As of [$c-month-year]March 2025[$c-month-year], South Dakota MSPs are permitted to apply credit card surcharges to help recover the fees charged by payment processors and manage day-to-day costs.

Adding a surcharge allows MSPs to recoup expenses from credit card transactions instead of taking the hit themselves, while still giving clients the convenience of paying by card.

That said, surcharging must be done carefully. Federal rules and card network regulations, such as those from Visa, Mastercard, American Express, and Discover,place strict conditions on how and when surcharges can be added. Ignoring these requirements could lead to penalties, legal trouble, or strained client relationships.

This guide explains South Dakota’s rules on credit card surcharges, outlines steps MSPs can take to comply with legal and industry standards, and explains how FlexPoint simplifies compliance for MSPs while improving their payment handling.

Disclaimer: This content is provided for general informational purposes only. It does not constitute legal advice. MSPs in South Dakota should consult a qualified legal advisor to understand how surcharging regulations apply to their specific situation.

What is Credit Card Surcharging for MSPs in South Dakota?

In South Dakota, credit card surcharging offers MSPs a practical way to manage rising payment processing costs by shifting some or all of the fees directly to clients.

This practice has been permitted in the state for over a decade. As South Dakota’s consumer protection division explains:

“In 2013, a court settlement between retailers and the credit card industry resulted in merchants being able to pass their payment processing costs to consumers who pay with a credit card.

In South Dakota, a merchant who chooses to exercise this surcharge, sometimes referred to as a "checkout fee," could increase your credit card purchase amount by as much as 4% (the maximum allowed).”

Every credit card transaction carries fees—often between 2% and 4%—that cover interchange fees, card network assessments, and processor markups, so the ability to add surcharges can be very beneficial for MSPs.

Otherwise, those costs can quickly reduce margins for MSPs that handle recurring payments or large monthly volumes of payments.

Consider an MSP in South Dakota that processes $60,000 in credit card transactions per month.

At an average processing fee of 3.1%, the business would pay $1,860 monthly, totaling $22,320 annually, just to accept payments.

If the MSP applies a 3.1% surcharge, it can shift the full cost to clients, reclaiming that $22,320 each year. These savings can support staff training, upgraded cybersecurity tools, or reinvestment in automation, without changing the client’s base pricing.

Some MSPs prefer not to pass the full fee along. Instead, they might apply a partial surcharge—for example, 1.8%—while covering the remainder internally.

In this scenario, the client would absorb $1,080 per month while the MSP still pays $780. Over 12 months, that approach saves $12,960, offering cost recovery without placing the entire burden on the client.

MSPs must comply with disclosure requirements outlined by card networks.

Clients must always see the surcharge amount before they complete a transaction.

If fees are added without notice, MSPs risk client disputes, chargebacks, and possible violations of card acceptance agreements.

MSPs should also monitor card network rules, such as Visa’s 3% cap or signage requirements, and any updates from South Dakota’s consumer protection division.

Although the state permits surcharging, it’s up to the MSP to apply those rules properly and fairly.

The following sections break down South Dakota’s credit card surcharging laws, including how MSPs can stay compliant while protecting their cash flow and client satisfaction.

{{cal-one}}

Understanding Credit Card Surcharging Laws in South Dakota

As of [$c-month-year]March 2025[$c-month-year], South Dakota does not impose any separate surcharge limits beyond what is already permitted at the federal and card brand levels.

This means MSPs can apply a surcharge of up to 4%, provided they don’t exceed their actual processing expenses and comply with the policies outlined by networks like Visa, Mastercard, Discover, and American Express.

Card brands set their own maximums: Visa now limits surcharges to 3%, while Mastercard, Discover, and American Express still allow up to 4%, as long as the fee doesn’t go beyond what the MSP pays to accept that card.

This processing cost, known as the merchant discount rate (MDR), acts as a ceiling for the surcharge.

For example, if an MSP’s payment processor charges 3.2% on American Express transactions, the MSP can apply no more than a 3.2% surcharge to those payments.

