In New York, credit card surcharging has shifted from a flat-out prohibition to a legally permissible practice since February 11, 2024—but only under tightly defined conditions. For managed service providers (MSPs), this change requires a deliberate review of pricing strategies and disclosure methods to ensure full compliance with the new requirements.

The state’s revised General Business Law § 518 outlines the legal framework, and both civil penalties and consumer protection authorities back enforcement.

To avoid enforcement issues, MSPs must treat surcharge policies as a formal part of their billing setup. This applies to each instance where the posted credit card price is missing or misrepresented, or where the surcharge exceeds the allowable rate.

To remain compliant and reduce the administrative burden, MSPs often turn to billing software that automates surcharge workflows. With these tools, New York MSPs can apply rules uniformly, calculate card brand-specific fees accurately, and maintain consistent disclosures across invoices.

This guide presents the framework New York-based MSPs must follow when legally surcharging credit card transactions. It also explores how automation platforms, particularly those tailored for MSP needs, can simplify compliance by embedding fee calculations into the billing process, standardizing client communication, and reducing human error.

Disclaimer: This content is intended for informational purposes only and should not be taken as legal counsel. MSPs operating in New York should consult with legal professionals and refer to the updated language of GBL § 518 and other applicable consumer protection statutes to ensure all surcharge practices are lawful and correctly disclosed.

What is Credit Card Surcharging for MSPs in New York?

Credit card processors and payment gateways typically charge transaction fees ranging from 2% to 4%, depending on the merchant's payment volume and the card type.

These fees can quickly erode margins for MSPs managing larger invoices or handling high-volume recurring payments.

Due to New York’s updated General Business Law § 518, MSPs can now recover those expenses by passing the fee to the client via credit card surcharging—as long as it’s clearly disclosed, does not exceed the actual cost to process the card, and is presented in line with the statute’s strict transparency rules.

Here’s how that might work for a New York-based MSP:

Suppose your MSP processes $150,000 in monthly credit card payments for IT services. With a 3.2% processing fee, you’d pay $4,800 each month to your payment processor. By applying a full 3.2% surcharge, you recover the entire $4,800 in fees; thus, allowing you to keep the full $150,000 in revenue.

Multiply that recovery across the year, and you’re looking at $57,600 in annual savings; money that can be reinvested into your business instead of going to processing costs.

If you prefer to share the cost with clients, you could apply a partial surcharge of 1.6% instead. This would allow you to recover $2,400 per month, or $28,800 annually. This is still a substantial reduction in your expenses while keeping part of the cost off your clients.

Whether you choose to recover all or part of your fees, surcharging gives you flexibility to protect your margins while staying compliant with industry regulations.

In an industry where margins are often squeezed by overhead and rising operational costs, the ability to reclaim card processing fees can protect profitability.

For MSPs operating in New York, this is a smart strategy, and it’s also a legally supported one when executed within the framework of GBL § 518 (which we will expand on in detail in the next section).

The key is transparent execution. The credit card price must be clearly posted on your invoice, service agreement, website checkout screen, or client portal, and include the full amount the client will pay. MSPs that rely on automated billing systems or service platforms should ensure those tools reflect compliant pricing structures.

When properly disclosed, legally justified, and integrated into your billing process, credit card surcharging in New York can become a valuable tool for cost recovery and enhancing long-term financial resilience.

{{cal-one}}

Understanding Credit Card Surcharging Laws in New York

For MSPs in New York, handling credit card surcharges means staying aligned with both card network requirements and the state’s updated disclosure laws.

While New York’s General Business Law § 518 doesn’t assign a specific numerical cap like some states, it still imposes a functional ceiling: MSPs can never charge more than their actual cost to process a credit card transaction.

Even if another platform or outdated signage references a 4% rate, applying more than your processing cost is considered noncompliant and potentially deceptive under New York’s broader consumer protection rules.

The percentage matters, but how that amount is communicated makes or breaks compliance.

Below, we break down New York’s specific requirements, what’s considered legal or illegal under the new guidelines, and the implications for MSPs, including how tools like FlexPoint can help automate compliance.

For more information and guidance, you can also view an explanatory video on the NYS Department of State’s CreditCard Surcharge Guidance page.

