Credit card processing fees can be a considerable expense for businesses in Pennsylvania, and many MSPs choose to implement credit card surcharging to recover some of these costs.

Otherwise, this expense greatly impacts profits, particularly when managing high transaction volumes and recurring billing. Surcharging offers a way to lower these costs and enhance financial efficiency.

Pennsylvania permits surcharging as of [$c-month-year]May 2025[$c-month-year], but MSPs must follow state and federal regulations to remain compliant. Further card networks (Visa, Mastercard, and American Express) also impose strict rules on surcharges, which MSPs must adhere to to avoid penalties.

This article explains how Pennsylvania MSPs can comply with surcharging laws, includes valuable steps for implementation, and highlights how payment automation tools make invoice management and surcharging more efficient.

Disclaimer: This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for, legal advice. Perform thorough due diligence and consult with a qualified legal professional to address specific questions related to your MSP.

What Is Credit Card Surcharging for MSPs in Pennsylvania?

Managed service providers in Pennsylvania frequently process credit card payments, particularly for subscription-based services and recurring payments.

While credit cards provide convenience and speed, the associated processing fees can add up, seriously reducing profitability.

Credit card surcharging allows MSPs to offset these costs by passing a portion of the processing fees to clients who choose to pay with a credit card.

This approach ensures MSPs are not absorbing the full burden of transaction fees, preserving their margins while offering flexible payment options.

Payment processing costs, which include interchange and assessment fees, typically total between 2 and 4% of the total transaction cost.

Consider an MSP that invoices a client for $7,200 and applies a 2.5% surcharge. The final amount due would be $7,380, with the additional $180 helping to cover transaction costs.

For MSPs managing a high volume of transactions, implementing a surcharge strategy can significantly improve cost recovery.

For example, an MSP that processes $135,000 in monthly credit card transactions and pays an average processing fees of 3%; and applies a full 3.0% surcharge could recover $4,050 each month, totaling $48,600 annually—revenue that would otherwise be lost to processing fees.

Alternatively, by choosing to implement a partial surcharge of 1.5%, the MSP would still recoup $2,025 per month, or $24,300 per year. While this doesn’t offset the entire cost of credit card processing, it does substantially reduce the financial burden. This approach can also help maintain stronger client relationships, as it shares the cost in a more balanced way.

However, surcharging must be implemented carefully.

While it can improve financial efficiency, MSPs must comply with Pennsylvania regulations and ensure client transparency. Disclosing surcharge fees in advance prevents disputes and maintains trust.

If they take the time to structure their surcharging policy correctly, Pennsylvania MSPs could manage costs effectively while maintaining healthy client relationships.

{{cal-one}}

Understanding Credit Card Surcharging Laws in Pennsylvania

Pennsylvania permits businesses, including MSPs, to apply surcharges on credit card transactions (as of [$c-month-year]May 2025[$c-month-year]). However, this is not without strict guidelines that must be followed.

These requirements assure consumer transparency while preventing excessive fees that could discourage credit card use.

While Pennsylvania does not impose additional state-specific restrictions beyond federal regulations, MSPs must still adhere to policies set by credit card networks such as Visa and Mastercard.

Here are some of the fundamental requirements for surcharging in Pennsylvania:

- Surcharge Disclosure: MSPs must inform clients about surcharges before processing a transaction. This includes displaying clear signage on invoices or showing surcharge details before checkout in the case of online payments.

- Invoice Transparency: Surcharges must appear as a separate line item on all invoices and receipts, ensuring clients understand the additional fee.

Debit and Prepaid Cards Excluded: Under the Durbin Amendment of the Dodd-Frank Act, surcharges cannot be applied to debit or prepaid card transactions, even if the payment is processed as a "credit" transaction.