Charging beyond that amount would violate network agreements, even if it remains under the 4% federal maximum.

Importantly, surcharges cannot be applied to debit or prepaid cards, regardless of whether the customer chooses to run the card as credit.

This restriction comes from the Durbin Amendment of the Dodd-Frank Act, which prohibits added fees on those types of transactions. Violating this rule can lead to fines or termination of merchant processing privileges.

{{debit-cta}}

In South Dakota, just like elsewhere, transparency is mandatory when applying surcharges.

MSPs must inform clients of the fee before the transaction is processed. This includes clearly stating the surcharge amount during checkout and ensuring it appears as a separate line item on both invoices and receipts.

Failing to follow these rules—whether due to poor disclosure or incorrect application—can expose an MSP to client complaints, chargebacks, or even contractual penalties from payment processors.

In some cases, these missteps can also damage long-term client trust.

If there’s any uncertainty around surcharge implementation, especially regarding signage, caps, or card network compliance, MSPs in South Dakota should consider seeking legal or compliance guidance to avoid unintentional violations.

{{usa-cta}}

Implementing Credit Card Surcharging for South Dakota MSPs

A well-planned surcharge strategy allows MSPs to recover payment processing fees without disrupting client relationships or risking non-compliance.

Below is a step-by-step guide for South Dakota MSPs to apply surcharges correctly

Step 1: Establish a Clear Surcharge Policy and Structure

Start by establishing a formal surcharge policy that outlines the percentage charged, how it’s calculated, and how it will be shown on invoices.

Depending on how billing is structured, South Dakota MSPs can choose from a few common models for applying surcharges:

a) Percentage-Based Surcharge

This model applies a fixed percentage to every credit card payment.

Example: An MSP adds a 3.1% surcharge to all card payments.

If a client’s invoice is $10,000, the surcharge would be $310, resulting in a total of $10,310.

b) Flat Fee Surcharge

Instead of a percentage, a flat dollar amount is added to each credit card payment. This fee must always remain at or below the MSP’s actual processing cost.

Example: The MSP applies a $55 flat fee per credit card transaction. If the client pays a $3,500 invoice, the total comes to $3,555.

However, if the invoice is only $250, and the MSP’s processing cost is 2.9%, they cannot charge more than $7.25. Charging beyond that would violate network rules.

c) Tiered Surcharge Structure

This model uses different surcharge rates depending on the invoice total.

Example: 1.7% on invoices under $4,000 and 2.9% on invoices $4,000 or more

A $2,800 payment would include a $47.60 surcharge (1.7%), while a $5,200 payment would add a $150.80 surcharge (2.9%).

Whichever model is chosen, MSPs should clearly explain it in their service contracts to avoid confusion and maintain full compliance with card network policies.

Step 2: Notify Credit Card Institutions and Clients

Before starting to apply surcharges, South Dakota MSPs must provide proper notice to both their credit card processor (acquirer) and the card networks.

Visa, for example, requires merchants to submit a notice at least 30 days prior to adding a surcharge. This can be done through a short online form.

As Visa states:

“U.S. merchants must first notify Visa and their acquirer of their intent to surcharge at least 30 days before implementing surcharging. Merchants can submit a notification form to Visa.”

Just as important is notifying your clients. Adding a fee without warning can result in disputes, chargebacks, or even lost business.

Disputes like these are expensive—on average, each chargeback costs $190, according to Swipesum.

To avoid this, South Dakota MSPs should communicate surcharge changes clearly and early.

Step 3: Update Invoicing & Billing Systems

Once the policy is defined and notices are sent, invoicing systems must accurately reflect the surcharge. The surcharge must appear as a separate line item so clients can see how it’s calculated and how it affects their total payment.

Example invoice:

- Services Rendered: $9,700

- Surcharge (2.9%): $281.30

- Total Due: $9,981.30

Automated billing platforms are especially helpful here. They reduce human error and ensure surcharges are calculated within compliance limits.