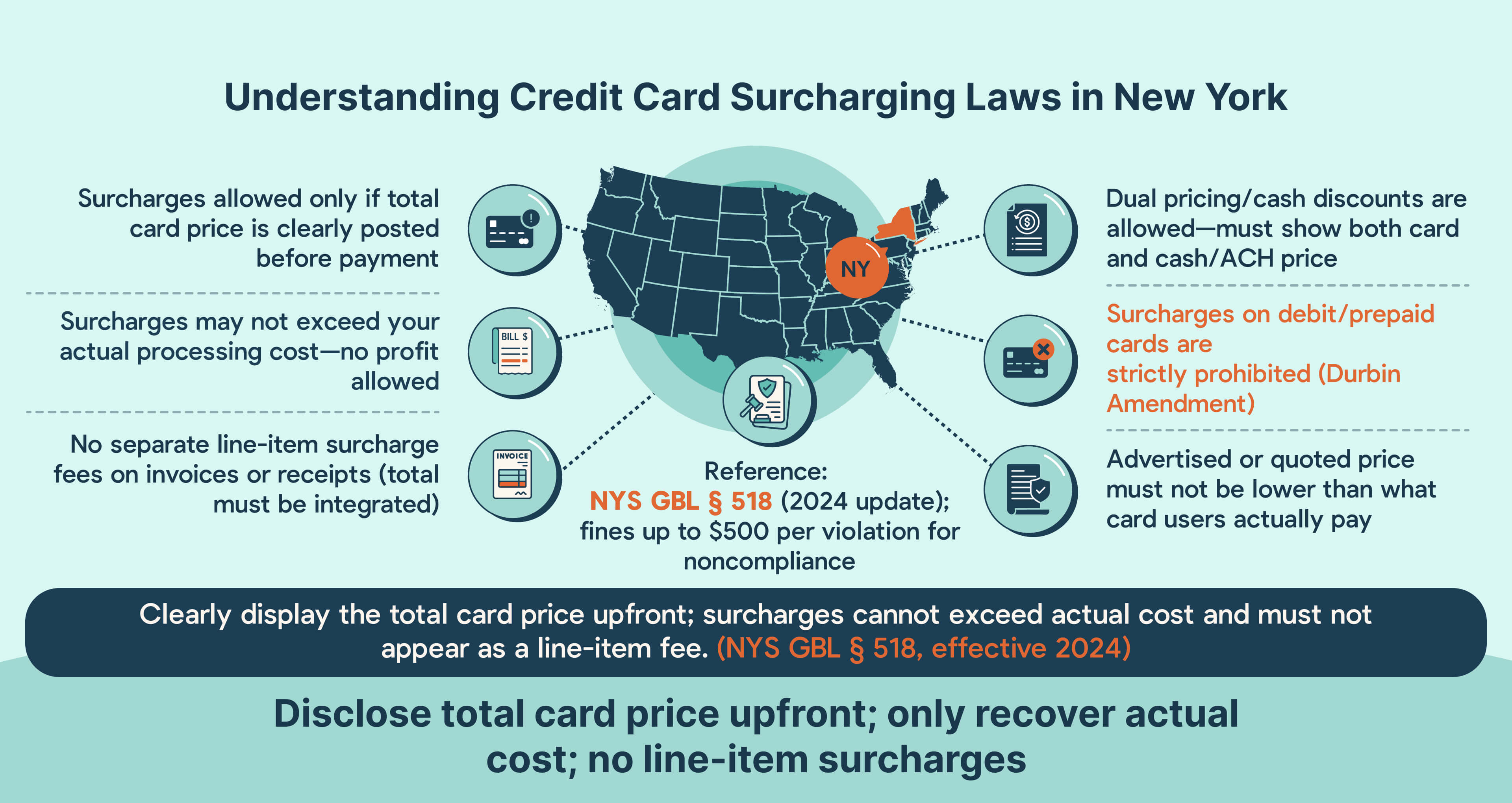

Key Provisions of NYS GBS § 518 Effective February 11, 2024

New York’s updated law explicitly permits MSPs and other businesses to add a credit card surcharge only under strict conditions, ensuring complete transparency and consumer protection.

