In Minnesota, credit card surcharging has been an option for managed service providers (MSPs) for decades; however, recent regulatory updates have altered how this fee must be presented to clients. For MSPs, this means understanding both long-standing and new disclosure requirements to stay compliant.

As of [$c-month-year]January 2025[$c-month-year], MSPs in Minnesota may continue to pass on credit card processing costs to clients, but the process is now subject to more precise rules.

Minnesota's statutes now explicitly authorize enforcement under the Deceptive Trade Practices Act, allowing civil fines and potential action from state regulators. In practical terms, MSPs must treat surcharge transparency as a core part of their billing process, not an afterthought.

Any surcharge must be tied exclusively to credit card use, remain within cost-based thresholds, and be communicated in a way that leaves no room for misunderstanding.

Even minor lapses in compliance, such as failing to provide verbal notice or including a fee on debit card transactions, can create legal exposure.

This guide outlines the requirements that Minnesota-based managed service providers must meet to legally impose credit card surcharges. It also examines how automation platforms—especially those specifically designed for MSP billing—standardize compliance by streamlining invoicing, applying rules consistently, and maintaining audit-ready documentation.

Disclaimer: This article is for informational use only and does not constitute legal advice. Minnesota MSPs should refer to the most recent version of Minn. Stat. § 325G.051 and related statutes, consult qualified legal counsel, and regularly review internal billing procedures to ensure surcharge practices align with state law.

What is Credit Card Surcharging for MSPs in Minnesota?

Credit card processors and payment gateways typically charge a 2% to 4% fee for each credit card transaction. These fees erode profits for MSPs billing thousands of dollars per client or those with high-volume recurring payments.

Credit card surcharging shifts that processing cost to the client. Under Minnesota law, and assuming card brand (Visa, Mastercard, American Express) rules are followed, a surcharge can be added to credit card payments as long as it’s clearly disclosed and tied directly to the cost of acceptance.

Here’s how that might play out for a Minnesota-based MSP:

Suppose your MSP processes $120,000 in monthly credit card payments for services. With a 2.5% processing fee, you’d be paying $3,000 each month to your payment processor. By applying a full 2.5% surcharge, you recover the entire $3,000, allowing your MSP to retain the full $120,000 in revenue instead of absorbing that cost.

Multiply that over a year, and you’re looking at $36,000 in savings; these funds you can reinvest into operations, client services, or growth initiatives.

If you prefer to share the cost with clients, you could apply a partial surcharge of 1.25%. In this case, you would recover $1,500 per month, or $18,000 annually—still a significant offset to your expenses while shouldering part of the fee yourself.

In a margin-sensitive business like managed IT services, surcharging provides a way to protect profitability without silently losing thousands to processing costs.

When implemented correctly—with updated signage, checkout disclosures, and automated invoicing systems that document the surcharge—you can keep your billing compliant, transparent, and client-friendly.

{{cal-one}}

Understanding Credit Card Surcharging Laws in Minnesota

For MSPs in Minnesota, the rules around credit card surcharges have always required close attention.

Under Minn. Stat. § 325G.051, MSPs are still technically permitted to add a surcharge of up to 5% on credit card payments. However, Visa currently caps surcharges at 3%, and Mastercard allows up to 4%, with both card brands requiring the surcharge not to exceed the actual processing cost.

{{debit-cta}}

Although the state statute permits a higher percentage, the lowest applicable limit effectively sets the maximum surcharge that MSPs can apply.

More importantly, the amount you charge can never exceed your actual cost to process the transaction, regardless of the 5% state cap or the 4% federal ceiling.

If your credit card processing rate is 2.6% (for example), that’s the most you’re allowed to pass on. Anything above that may be considered deceptive or unlawful under Minnesota’s consumer protection laws.

Minn. Stat. § 325G.051 also requires in-person transactions to include both verbal notification and posted signage, while online and phone-based payments must include clear notice on checkout pages or during the call before the card is processed.

