa’s 3% cap—must be strictly followed.

FlexPoint automates surcharge calculations and seamlessly integrates with invoicing systems, ensuring Vermont MSPs can stay compliant while streamlining financial operations.

Enhance your MSP’s bottom line and compliance with automated credit card surcharging solutions from FlexPoint.

Stay within Vermont’s regulations and simplify your MSP payment processes using FlexPoint today.

Schedule a demo to see how FlexPoint can transform your financial operations and maximize profitability.

{{demo-cta}}

Additional FAQs: Credit Card Surcharging in Vermont for MSPs

{{faq-section}}