FlexPoint’s billing system can automatically apply the correct surcharge percentage based on the payment method, helping MSPs issue accurate invoices and maintain consistency across all client billing.

Step 4: Monitor and Review Compliance

Surcharging rules aren’t static. Card network policies and processing rates can change, and it’s the MSP’s responsibility to keep their approach compliant.

South Dakota permits surcharges up to the federal limit of 4%, but card networks may impose stricter caps, such as Visa, with a maximum of 3%.

Example: If an MSP pays 2.7% to process Mastercard transactions, they cannot charge 3%. The maximum legal surcharge is 2.7% in this case.

Overcharging—even unintentionally—can trigger fines, require refunds, and result in lost surcharge privileges.

Following these steps helps MSPs apply fees properly while protecting client relationships and staying compliant in South Dakota.

{{ebook-cta}}

The Role of FlexPoint in Streamlining Credit Card Surcharging for South Dakota MSPs

FlexPoint delivers multiple payment solutions that allow South Dakota MSPs to manage processing fees effectively while remaining compliant with state-accepted surcharging practices and card network rules.

Payment Processing Plans

FlexPoint offers two primary billing models designed to suit different financial strategies:

- Interchange+ Plan

- Customer Surcharge Plan

Each option is structured to help MSPs determine whether to internalize processing costs or pass them on in a compliant and transparent way.

a) Interchange+ Plan

MSPs that prefer not to charge their clients extra for credit card payments often select the Interchange+ Plan. This model breaks down the true cost of each transaction and gives complete visibility into the interchange rate and processor markup.

Interchange fees can vary based on factors such as whether the transaction is conducted in person or online, the card brand used, and the card’s reward level.

For example:

A basic Visa debit transaction might cost around 0.9% + $0.12, while a premium travel rewards card from American Express may result in a processing fee of 3.3% + $0.10.

Online payments typically incur higher fees due to elevated fraud risk, while card-present transactions are more affordable.

The Interchange+ model allows MSPs to monitor these fee differences and adjust pricing or internal budgeting as needed. It benefits those who prefer bundling processing costs into their service packages instead of itemizing them on invoices.

Example Scenario

A South Dakota-based MSP processes $48,000 in monthly credit card payments.

With an average interchange rate of 2.85%, the company pays about $1,368 per month, up to $16,416 annually. Using the Interchange+ Plan, the MSP absorbs the fee but gains detailed insight into its cost drivers and maintains flat-rate pricing for clients.

b) Customer Surcharge Plan

For MSPs looking to avoid absorbing these transaction fees, the Customer Surcharge Plan allows them to shift the expense to the client. This approach involves adding a fixed percentage fee to each credit card transaction to fully cover processing costs.

Example Scenario

An MSP in South Dakota processes $72,000 in monthly credit card payments.

With a processing rate of 3%, this results in $2,160 in monthly fees, totaling $25,920 annually.

Applying a 3% surcharge allows the MSP to recover those funds entirely, freeing up that portion of the budget for reinvestment in staffing, equipment, or technology upgrades.

This strategy is particularly helpful for MSPs with tight operating margins or high-dollar service agreements, where absorbing credit card fees would otherwise reduce profitability.

Some MSPs opt for a blended approach: applying a smaller surcharge to clients while covering the rest of the processing fees themselves. This method offers cost relief while keeping additional charges modest for clients.

FlexPoint’s platform makes this hybrid model easy to implement.

Its flexible configuration tools allow MSPs to apply custom surcharge rates, track cost-sharing metrics, and ensure they remain within the allowable limits set by card brands.

Selecting the best-fit model depends on the MSP’s pricing structure, client expectations, and financial goals.

- MSPs prioritizing predictable, all-inclusive service pricing may gravitate toward the Interchange+ Plan.

- Those seeking to eliminate payment processing costs altogether can choose the Customer Surcharge Plan.

- Others may find that a partial surcharge model strikes the right balance, sharing the cost while preserving goodwill.