{{debit-cta}}

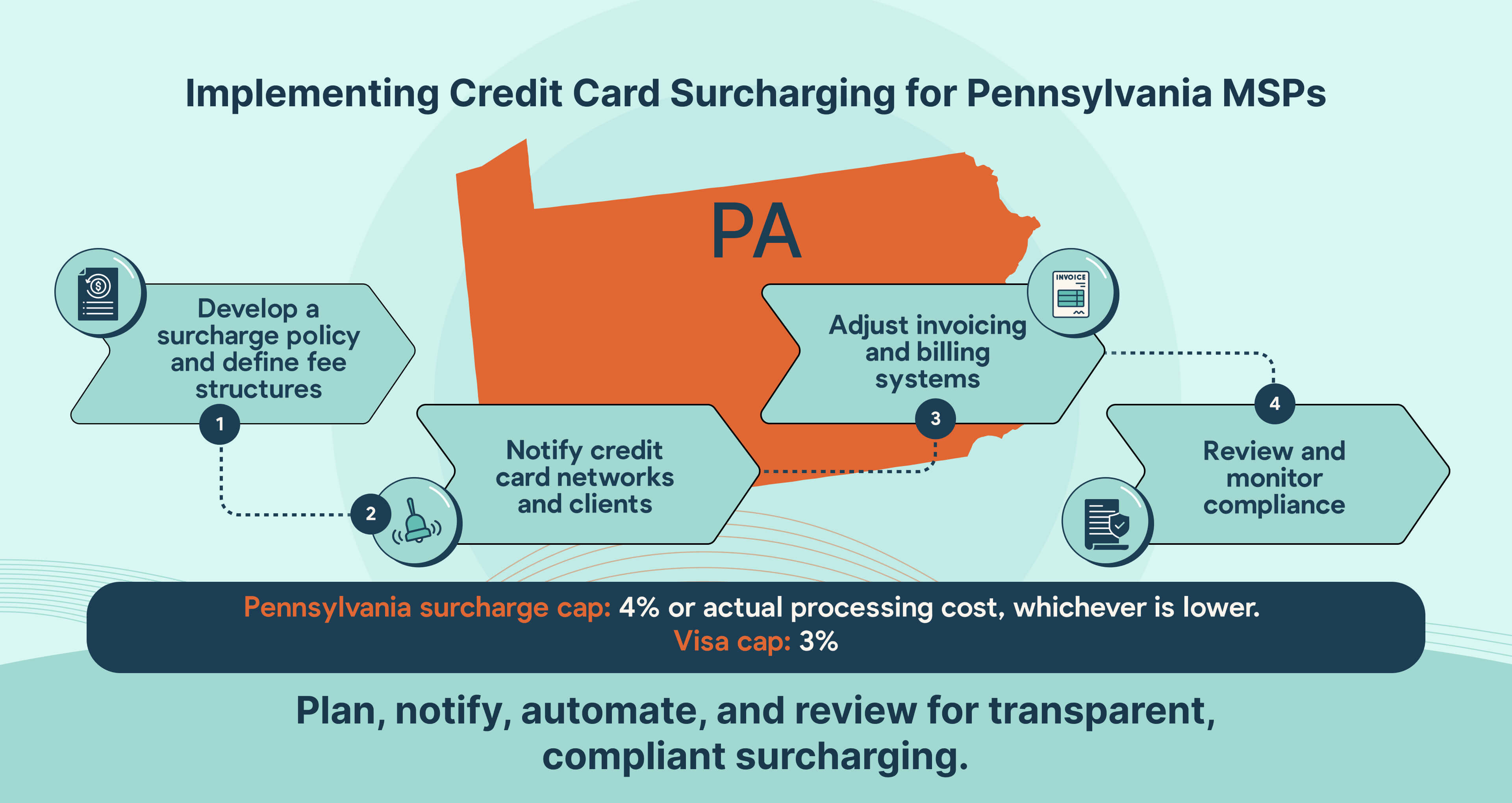

- Surcharge Limits: The surcharge cannot exceed 4% of the total transaction amount or the actual processing fee, whichever is lower. However, Visa caps surcharges at 3%, meaning Pennsylvania MSPs must be mindful of this limit when processing payments.

For example, if an MSP invoices a client for $12,000 and applies a 3% surcharge, the total charge would be $12,360. If the actual processing fee is only 2.8%, the surcharge must be adjusted to match that amount rather than applying the full 3%.

Failing to comply with surcharge regulations leads to penalties, disputes, and chargebacks.