A longstanding prohibition on surcharging debit cards or store-branded credit programs also remains in place. Under the Dodd-Frank Act, even if a debit card is run as “credit,” it cannot legally be surcharged. Card brand networks also enforce this rule, and violations can result in fines or loss of processing privileges.

With new legislation now in effect, the rules have become even more restrictive.

Minnesota Surcharging Changes Effective January 2025

As of [$c-month-year]January 1, 2025[$c-month-year], a new law—HF 3438, enacted in May 2024—has redefined how Minnesota regulates pricing transparency and surcharges.

This law amended Minn. Stat. § 325D.44, expanding the definition of a deceptive trade practice to include any instance where a business displays a price that doesn’t include all mandatory fees or surcharges.

Accordingly, a surcharge may be considered a mandatory fee if:

- The customer must pay it to complete the transaction.

- The fee is not reasonably avoidable.

- Or a typical consumer would expect it to be included in the advertised price.

This change doesn’t repeal the older surcharge permission statute (§ 325G.051) but significantly narrows how surcharges can be presented.

In practice, if your client can’t avoid the credit card fee (because you don’t accept any non-surcharged alternatives), then you can no longer add it as a separate line item. Instead, it must be built into the listed price of your services.

For many MSPs—especially those that primarily bill online or don’t offer ACH or check alternatives—this effectively bans separately added surcharges.

If credit cards are your only payment option, you must now advertise the full amount, including the surcharge, upfront.

For example, listing $3,500 and adding a separate $105 surcharge fee at checkout could violate Minnesota’s deceptive trade laws.

If you can’t meet the new visibility and optionality standards, continuing to add a separate credit card fee could put your MSP at risk of fines or public complaints.

Under 325G.051, any seller who violates this section is subject to a civil penalty of not more than $500 and must refund the surcharge to each buyer. To avoid breaking the law, review your billing systems now and consult with legal counsel if needed.

If you’re unsure whether your surcharge approach complies with Minnesota’s updated statutes or whether your processing fees justify the amount you’re charging, consult legal counsel before moving forward.

{{usa-cta}}

Implementing Credit Card Surcharging for Minnesota MSPs

For Minnesota MSPs, passing on credit card processing fees may seem like a practical business decision, but it must be handled with care.

While the ability to surcharge remains technically available under Minn. Stat. § 325G.051, implementing it without complete transparency can strain client relationships or create compliance risks under updated consumer protection laws.

The success of any surcharge strategy starts with clarity and precision. Clients should know why the fee exists, exactly how much they’re being charged, and when it applies.

Charging too much—even slightly above your actual processing rate—could result in regulatory violations.

Charging too little means you're still absorbing a portion of the cost.

The goal is to cover your actual expenses without exceeding legal thresholds or compromising client trust.