With FlexPoint, South Dakota MSPs have a payment system that supports both cost management and client transparency, while removing the guesswork from surcharge compliance.

How FlexPoint Enhances Surcharging Compliance and Transparency

FlexPoint simplifies credit card surcharging for MSPs across South Dakota, making sure every surcharge is handled in line with applicable state guidelines, federal rules, and card brand restrictions.

This allows South Dakota MSPs to confidently recover credit card processing fees, knowing they’re staying within the federal 4% limit, Visa’s 3% cap, and other card-specific requirements.

Here’s an example of what a compliant invoice might look like for a South Dakota-based MSP applying a 2.9% surcharge on a $9,750 invoice:

Payment Terms: Payment is due within 30 days of the invoice date. This invoice includes a credit card surcharge applied in accordance with federal law (maximum 4%), South Dakota’s regulatory framework, and card brand rules. Per federal regulations, surcharges are never applied to debit or prepaid cards.

Notes: The surcharge reflects actual credit card processing fees and is shown as a separate line for transparency. If you have questions about this charge or how it’s calculated, contact us at [Your Contact Information].

FlexPoint’s Integration with MSP Tools for Seamless Billing

Automating surcharge tracking is essential for accuracy and efficiency, especially for South Dakota MSPs managing recurring invoices and client accounts.

FlexPoint integrates with many of the most widely used accounting and PSA tools in the MSP industry, helping businesses stay organized and compliant without manual effort.

South Dakota MSPs can easily connect FlexPoint with platforms such as:

These integrations help reduce repetitive tasks, minimize human error, and ensure surcharge information is properly captured at each step—from invoice generation to automated reconciliation.

For instance, if an MSP links FlexPoint with Xero, the system automatically records the credit card surcharge when a payment is processed. There’s no need to adjust the invoice manually or track the surcharge as a separate entry.

During busy billing periods, tracking each card fee manually can slow down operations and introduce inconsistencies. FlexPoint’s automated reconciliation tools help eliminate that risk.

With these integrations in place:

- Payment and surcharge data flow directly into the MSP’s accounting software without manual updates.

- Invoices reflect surcharges as distinct line items, supporting transparency.

- Reports remain up-to-date and audit-ready, helping MSPs avoid discrepancies when preparing taxes or evaluating financial performance.

Client-facing tools matter just as much. A smooth billing experience helps reinforce trust and professionalism.