Pennsylvania MSPs must align surcharge policies with state laws, federal regulations, and credit card network rules. If you are unsure of your surcharging options in Pennsylvania, we recommend consulting with a lawyer or qualified legal professional.

{{usa-cta}}

Implementing Credit Card Surcharging for Pennsylvania MSPs

Adding a credit card surcharge requires cautious planning, compliance with regulations, and straightforward client communication.

A surcharge alone will not prevent potential payment issues. MSPs need clear invoicing practices and upfront explanations to ensure clients understand the additional charge.

A PYMNTS study found that 70% of consumers react negatively to surcharges, and nearly 40% would consider switching to a provider that does not impose them.

Because of this, MSPs must strike a balance—recouping costs while maintaining strong client relationships.

The following guide helps Pennsylvania MSPs integrate surcharging into their billing process while ensuring compliance and client satisfaction.

Step 1: Develop a Surcharge Policy and Define Fee Structures

Having a defined surcharge policy prevents inconsistencies and payment disputes. Including this policy in contracts ensures clients know how and when fees will be charged.

Pennsylvania MSPs can design surcharge structures based on business needs, adjusting fees for different transaction levels, client segments, or payment types.

Typical models include:

a. Fixed Percentage Surcharge

A standard percentage is applied to all credit card transactions.

Example: An MSP charges 3% on all invoices.

- A $7,000 invoice would include a $210 surcharge, making the total $7,210.

b. Tiered Surcharge System

The surcharge varies based on the invoice amount.

Example: An MSP charges 2% on invoices under $4,000 and 3% on invoices above $4,000.

- A $3,600 invoice would include a $72 surcharge (2%).

- A $5,500 invoice would include a $165 surcharge (3%).

c. Flat Fee Surcharge

A flat fee surcharge allows MSPs to charge a set fee instead of a percentage-based amount for credit card transactions.

A flat fee surcharge allows MSPs to charge a set fee instead of a percentage-based amount for credit card transactions.

Example: A $40 flat fee is applied to every invoice. If a client is invoiced $5,500, the total amount after surcharging would be $5,540.

To meet compliance standards, the surcharge must not exceed the 4% limit, 3% for Visa payments, or the actual processing cost (merchant discount rate or MDR).

For instance, if an MSP applies a $40 surcharge to a $500 transaction, the charge would exceed legal limits. Instead, the surcharge should be capped at $20 or less.

Pennsylvania MSPs using flat fee surcharges must regularly review processing costs to confirm their fees remain compliant while maintaining transparency with clients.

Choosing the right surcharge model depends on the MSP’s billing structure and client relationships.

Step 2: Notify Credit Card Networks and Clients

Pennsylvania MSPs must inform card networks (Visa, Mastercard, Discover, and American Express) at least 30 days in advance before implementing surcharges.

For example, Visa requires MSPs to submit a notification form to Visa and their acquiring bank at least 30 days before implementing surcharging.

Clients must also be informed in advance. A well-structured communication plan dissuades misunderstandings and chargebacks.

Below is an example of how an MSP might introduce the concept of surcharging to its clients:

“Beginning [date], a 3% surcharge will be applied to all credit card payments. This fee helps offset rising transaction costs and ensures we can continue offering seamless service. Clients may avoid this fee by paying via ACH or check.

Please note that surcharging is not a profit-generating measure. Rather, it helps us offset rising payment processing costs without having to raise our service rates across the board.

We remain committed to providing cost-effective solutions while maintaining transparency in our billing practices.

If you have any questions or would like to discuss alternative payment options, please reach out to our billing department at [contact information]. Thank you for your continued partnership.”

Failing to disclose surcharges upfront can lead to disputes and a loss of trust.

If clients receive an invoice for $9,000 but notice an unexpected $270 surcharge, they may initiate a chargeback, assuming the charge was added in error.

Since, according to Swipesum, the average chargeback costs businesses $190 per dispute, proactive communication helps prevent financial losses and maintains client trust.