NYS GBL § 518 (as of [$c-month-year]April 2025[$c-month-year]) requires the following:

- Clear Disclosure of Total Price: If you impose a surcharge, you must clearly and conspicuously post the total price a client will pay when using a credit card, including the surcharge. Clients should be informed of the total payment cost by card (excluding standard sales tax) before proceeding with the payment.

- No Exceeding Actual Cost: The surcharge cannot exceed the actual cost incurred by the MSP to process the credit card transaction. You are only allowed to pass on the charges the card company imposes on you (e.g., interchange and processing fees), and nothing more.

- Posted Price Limit: The final price, including the surcharge, cannot exceed any price you’ve publicly posted for the service. Practically, this means if you advertised or listed a price for your services, you can’t add a surcharge on top of that posted base price unless the posted price already accounted for the card fee.

- Penalty for Violations: Failure to follow these rules can result in enforcement actions. The updated law authorizes fines of up to $500 per violation. New York’s state and local consumer protection authorities can enforce these penalties, so non-compliant surcharging can quickly become costly.

Example: An MSP in New York bills a client $5,000 for an IT infrastructure project.

If the MSP’s credit card processing fee is 3.5%, the MSP can legally offer a credit card payment option at a total of $5,175 (which includes a 3.5% surcharge, approximately $175).

The $5,175 figure – the full price for paying by card – must be clearly disclosed on the invoice or payment page before the client makes a payment.

At the same time, the MSP should note that the amount due is $5,000 if paid by check or ACH, with no surcharge.

This way, the client sees the complete credit card price upfront and can make an informed decision.

The surcharge in this example exactly recovers the MSP’s processing cost (3.5% of $5,000) and does not exceed it, satisfying New York’s requirements.

What’s Legal vs. Illegal Under New York’s Updated Guidelines

New York’s law sharply distinguishes between acceptable and unacceptable surcharge practices.

MSPs must adhere to these guidelines from the Department of State Consumer Protection to stay compliant:

Allowed Practices:

- Dual Pricing: You may display one price for credit card payments and a lower price for cash, check, or ACH payments. For example, an MSP could quote a service at $1,030 for credit card payment and $1,000 for cash or ACH. This is effectively a built-in 3% cash discount off the higher credit price.

- Cash Discounts: Similarly, it’s legal to advertise that you offer a discount for cash payments on a higher regular price. In practice, this is just another way of framing dual pricing – the key is that the client who pays with a card is paying the posted higher price, not a surprise add-on fee.

- Same Price for All Payments: Of course, it’s always legal to charge the same price regardless of payment method (i.e., not implement any surcharge at all).

Prohibited Practices:

- Adding Undisclosed Surcharges at Payment Time: You cannot advertise or quote one price to a client and then simply add a surcharge without prior disclosure at the time of payment. New York prohibits placing a generic notice, such as “a 3% credit card fee will be added,” on a sign or invoice without listing the actual higher price the client will pay.

- Line-Item Surcharge Fees on Receipts: It is illegal to list the credit card surcharge as a separate line item on the client’s receipt or invoice (e.g., a line for “Credit Card Processing Fee: $X”). The total price with the fee should instead be presented as a single integrated amount for those paying by card.

- Misleading Price Listings: You cannot post signage or tags that imply a lower price while hiding the higher credit price. All clients must be able to see the applicable price for credit card payment without any misleading statements.

Surcharging Debit Cards: Debit cards cannot be surcharged under any circumstances in New York (or any other state). Even if a debit card is run “as credit” (without a PIN), it should not incur a surcharge fee. This prohibition comes from federal regulations and card network rules that treat debit transactions differently.

{{debit-cta}}

The updated New York law aims to ensure transparency, so any attempt to hide the surcharge or spring it on clients is both illegal and harmful to an MSP’s reputation.

Implications for MSPs in New York

For MSPs operating in New York, these rules mean that surcharging is a viable cost-recovery strategy, but it must be implemented carefully and per the regulations. The good news is that by following the law, MSPs naturally foster greater transparency with their clients.

When clients see a clearly labeled credit card price versus a cash price, it builds trust that the MSP is not padding invoices, but simply passing through third-party costs. This can lead to more informed discussions with clients about payment methods.

Some clients may choose to switch to ACH or check to avoid the surcharge, saving the MSP even more in fees, while others will appreciate the convenience of credit card payment and understand the added cost.