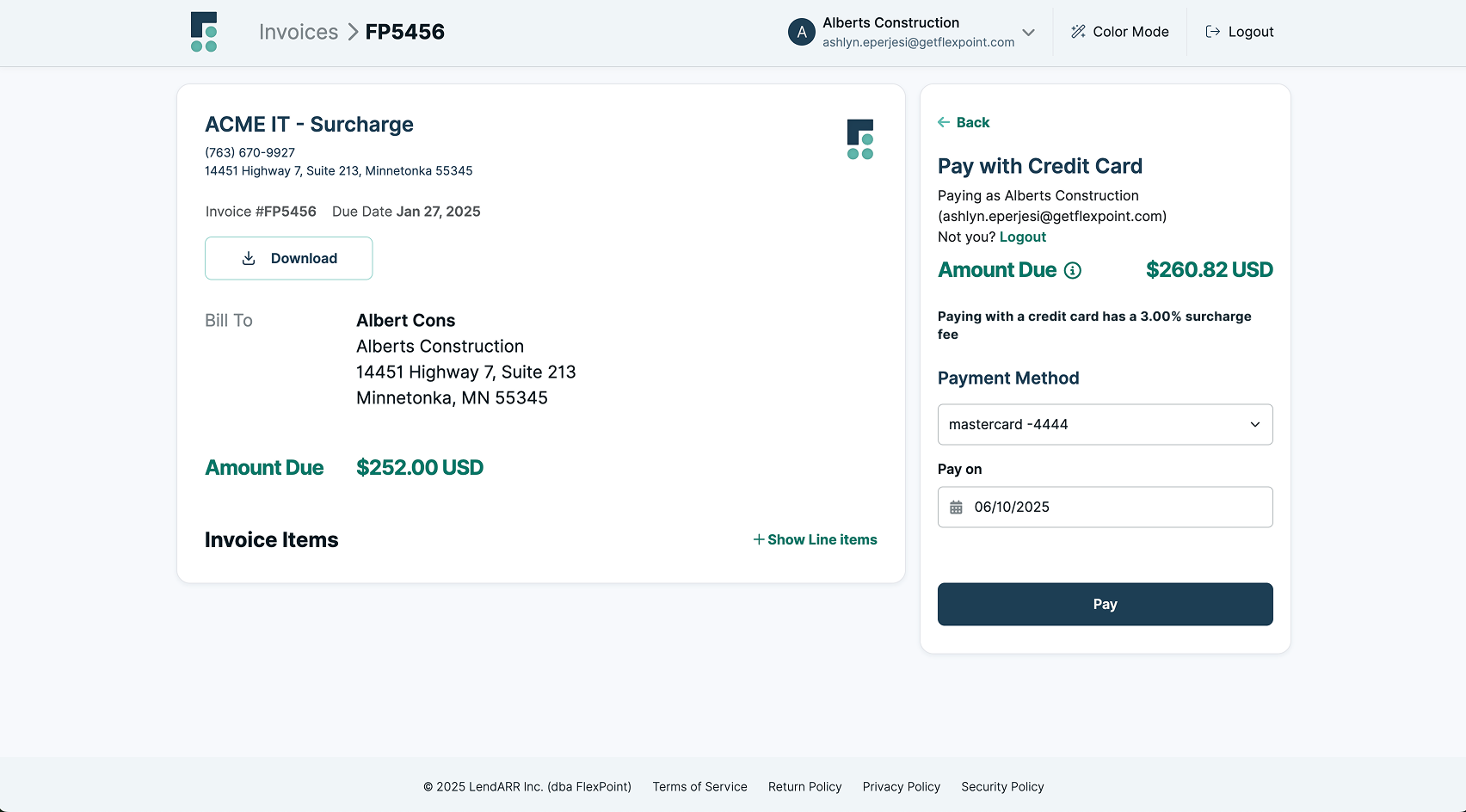

FlexPoint offers custom-branded payment portals, giving South Dakota MSPs a clean, user-friendly interface that clients can use to view and pay invoices, while clearly seeing surcharge amounts and explanations.

These portals allow MSPs to fully comply with surcharge disclosure rules while offering a polished, branded experience that aligns with the rest of their business communications.

The result is a streamlined payment process for MSPs and their clients, with fewer questions, errors, and better long-term retention.