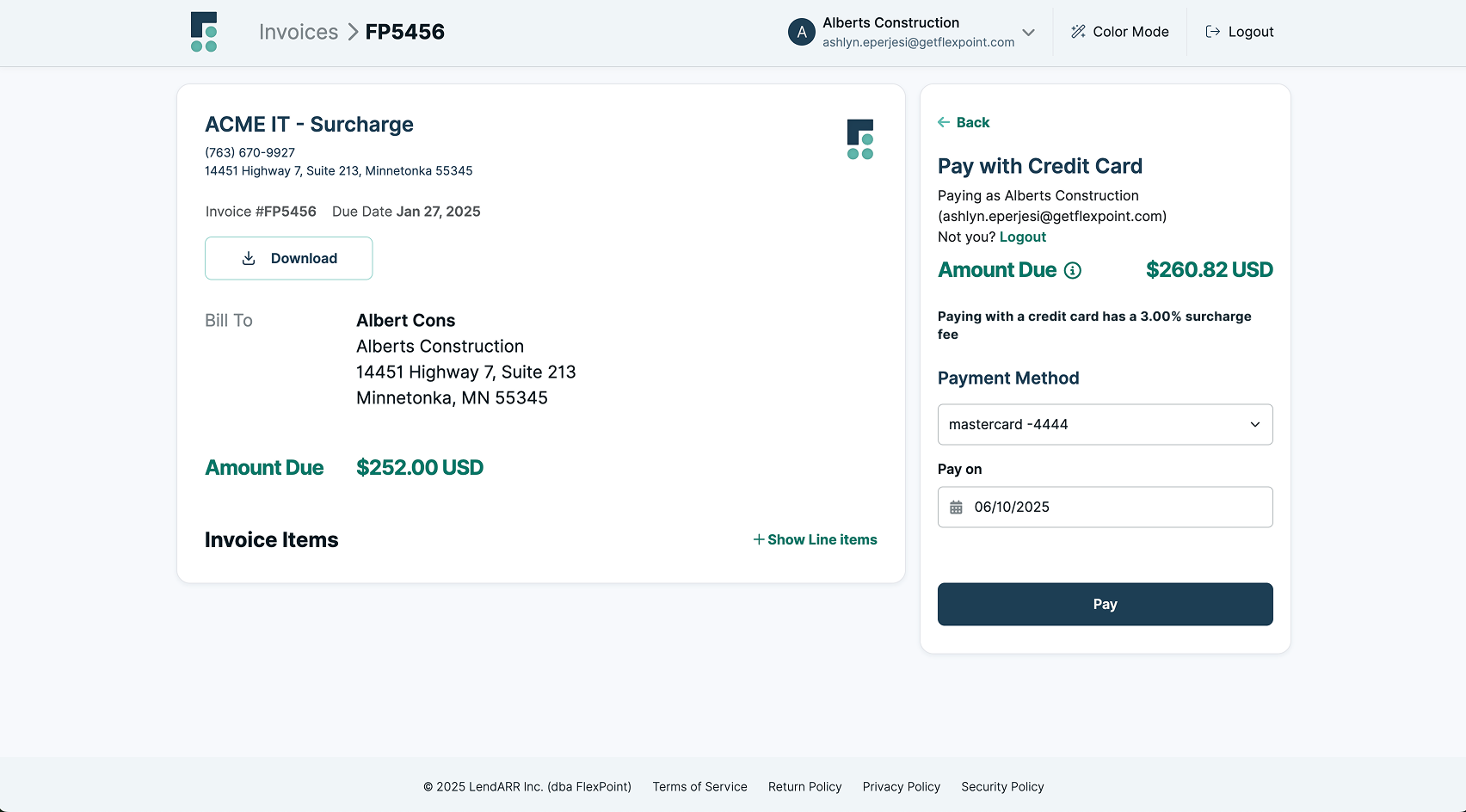

Step 3: Adjust Invoicing and Billing Systems

Pennsylvania MSPs should itemize surcharges on invoices to align with state regulations. Separating these fees ensures clients see what they are paying and why it is applied.

For example, an invoice for $6,200 with a 3% surcharge should list:

- Service Fee: $6,200

- Credit Card Surcharge (3%): $186

- Total Due: $6,386

Payment automation tools like FlexPoint simplify surcharge calculations and ensure they are correctly integrated into invoices. This minimizes manual payment errors and helps MSPs stay compliant with surcharge rules.