If you are unsure of your surcharging options in New York, we recommend consulting with a lawyer or qualified legal professional.

{{usa-cta}}

Implementing Credit Card Surcharging for New York MSPs

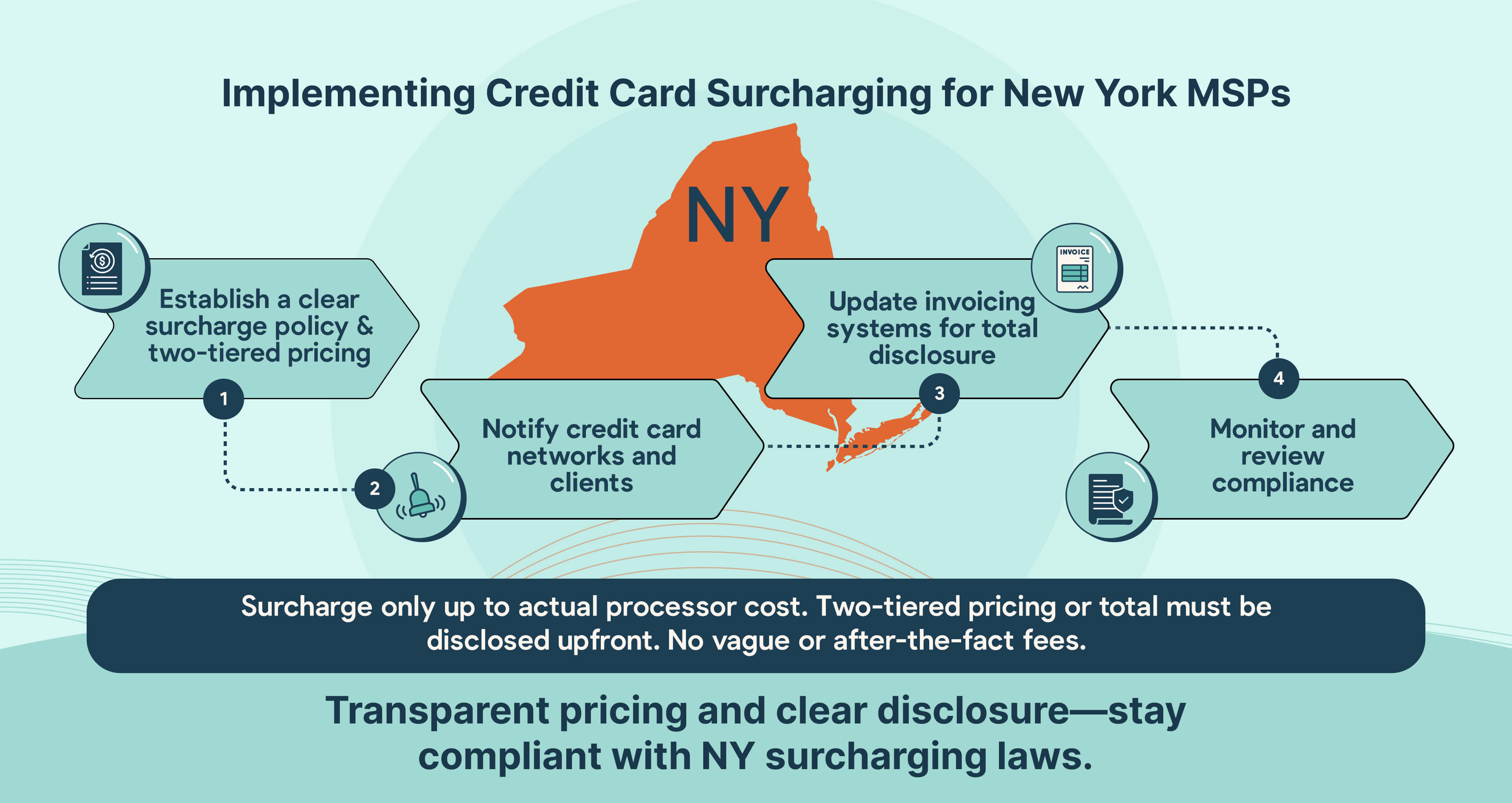

Due to updates under General Business Law § 518, effective February 11, 2024, MSPs now face stricter standards in how and when surcharges are disclosed to clients.