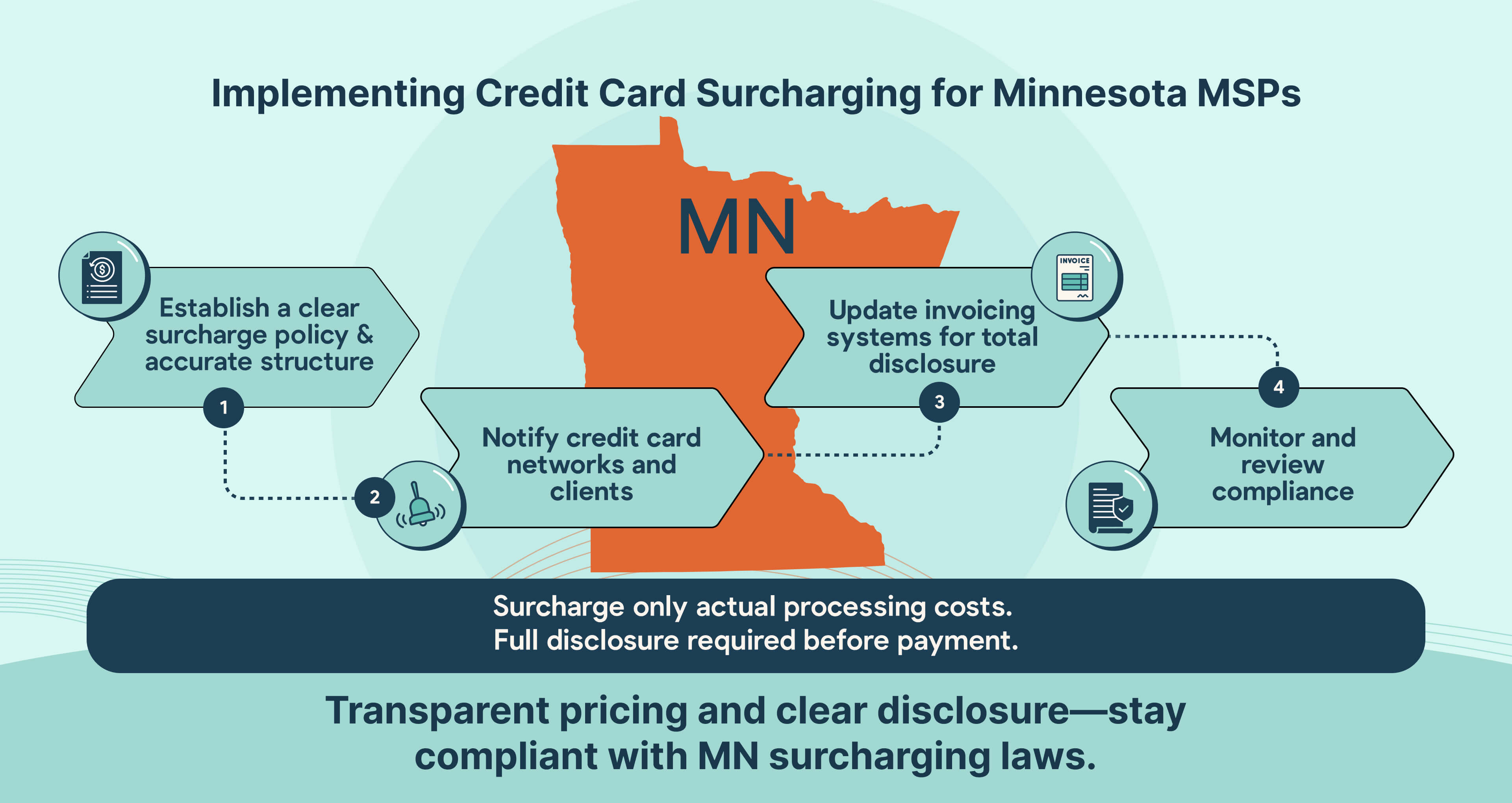

Here are four practical steps Minnesota MSPs can follow to apply surcharges in a way that’s both compliant and client-friendly.

Step 1: Establish a Clear Surcharge Policy and Structure

Before you charge anything, develop a written policy that outlines:

- Which types of transactions are subject to the surcharge

- How the surcharge is calculated (flat percentage or tiered model)

- What steps your MSP is taking to remain compliant with Minnesota statutes, card network rules, and federal regulations like the Durbin Amendment

You can structure your surcharge in one of two ways:

a) Fixed Percentage Model

You apply the same percentage fee to all credit card transactions.

Example: You charge 2.85% across the board. If your invoice is $7,400, the surcharge would be $210.90, bringing the total to $7,610.90.

b) Tiered Surcharge Model

The surcharge increases in proportion to the invoice amount.

Example:

- 2% for invoices under $3,500

- 3% for invoices $3,500 and above

If a client receives a $3,200 invoice, they pay a $64 fee. The fee for a $5,100 invoice would be $153.

Whatever method you choose must reflect your actual average card processing cost.

Rounding up or padding the fee, no matter how small, violates both card network rules and Minnesota’s Deceptive Trade Practices standards.