Using automation, MSPs ensure accuracy and avoid miscalculations that lead to compliance issues or client dissatisfaction.

Step 4: Review and Monitor Compliance

Staying compliant with surcharging laws requires ongoing effort, as both state and federal regulations change quickly.

Pennsylvania MSPs must monitor evolving laws and updates from card networks like Visa and Mastercard to avoid noncompliance and potential penalties.

Changes may come from regulatory agencies like the Consumer Financial Protection Bureau (CFPB) or state lawmakers.

While Pennsylvania currently allows surcharging, future legislative updates could impose new restrictions or disclosure requirements.

MSPs should regularly review their surcharging policies and make adjustments as needed.

Some of the most important regulations and practices (in place as of [$c-month-year]May 2025[$c-month-year]) to keep in mind include:

- Following surcharge limits: Visa caps surcharges at 3%, while Mastercard allows up to 4%. However, an MSP cannot charge more than its actual processing fees.

- Matching merchant discount rates (MDR): If an MSP’s processing cost is 2.7%, it cannot apply a 3% surcharge, even if state laws or card networks allow a higher percentage.

- Reviewing client agreements: Any changes to surcharge rules should be reflected in service agreements. MSPs should notify clients when surcharge policies are updated.

- Addressing client concerns: If clients raise concerns or request clarification about surcharges, MSPs should explain the fees and how they help offset payment processing costs.

Failure to comply with these rules could result in fines, payment disputes, and chargebacks, which could lead to unnecessary expenses for the MSP.

Pennsylvania MSPs can avoid surcharge miscalculations by integrating FlexPoint, an MSP-specific payment automation tool that applies surcharges accurately, adheres to legal limits, and provides clear invoice breakdowns.

{{ebook-cta}}

The Role of FlexPoint in Simplifying Credit Card Surcharging for Pennsylvania MSPs

Payment processing fees are a recurring expense for Pennsylvania MSPs, cutting into revenue with every credit card transaction. These costs add up, especially for MSPs that rely on recurring billing.

To manage expenses without disrupting cash flow, MSPs need a strategic approach to payment processing.