Again, the law permits surcharges only up to the actual amount charged by the payment processor.

In practice, this means no vague “fees may apply” language and no last-minute additions at checkout or on invoices. If the surcharge isn’t clearly disclosed in advance, it’s illegal.

Clients need to know the reason for the fee, the exact amount, and what alternatives exist.

New York consumers now have access to complaint channels through both the Division of Consumer Protection and the Attorney General, making it even more critical for MSPs to get it right the first time.

Here’s how MSPs in New York can build a surcharge strategy that stays within the lines.

Step 1: Establish a Clear Surcharge Policy and Structure

a) Fixed Percentage Model:

If your blended processing cost is 2.95%, and your invoice is $8,600, you may charge a credit card fee of $253.70, for a total of $8,853.70—but only if this total amount is clearly shown before payment is made.

Two-Tiered Pricing Requirement:

Under the law effective February 11, 2024, you must either:

- Display the full credit card-inclusive price before checkout, or

- Display both the cash price and the credit card price side-by-side (known as two-tiered pricing)

General Business Law § 518 defines two-tier pricing as “the tagging or posting of two different prices in which the credit card price, inclusive of any surcharge, is posted alongside the cash price.”

For example:

- Cash/ACH price: $4,950

- Credit Card price (with 2.8% surcharge): $5,088.60

Both options must be posted clearly before the client completes the transaction. Under New York law, simply stating “a 3% surcharge applies” without listing the full total is no longer permitted.

b) Tiered Surcharge Model

Separately, you can also structure your surcharge percentage based on invoice size, as long as each rate accurately reflects your actual processing costs.

For instance:

- 2.5% for invoices under $4,000

- 2.9% for invoices $4,000 and above

If a client’s invoice is $3,600, the surcharge would be $90. If the invoice is $4,400, the surcharge would be $127.60.

Remember: whether you choose a flat rate or tiered surcharge structure, your posted pricing must comply with the two-tier disclosure rules. Never add fees after the fact or describe them vaguely on a receipt.

Step 2: Notify Credit Card Institutions and Clients

MSPs must notify both their payment processor and the major credit card brands about their intention to add a surcharge.

Visa and Mastercard require businesses to provide at least 30 days' advance notice before introducing any credit card surcharges.

This notice requirement typically applies even if your surcharge aligns with your actual processing costs. Many MSPs handle the process through their merchant services provider or submit a direct registration form through the card brands' portals.

Once the networks are informed, your focus should shift to client communication.

Under General Business Law § 518, clients must be informed of the total credit card price before they make a payment. Surprise surcharges are strictly prohibited.

Your communication strategy should include clear disclosures in all relevant client touchpoints, such as:

- Client onboarding materials and welcome packets

- Service contracts and renewal agreements

- Online payment portals and checkout screens

- Itemized invoices and recurring billing notices

Step 3: Update Invoicing Systems

While New York’s updated General Business Law § 518 does not prescribe a specific invoice layout for surcharges, MSPs must still prioritize clear and precise billing practices.

Transparent documentation assures compliance and helps avoid misunderstandings that could lead to disputes under New York’s consumer protection statutes.

The full, credit card-inclusive price must be prominently displayed on the invoice before the client authorizes payment.

If your MSP listed only the base price and added the surcharge quietly later, you would violate New York’s strict disclosure laws.

Software or tools like FlexPoint simplify this by automatically adjusting invoice templates to reflect the total due for credit card transactions. This ensures no manual calculations are missed and that every client sees the accurate final amount ahead of payment.

Step 4: Monitor and Review Compliance

MSPs must actively manage their surcharge practices to stay in compliance with General Business Law § 518 and industry standards.

Staying ahead of compliance and preventing client dissatisfaction means setting up proactive checkpoints:

- Reviewing legal updates from the NYS Division of Consumer Protection

- Monitoring card network bulletins for surcharge policy changes

- Completing annual audits of surcharge practices across all client billing workflows

- Conducting quarterly merchant statement reviews to verify the current effective rates

- Consistently updating client disclosures

An automated, built-in approach using FlexPoint ensures that New York MSPs can maintain compliance efficiently while recovering necessary processing costs, without risking client trust or incurring regulatory fines.