Don’t rely on vague language like “a surcharge may apply.” You must disclose the exact percentage or dollar amount before payment is processed.

Step 2: Notify Credit Card Institutions and Clients

Before launching a surcharge policy, you must notify the card networks and your payment processor.

Both Visa and Mastercard require at least 30 days’ notice before implementation. This can often be done through your gateway provider or directly via the networks' compliance portals.

Next comes your client communication strategy. Surprise fees, even small ones, can create friction or trigger a payment dispute. Be proactive and clear.

Include surcharge details in:

- Client onboarding documents

- Payment instructions or checkout portals

- Service agreements and renewal contracts

- Itemized invoices and recurring billing statements

For example, if you send a client an invoice for $8,100 and quietly tack on a 3% fee ($243), they may push back or request a chargeback.

According to Swipesum, the average chargeback costs a business around $190 in fees, penalties, and lost time. Proper disclosure prevents this outcome.

Step 3: Update Invoicing Systems

Even though Minnesota doesn’t require a surcharge-specific invoice format, clear and accurate billing helps meet obligations under § 325G.051. It ensures you remain in good standing under the state’s broader consumer fraud laws.

Here’s how your invoice might look:

- Managed IT Services: $6,950

- Credit Card Surcharge (2.7%): $187.65

- Total Due: $7,137.65

Step 4: Monitor and Review Compliance

Maintaining compliance isn’t a one-and-done task. As laws shift and card brand rules update, your surcharge policy must evolve too.

To stay compliant and avoid penalties:

- Review your merchant statements quarterly

- Adjust your surcharge rate if your processing costs change

- Keep all disclosures up to date in agreements, invoices, and online systems

- Continue excluding debit and prepaid cards from surcharges under both card brand policies and the Dodd-Frank Act

Remember how Minnesota’s price transparency laws, now in effect under the revised § 325D.44, may impact your surcharge disclosures.

If your MSP does not offer a viable, fee-free payment alternative, like ACH, check, or cash, your credit card surcharge may be treated as a mandatory fee. In that case, it must be included in the advertised price of your service, not added at checkout or invoicing.

{{ebook-cta}}

The Role of FlexPoint in Streamlining Credit Card Surcharging for Minnesota MSPs

As discussed above, MSPs in Minnesota can use credit card surcharging to offset the rising costs of credit card acceptance, but it comes with conditions.

To stay compliant, the fee must apply only to credit card payments, match your actual transaction cost, and be clearly communicated before the client pays.

Anything less puts your MSP at risk of breaching Minnesota’s consumer protection laws or violating card brand agreements.

FlexPoint, an MSP Payment Automation Platform, makes it simple to meet these requirements while removing manual guesswork.

Its payment automation tools are built specifically for service-based billing environments and offer:

- Precise application of surcharges to eligible credit card payments

- Dynamic calculation based on card brand and rate type

- Automatic itemization on client invoices

- Internal documentation that shows surcharge rates match actual processing fees

You also have flexibility in how you choose to handle processing costs:

a) Interchange+ Plan

If you prefer not to pass fees on to your clients, FlexPoint’s Interchange+ Plan helps you track and absorb those charges internally while still gaining valuable insight.

Each transaction is billed based on the actual interchange rate charged by the card provider, rather than a flat processing percentage.

For example:

- A client pays $3,800 using a premium Mastercard with a 2.4% interchange rate, so your processing cost is $91.20

- Another client uses a basic Visa card with a 1.7% interchange rate to pay the same amount, costing you $64.60

This plan provides you with complete visibility into the cost per transaction, making it easier to budget, even if you choose to absorb all fees as part of your pricing model.

b) Customer Surcharge Plan

If you decide to recoup those costs from your clients, FlexPoint’s Customer Surcharge Plan gives you a built-in, rule-based way to do so.