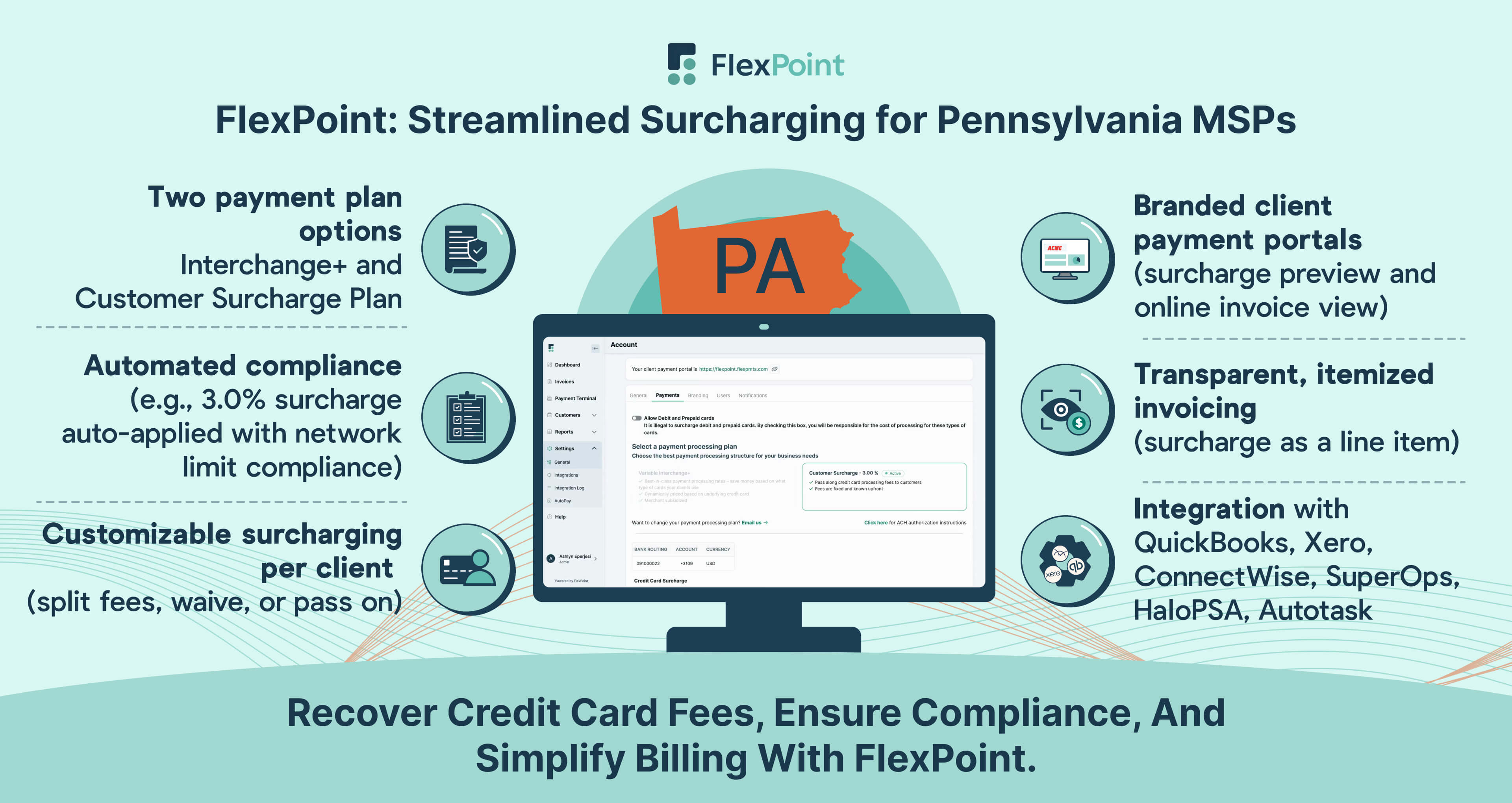

FlexPoint provides a tailored solution that simplifies billing and allows MSPs to choose between pricing models.

Whether an MSP prefers to absorb credit card fees or pass them on to clients, FlexPoint offers flexible options to fit their needs.