{{client-portal-gif}}

Offering Flexibility in Surcharging

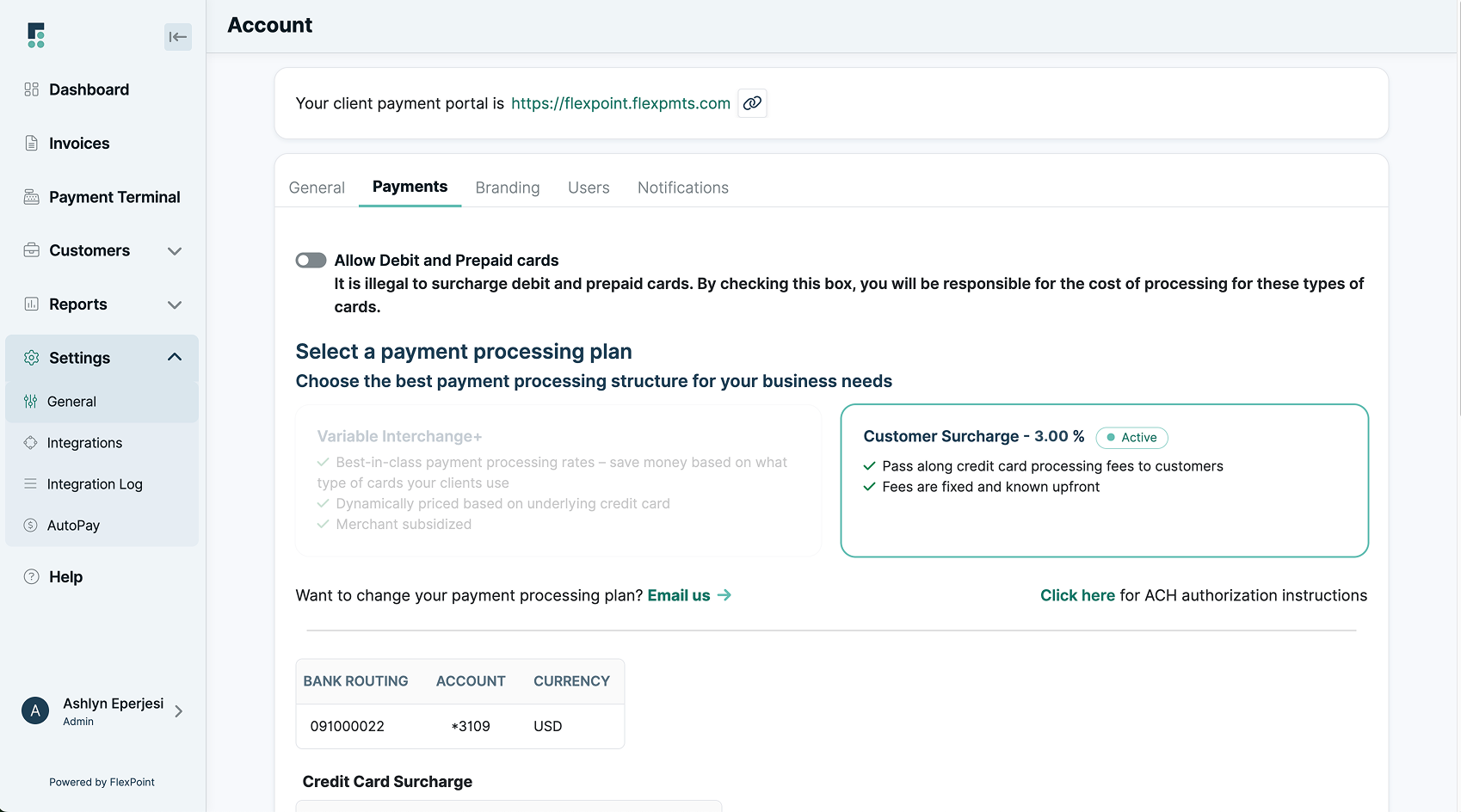

{{admin-portal-gif}}

FlexPoint gives South Dakota MSPs the flexibility to apply surcharges thoughtfully, helping them manage payment costs without straining client relationships.

Instead of applying a flat surcharge across every client and transaction, MSPs can tailor their surcharge strategies based on factors like payment method, client type, or contract value.

This adaptive strategy helps MSPs preserve strong relationships with key accounts while still recovering processing costs in other areas of the business. It also allows room for flexibility when onboarding new clients or renegotiating service terms.

Conclusion: Streamlining Payments with Effective Surcharging Strategies

For MSPs in South Dakota, a strong surcharging strategy requires thoughtful planning, clear communication, and reliable automation.

When done right, surcharging becomes a tool for protecting margins without surprising clients. It allows MSPs to recover processing costs while offering a consistent, professional billing experience that supports long-term business growth.

Enhance your MSP’s bottom line and compliance with automated credit card surcharging solutions from FlexPoint. Stay within South Dakota’s regulations and simplify your MSP payment processes using FlexPoint today.

Schedule a demo to see how FlexPoint can transform your financial operations and maximize profitability.

{{demo-cta}}

Additional FAQs: Credit Card Surcharging in South Dakota for MSPs

{{faq-section}}