Suppose you invoice a client $7,250, and your processor charges an average of 2.65%. FlexPoint will apply a surcharge of $192.13, bringing the total to $7,442.13. The client sees the fee clearly separated on the invoice, and you retain the full $7,250 in revenue, without any ambiguity.

The system also prevents common compliance issues:

- Surcharges are blocked on debit and prepaid cards, which remain non-surchargable under federal rules and card brand policies

- Disclosures are generated automatically and formatted for invoices, online checkout, and mobile interactions

- All records are stored to demonstrate that your surcharge equals (or is less than) your actual cost

Minnesota’s updated consumer protection framework requires that if a surcharge is mandatory (i.e., not avoidable), it must be included in the advertised price. FlexPoint supports this interpretation by allowing you to configure surcharges only when a fee-free payment method is available, keeping you in line with the latest rules under § 325D.44.

Not every MSP wants to pass 100% of the processing cost to clients, and FlexPoint also supports this choice. You can choose to share the fee between your business and the client.

Suppose your average card fee is 2.8%. You decide to pass 1.2% to the client and absorb the remaining 1.6% yourself.

On a $6,400 invoice, the client pays a surcharge of $76.80, and your MSP covers $102.40. This approach softens the impact on the client while still recovering a meaningful portion of your expenses.

How FlexPoint Enhances Surcharging Compliance and Transparency

As of [$c-month-year]May 2025[$c-month-year], Minnesota law permits MSPs to apply surcharges when several rules are closely followed.

Under § 325G.051, surcharges are allowed only when tied directly to credit card use, and § 325D.44 clarifies that how you communicate these fees matters as much as the amount. Any fee must be clearly disclosed before the transaction and must not exceed the actual charges from your payment processor.

If a surcharge appears as a surprise on an invoice or if you charge more than your real cost to process the card, you may be entering deceptive trade territory. This can trigger enforcement under Minnesota’s consumer protection statutes, where each violation may be subject to a civil penalty and a refund requirement.

Fortunately, FlexPoint integrates surcharge compliance into your entire billing process—automatically, accurately, and without guesswork.

FlexPoint’s surcharge automation system is designed for professional service businesses like MSPs, and it does more than calculate percentages.