{{ebook-cta}}

The Role of FlexPoint in Streamlining Credit Card Surcharging for New York MSPs

MSPs in New York have a valuable opportunity to offset rising credit card acceptance costs through surcharging, but compliance is mandatory and complex.

That’s where FlexPoint transforms what could be a complicated process into a streamlined, audit-ready system.

Explicitly designed for service-based billing models like MSPs, FlexPoint offers:

- Accurate, automatic application of surcharges to eligible credit card transactions.

- Real-time calculation of fees based on the specific card brand and interchange rate type.

- Transparent display of credit card-inclusive totals on invoices and online payment portals.

- Internal documentation that ties every surcharge directly to the actual processing rate for compliance defense.

FlexPoint also offers various pricing models for MSPs to choose from, depending on whether they opt to implement surcharges.

a) Interchange+ Plan

For MSPs who prefer to absorb processing fees instead of passing them on to clients, FlexPoint’s Interchange+ Plan provides complete visibility into real costs without imposing surcharges.

Instead of a flat fee, each transaction is billed according to the actual interchange rate charged by the processor.

For example:

- A client pays $5,200 using a premium American Express card with a 3.4% interchange rate, resulting in a $176.80 cost to you.

- Another client pays $5,200 via a basic Visa card with a 2.1% interchange rate, resulting in a $109.20 cost.

This plan lets you track every penny spent on interchange fees, even when you don't pass those costs along. With better forecasting, you can bake those expenses into pricing models without violating New York’s strict surcharge rules.

b) Customer Surcharge Plan

FlexPoint’s Customer Surcharge Plan ensures full compliance at every step if you decide to pass on the entire processing fee.

Suppose you issue a service invoice for $6,900, and your processing rate is 2.7%.

FlexPoint will apply a surcharge of $186.30, bringing the total credit card price to $7,086.30—clearly shown to the client before payment.

Key protections built into the system include:

- Blocking surcharges on debit and prepaid cards automatically, which remain non-surchargable under federal rules.

- Embedding compliant disclosures on invoices, online portals, and mobile payment links.

- Storing detailed surcharge calculation records to prove that the applied fee matches the processor’s actual charges.

Given New York’s heightened emphasis on fee transparency, if no alternative, fee-free method (such as ACH or check) is offered, surcharges must be included in the advertised price rather than presented separately. FlexPoint’s dual pricing configuration prevents accidental violations by requiring fee-free options before applying a surcharge.

Not every New York MSP wants to pass the entire burden of credit card processing fees onto clients.

Sometimes, maintaining strong client relationships or staying price-competitive means absorbing part of the fee yourself while still recovering a portion of it.

FlexPoint supports this flexibility by allowing MSPs to split the processing cost between their business and their clients while remaining fully compliant with General Business Law § 518.

How FlexPoint Enhances Surcharging Compliance and Transparency

Since February 11, 2024, New York law, as outlined in GBL § 518, permits surcharges only if specific disclosure and pricing rules are met. As of [$c-month-year]April 2025[$c-month-year], these laws remain in effect.

Failure to post the full credit card price before checkout or charging more than the actual processing cost risks enforcement under deceptive trade statutes.

FlexPoint automates surcharge compliance by:

- Generating invoices that display both the subtotal and the total, including the total paid by credit card.

- Calculating surcharges dynamically based on card type and transaction amount.

- Automatically omitting surcharges when clients pay by ACH, check, or debit.

- Retaining audit-ready records that validate your surcharge practices aligns with New York's strict legal requirements.