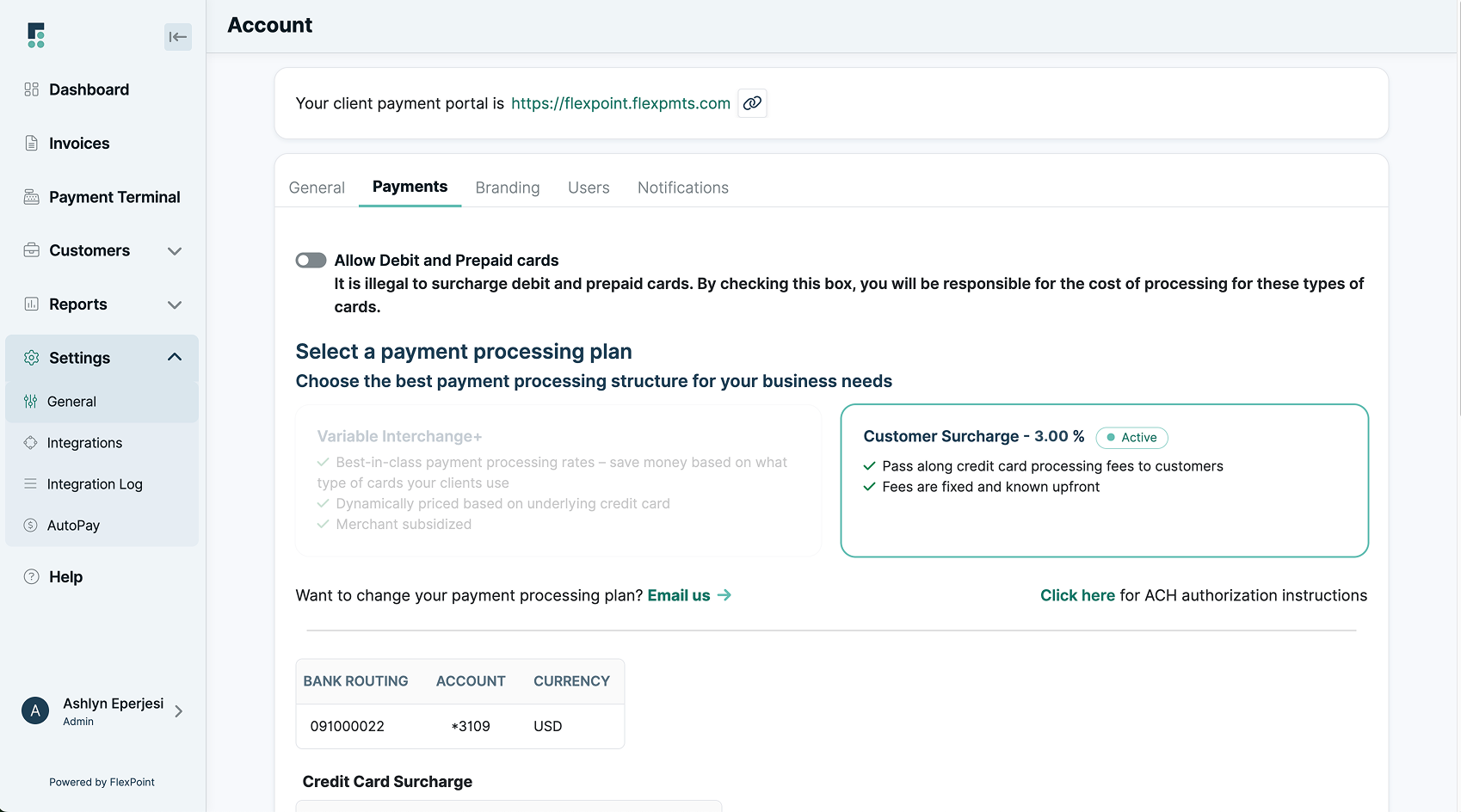

Flexible Surcharge Options for MSPs

Pennsylvania MSPs can select from two primary payment models based on how they prefer to handle transaction costs:

- Interchange+ Plan

- Customer Surcharge Plan

a. Interchange+ Plan

This plan structures pricing based on interchange rates, allowing MSPs to pay fees that vary depending on the type of credit card used.

For example:

- A transaction with Discover might carry a lower interchange rate, reducing processing costs.

- Payments made with American Express or high-reward credit cards typically have higher rates, increasing the cost of accepting those cards.

MSPs that prefer to absorb transaction fees rather than impose surcharges find this model most beneficial.

The Interchange+ Plan provides greater financial transparency and predictability, helping MSPs budget for payment processing expenses.

b. Customer Surcharge Plan

The Customer Surcharge Plan applies a percentage-based surcharge on credit card payments for MSPs looking to shift transaction fees to clients.

Example:

A Pennsylvania MSP processes a $6,800 transaction and applies a 2.5% surcharge:

- Service Total: $6,800

- Surcharge (2.5%): $170

- Total Due: $6,970

This approach relieves the MSP’s financial burden by offsetting processing fees.

FlexPoint also provides a cost-sharing feature, enabling MSPs to divide surcharges with clients. This approach softens the transition to surcharging while preserving strong client relationships.

FlexPoint helps MSPs comply with Pennsylvania’s surcharging laws and credit card network policies regardless of which plan an MSP chooses.

The platform automates surcharge calculations, ensuring fees are applied accurately and displayed clearly on invoices.

Pennsylvania MSPs minimize transaction costs while maintaining strong client relationships with the right payment strategy.

Whether covering processing fees with an Interchange+ Plan or applying surcharges, FlexPoint provides the tools to simplify payment management and improve financial stability.

How FlexPoint Enhances Compliance and Transparency

FlexPoint helps Pennsylvania MSPs manage surcharging while complying with state laws, federal regulations, and card network policies.

The platform automates surcharge calculations, ensuring charges do not exceed Pennsylvania’s 4% cap or the processing costs incurred.