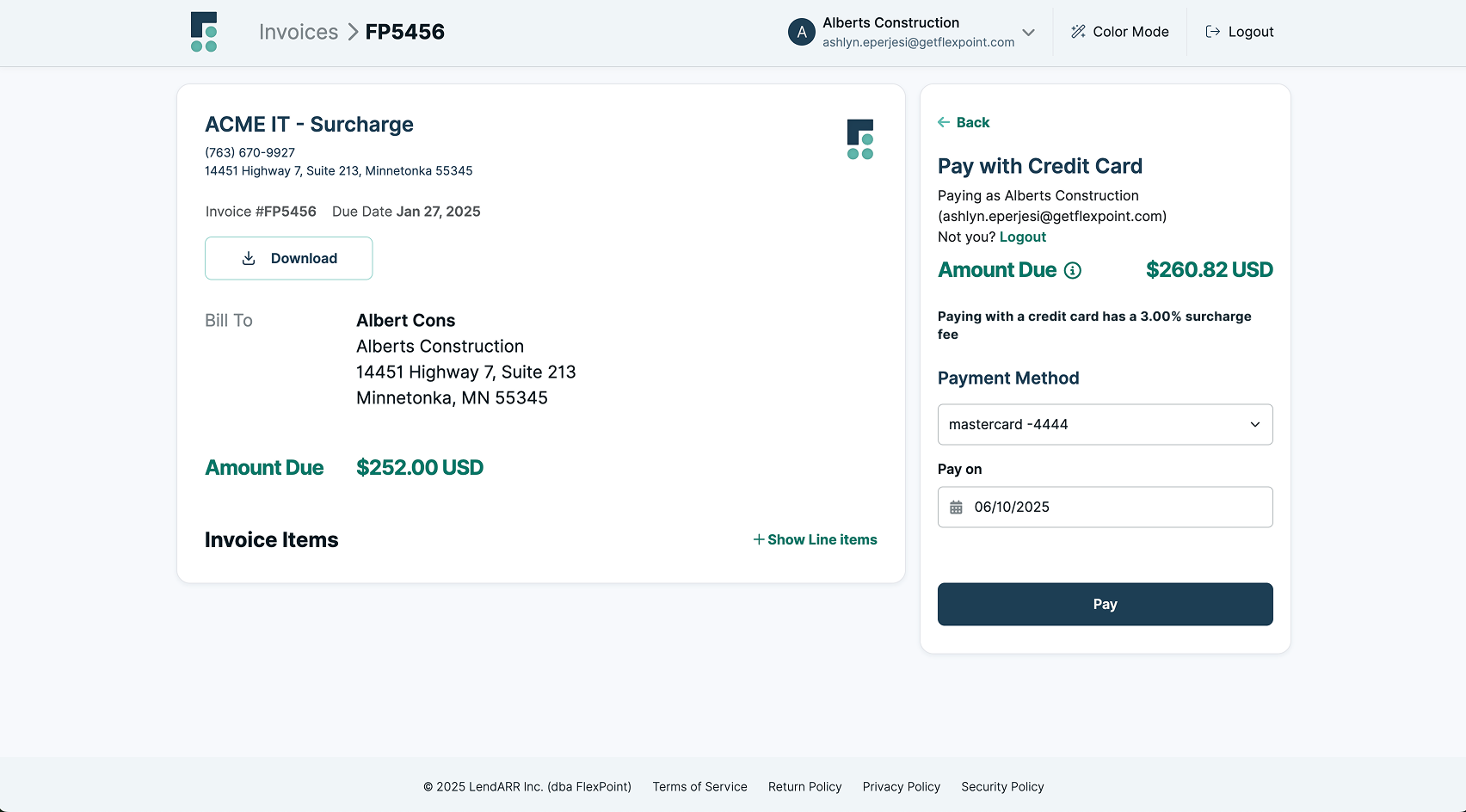

Here’s how a Minnesota-compliant invoice generated through FlexPoint might appear:

FlexPoint’s Integration with MSP Tools for Seamless Billing

When invoicing, accounting, and payment tracking are handled by separate software platforms, even simple billing tasks can become slow, error-prone, and compliance-challenged for MSPs.

FlexPoint was designed to close that gap.

It integrates directly with the financial and PSA tools Minnesota MSPs already use every day, including:

Once connected, FlexPoint acts as a unified billing engine. It syncs invoices, records payments, tracks credit card surcharges, and eliminates the need to re-enter the same data in multiple places. That means fewer reconciliation delays, no mismatched numbers across platforms, and far less time spent fixing preventable billing errors.

Suppose your average card processing rate is 2.5%, and you invoice a client $6,400. FlexPoint applies the $160 surcharge, ties it directly to the credit card payment, and automatically reflects that fee on both the client’s invoice and your accounting ledger, without requiring any manual edits.

FlexPoint also improves the way your clients interact with your billing system.

Minnesota MSPs using FlexPoint can offer clients a branded, secure portal where they can:

- View detailed invoices that break down services and fees

- Select from ACH or credit card payment methods

- Clearly see any surcharge listed separately from service charges

This level of visibility helps clients feel informed and respected. It also reinforces legal compliance, since Minnesota law requires clear and timely disclosure of any credit card surcharge under § 325G.051.

When clients log in and see that a $6,400 invoice includes a $160 fee (at 2.5%), they know exactly what they’re paying—and why.

It also reduces billing disputes and the risk of chargebacks. With a record of what was shown to the client, when it was shown, and how the surcharge was calculated, your team is never left scrambling to justify a fee after the fact.

{{client-portal-gif}}

Offering Flexibility in Surcharging

{{admin-portal-gif}}

With FlexPoint, MSPs in Minnesota can decide exactly how and when credit card surcharges apply on a client-by-client basis. This gives you the flexibility to adjust your fee approach according to factors such as contract size, service tier, or the depth of your working relationship.