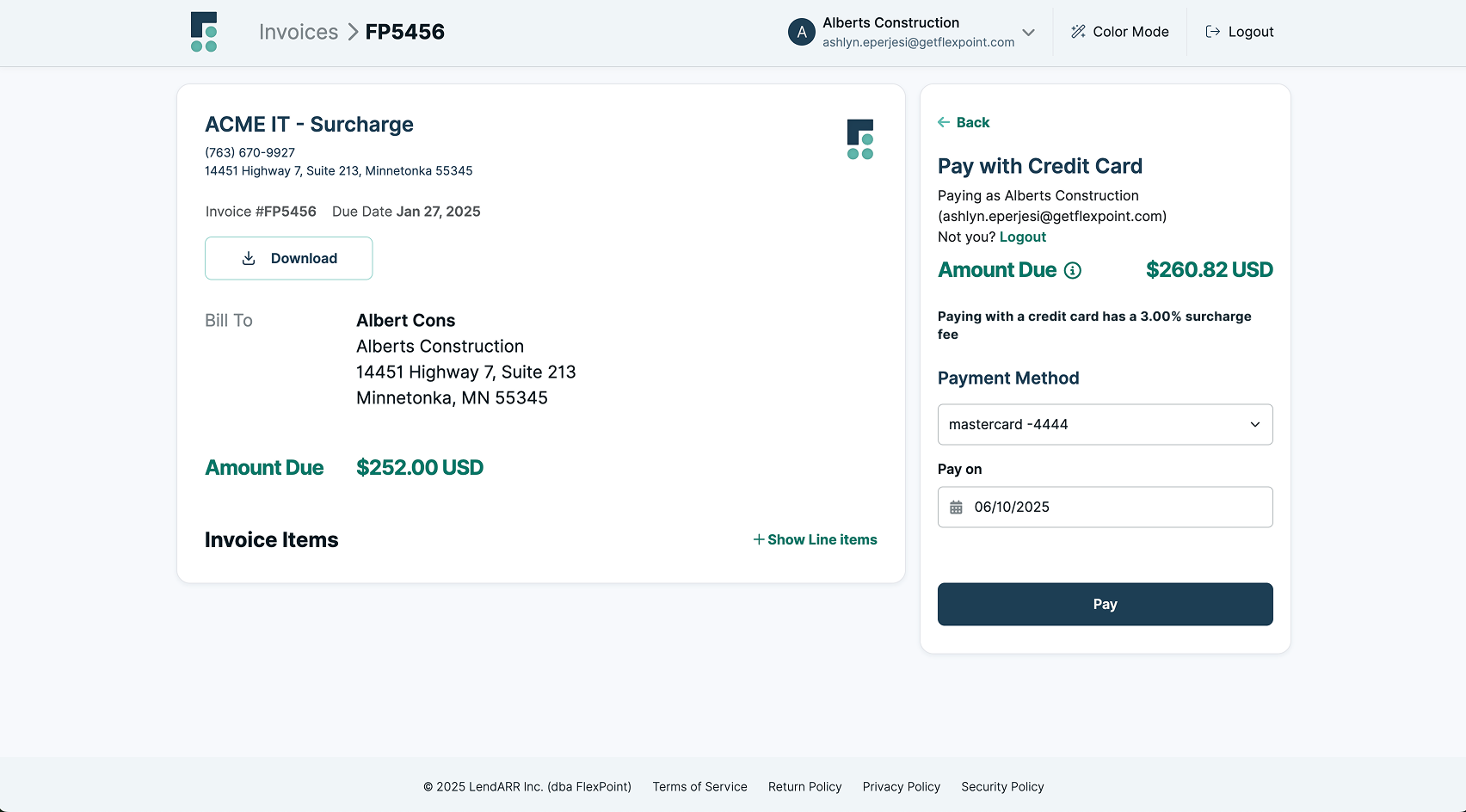

Here’s how a compliant invoice might appear:

Notes

Thank you for your ongoing business. For any billing questions, contact [Your Contact Information].

FlexPoint’s Integration with MSP Tools for Seamless Billing

Billing challenges multiply when invoicing, payment collection, and reconciliation happen across disconnected systems.

FlexPoint closes that gap by integrating directly with:

When a client pays $8,300 via credit card, FlexPoint automatically applies a 2.5% surcharge (for example), adjusts the total, updates the accounting ledger, and posts the payment in real time without any manual entry.

This real-time synchronization minimizes reconciliation errors and ensures financial reports always reflect the actual revenue collected, including surcharge recovery.

On the client side, FlexPoint provides a secure, branded payment portal where clients can:

- See service breakdowns, surcharges, and total due.

- Select fee-free ACH payment options.

- Understand the impact of choosing credit versus ACH immediately during checkout.

For instance, when a client sees a $7,000 invoice showing a $175 card surcharge, they know exactly what they are paying and can opt for ACH if they prefer.