By itemizing surcharges on invoices and integrating seamlessly with financial systems, FlexPoint reduces errors and keeps clients informed about their payments.

Pennsylvania MSP Client INVOICE

For a $12,500 invoice with a 3% surcharge, FlexPoint could calculate and display charges like this:

Notes:

- Surcharges apply only to credit card transactions and will not be charged on debit card payments.

- The surcharge will not exceed the actual processing cost for accepting credit cards.

- Clients with questions or concerns about surcharges can contact billing support at (XXX) XXX-XXXX or via email at support@example.com.

FlexPoint enables Pennsylvania MSPs to automate surcharge compliance, improve invoice transparency, and maintain client trust while reducing financial strain from processing fees.

FlexPoint’s Integration with MSP Tools for Seamless Billing

Managing invoicing and payment records manually can be time-consuming and prone to errors.

FlexPoint eliminates these inefficiencies by integrating with widely used accounting and business management platforms, allowing Pennsylvania MSPs to automate financial tasks.

Compatible platforms include:

By integrating these systems with FlexPoint, MSPs can eliminate redundant data entry, automate surcharge calculations, and keep transaction records current.

For example, when an MSP processes a client’s credit card payment through FlexPoint, the surcharge is automatically applied and reflected in their QuickBooks Online records.

This removes the need for manual adjustments and ensures billing accuracy.

Automated reconciliation also means all payments, fees, and surcharges are categorized correctly, allowing MSPs to generate reports confidently.

FlexPoint reduces administrative burdens and improves financial transparency, helping Pennsylvania MSPs focus on delivering quality service rather than managing payment complexities.

Providing MSPs with branded client payment portals and live financial tracking tools simplifies transaction management and further enhances visibility into their financial health.

{{client-portal-gif}}

Offering Flexibility in Surcharging

{{admin-portal-gif}}

FlexPoint permits Pennsylvania MSPs to tailor surcharging policies based on client relationships. MSPs can waive surcharges for loyal, long-standing clients while applying them to newer accounts or those with infrequent transactions.

FlexPoint automatically applies surcharges within permitted limits set by Visa, Mastercard, and other card networks to prevent compliance issues.

For instance, if a client pays with Mastercard, the surcharge might be set at 2.75%, aligning with the processing rate and staying within Mastercard’s 4% cap.

This automation ensures regulatory compliance and streamlines payment processing, reducing errors and disputes.

Clients gain complete visibility into their payments through FlexPoint’s branded portals, where they can review invoices, see surcharge details, and manage their payment preferences.

Additionally, clients have the flexibility to update payment methods at their convenience.

If clients frequently use a high-reward credit card but want to avoid surcharges, they may opt for an ACH payment instead. This adaptability also strengthens trust between MSPs and their clients while improving cash flow management.

FlexPoint’s automated surcharging solutions enhance operational efficiency, simplify compliance, and cultivate better client communication for Pennsylvania MSPs.

With these tools, MSPs can focus on delivering exceptional service, knowing their financial processes are optimized.

Conclusion: Streamlining Payments with Effective Surcharging Strategies

For Pennsylvania MSPs, credit card surcharging offers a functional way to offset processing fees.

Nevertheless, implementing surcharges correctly demands meticulous planning, communication, and adherence to federal, state, and card network regulations.

To uphold transparency, managed service providers must disclose surcharges upfront and itemize them on invoices.

Additionally, staying within permitted surcharge limits prevents disputes and ensures compliance with regulations from Visa, Mastercard, and other networks.

FlexPoint simplifies this process by providing an automated payment platform designed specifically for MSPs.

From accurate surcharge calculations to seamless invoice integration, FlexPoint helps Pennsylvania MSPs apply surcharges while reducing administrative workload and ensuring compliance with all applicable laws.

Enhance your MSP’s bottom line and compliance with automated credit card surcharging solutions from FlexPoint.

Stay within Pennsylvania’s regulations and simplify your MSP payment processes using FlexPoint today.

Schedule a demo to see how FlexPoint can transform your financial operations and maximize profitability.

{{demo-cta}}

Additional FAQs: Credit Card Surcharging in Pennsylvania for MSPs

{{faq-section}}