Rather than using a single rule for every invoice, FlexPoint allows you to be intentional, waiving the surcharge for certain accounts while applying it in full for others.

Let’s say you have a long-time client who pays $10,800 per month for enterprise-level support. They’ve been with your MSP for years, and your margins are healthy. You might choose to cover the 2.4% card fee of $259.20 as a courtesy or loyalty benefit.

Now, take a new client who is billing at $3,400 per month. In that case, you might decide to apply a 2.6%surcharge—$88.40—to offset processing costs while onboarding.

FlexPoint makes these decisions easy to implement. With just a few clicks, you can enable or disable surcharging for individual clients, set custom percentages based on actual card processing costs, and ensure every charge complies with Minnesota’s current statutes and disclosure standards.

That level of control matters in Minnesota, where the law now emphasizes both fee accuracy and upfront visibility. If your surcharge isn’t disclosed clearly before payment or exceeds your actual cost, you could be in violation of § 325D.44—even if the amount seems minor.

FlexPoint helps you avoid that risk while building a surcharge policy that reflects your business priorities and supports long-term client satisfaction.

Alternative Cost-Effective Payment Method - ACH for Minnesota MSPs

Relying on credit cards to get paid is often convenient, but it’s also expensive. ACH payments are a practical option for Minnesota-based MSPs hoping to avoid the complexity of surcharge rules and the cost of card processing.

Instead of managing various surcharge percentages, card type restrictions, and evolving compliance rules, ACH provides a flat, predictable model.

ACH transfers cost between $0.25 and $1.00 per transaction, regardless of whether the invoice is $500 or $15,000. There are no card network thresholds to track, no brand-specific rules to follow, and no risk of applying a surcharge to a non-eligible card by mistake.

For service providers tired of calculating whether a 2.4% surcharge on a $9,100 invoice will trigger a potential client complaint—or a state violation—ACH payments remove that layer of risk entirely.

When clients pay via ACH transfer, they know exactly what to expect. There’s no added fee tacked on at checkout, no pricing ambiguity, and no risk of a client delaying payment to avoid what they perceive as an extra charge.

FlexPoint makes it easy to transition to ACH payments without adding more work for your team. The platform supports Same-Day ACH, allowing many transactions to clear in hours rather than days. This helps MSPs maintain cash flow without waiting through the traditional 3–5 day bank cycle.

ACH payments also have fewer chargebacks, lower payment failure rates, and less back-office cleanup.

Because FlexPoint automatically reconciles payments and updates your records in real time, you don’t need to switch between systems to verify incoming funds or update client balances manually.

Conclusion: Reduce Processing Costs AND Maintain Compliance for Minnesota MSPs with Credit Card Surcharging

MSPs can’t simply add a fee at checkout and call it compliant.

Under Minnesota law, a surcharge is only permitted if it’s:

- Disclosed upfront, before the client completes the transaction

- Tied directly to your actual processing cost, not a rounded or estimated rate

- Presented clearly on invoices, statements, or online checkouts in a way that leaves no ambiguity

Ignoring these requirements frustrates clients and harms your relationship with them. In addition, it may be treated as a deceptive trade practice under Minn. Stat. § 325D.44, with possible penalties and refund obligations for each violation.

At the same time, card brands require merchants to follow their own surcharge policies, including fee limits and notice protocols.

With all these layers in play, compliance can get complicated quickly. That’s why many Minnesota MSPs use FlexPoint to handle surcharge automation, keep disclosures consistent, and ensure every fee applied is fully compliant from start to finish.

Enhance your MSP’s bottom line and compliance with automated credit card surcharging solutions from FlexPoint.

Stay within Minnesota’s regulations and simplify your payment processes today.

{{demo-cta}}

Additional FAQs: Credit Card Surcharging in Minnesota for MSPs

{{faq-section}}