{{client-portal-gif}}

Offering Flexibility in Surcharging

{{admin-portal-gif}}

With FlexPoint, New York MSPs have fine-tuned control over how surcharges are applied:

- Customize by client: Offer full surcharges to some clients and partial or waived surcharges for strategic accounts.

- Share the cost: Paying only part of the processing fee to clients.

- Enforce dual pricing: Set credit card-inclusive prices while offering cash or ACH discounts that are legally compliant.

Example:

- A long-time enterprise client paying $12,500 monthly might have the 2.5% surcharge ($312.50) fully absorbed as a loyalty incentive.

- A newer client invoiced $4,300 monthly might see a 2.8% surcharge ($120.40) to cover processing costs transparently.

FlexPoint lets you control surcharge percentages per client while staying fully aligned with New York’s legal requirements.

Alternative Cost-Effective Payment Method - ACH for New York MSPs

While credit cards offer clients convenience, they bring significant costs for MSPs operating in New York, especially when factoring in processing fees and strict surcharge compliance rules under General Business Law § 518.

ACH (Automated Clearing House) payments offer a highly effective alternative for MSPs seeking to streamline billing and minimize overhead.

Instead of juggling different surcharge caps by card brand, such as 3% for Visa and 4% for Mastercard, and monitoring evolving surcharge disclosure regulations, ACH payments offer a flat, predictable payment method with fewer complications.

Typically, ACH transfer fees range between $0.25 and $1.00 per transaction, regardless of the invoice total, whether $600 or $20,000.

There are no interchange categories to track, no brand-by-brand rate differences, and no risk of misapplying a surcharge to a debit or prepaid card, which are prohibited from surcharging under New York law and card network policies.

For example, instead of calculating whether a 2.7% surcharge on a $8,500 invoice ($229.50) might upset a client or trigger a compliance issue, ACH simply removes that risk altogether.

When a client pays via bank transfer, the amount owed remains straightforward, without any added fees or hidden charges. Clients appreciate the simplicity—and so does your accounting team.

FlexPoint makes it easy for New York MSPs to encourage ACH adoption:

- Same-Day ACH capabilities allow payments to clear in the same business day (when submitted before 4 pm ET), rather than waiting the traditional 3–5 business days associated with standard bank transfers.

- Real-time reconciliation features mean once a payment is received, FlexPoint instantly updates the client's account, eliminating the need for manual ledger adjustments or tedious cross-system verifications.

Beyond speed and simplicity, ACH payments offer several operational advantages, including lower chargeback rates, reduced transaction failure rates, and streamlined financial record-keeping.

Encouraging ACH payments not only lowers transaction costs but also supports a transparent billing process that aligns perfectly with New York's heightened expectations for disclosure and fee transparency.

With FlexPoint, New York MSPs can easily make ACH a preferred payment option, safeguarding margins while delivering a better billing experience for their clients.

Conclusion: Reduce Processing Costs AND Maintain Compliance for New York MSPs with Credit Card Surcharging

Under General Business Law § 518, New York credit card surcharges are only lawful when they meet specific conditions:

- They must be clearly disclosed upfront, giving the client full visibility into the total credit card price before completing the transaction.

- They must be directly tied to your actual processing costs, not based on rounded numbers or general estimates.

- They must be presented transparently on invoices, payment screens, and service agreements, avoiding vague descriptions or after-the-fact additions.

Failing to fulfill any of these obligations risks more than just client dissatisfaction.

Under New York's consumer protection laws, violations can be classified as deceptive trade practices, exposing MSPs to civil penalties up to $500 per violation and potential refund obligations for affected clients.

Additionally, card brands impose their own surcharge rules, including maximum allowable percentages and a requirement for advance registration.

Non-compliance with card brand policies can result in steep fines, higher processing costs, or even loss of merchant processing privileges.

With these overlapping legal and network requirements, managing surcharges manually becomes both risky and time-consuming.

That’s why a growing number of New York MSPs turn to FlexPoint—a purpose-built solution that automates surcharge calculations.

Enhance your MSP’s financial operations with FlexPoint’s automated surcharging and ACH solutions.

Stay compliant with New York’s regulations and maximize your profitability today.

Schedule a demo to learn more about FlexPoint’s payment solutions.

{{demo-cta}}

Additional FAQs: Credit Card Surcharging in New York for MSPs

{{faq-section}}