Since early 2013, Illinois has permitted businesses to apply surcharges on credit card payments, but this permission comes with detailed compliance expectations. The state’s position on surcharges has remained steady.

As of [$c-month-year]April 2025[$c-month-year], businesses, including MSPs, may charge clients extra for using credit cards, but only if the fee is disclosed correctly, fairly calculated, and strictly limited to credit card transactions.

Failing to follow these rules poses reputational risk and can trigger enforcement under Illinois’s Consumer Fraud and Deceptive Business Practices Act, which authorizes financial penalties and civil action for violations.

For managed service providers operating in Illinois, the line between a compliant surcharge and an illegal fee depends on several key elements: visible signage, truthful pricing communication, and the correct application of fee limits.

Missteps in any of these areas can lead to client disputes or action from the Illinois Attorney General.

This guide discusses the current rules Illinois MSPs must follow when applying credit card surcharges. It also outlines how payment automation tools can simplify surcharge compliance by automating billing tasks, managing documentation, and facilitating client communication.

Disclaimer: This material is provided for general informational purposes only and does not constitute legal advice. Illinois MSPs should review the latest guidance, assess their internal billing practices, and consult with legal counsel before implementing surcharges.

What is Credit Card Surcharging for MSPs in Illinois?

Credit card surcharging offers Illinois MSPs a practical way to offset the transaction fees that reduce profits, particularly when clients pay sizable invoices or use premium credit cards with elevated interchange rates.

Each credit card payment carries a cost, and those expenses accumulate quickly for MSPs managing recurring billing cycles or long-term IT retainers.

Surcharging allows you to shift part or all of that cost back to the client, provided the surcharge is fully disclosed and in line with Illinois consumer protection requirements.

Applying a surcharge means adding a small percentage-based fee to a credit card invoice when the client opts to pay that way. The fee reflects your own processing costs and is legally permitted under current Illinois law when applied correctly.

Here’s how it might look for an MSP operating in Illinois:

Suppose your MSP processes $85,000 in monthly credit card payments for managed cybersecurity services. With a 3% processing fee, you’d pay $2,550 each month to your payment processor. By applying a full 3% surcharge, you recover that entire $2,550, allowing you to keep the full $85,000 in revenue while the client covers the cost for the convenience of using a credit card.

Repeat that across the year, and the savings become significant—$2,550 per month adds up to $30,600 annually that stays in your business instead of going to payment processors.

If you prefer to share the cost, you could apply a partial surcharge of 1.5% instead. This would recover $1,275 per month, or $15,300 annually. This is still a meaningful reduction in processing costs while absorbing part of the expense yourself.

Whether you choose to pass on the full cost or just a portion, surcharging gives you room to protect your margins while remaining compliant with Illinois state law and card brand requirements.

{{cal-one}}

Understanding Credit Card Surcharging Laws in Illinois

For MSPs operating in Illinois, even a relatively modest surcharge—just a few percentage points—can make a noticeable difference in profitability, especially when clients use premium credit cards linked to rewards programs or corporate accounts.

These card types typically generate processing fees ranging from 2 to 4%, and when applied across monthly billing cycles, those charges can add up.

While no statute specifically outlines surcharge rules in percentage terms, Illinois relies on its Consumer Fraud and Deceptive Business Practices Act (815 ILCS 505) to establish boundaries.

Under this law, you can only impose a surcharge on a credit card payment if that fee reflects your actual processing cost. Charging more than your provider charges may be considered deceptive, even if it's unintentional.

It’s also important to recognize where surcharges are explicitly off-limits.

Illinois follows card brand agreements and federal rules, including the Durbin Amendment, which is part of the broader Dodd-Frank Act. This amendment regulates how debit card fees are handled and makes it clear that merchants may not add surcharges to debit card transactions, regardless of whether the card is processed through the system with or without a PIN.

{{debit-cta}}

If the payment is deducted from a bank account, it is classified as a debit. Debit surcharges are strictly prohibited.

The takeaway for MSPs is simple: surcharging is legally allowed in Illinois, but only if applied correctly.

Failing to follow relevant rules can create payment friction with clients but also opens the door to legal trouble. Under Illinois law, penalties for violating consumer fraud protections can reach up to $50,000 per instance, especially if there is evidence of willful misconduct or repeat violations.

Illinois law is structured in a way that allows MSPs to recover processing fees transparently, as long as clients are given notice and the amount falls within what they are actually paying to their merchant processor or payment gateway. In other words, the surcharge must reflect cost, not profit.

While the legal environment for surcharging is currently favorable in Illinois, there are signs of possible regulatory changes on the horizon.

In 2024 Illinois lawmakers introduced the “Junk Fee Ban Act” (HB 4629 / SB 3331). This bill would make it unlawful for businesses to display or advertise a price without also clearly showing the total amount a consumer may be required to pay.

The total price must be displayed more prominently than any other price-related detail, effectively curbing practices where surcharges are only disclosed at checkout.

Although this bill has not yet passed (as of [$c-month-year]April 2025[$c-month-year]), it reflects growing interest in fee transparency and could affect how surcharge details are presented in marketing materials and proposals.

Separately, a new Illinois law, known as the Interchange Fee Prohibition Act, was passed in 2024 and is set to take effect on July 1, 2025. This law prohibits payment processors and card brands from charging interchange fees on sales tax or gratuity portions of a credit or debit card transaction.

While this legislation doesn't directly limit your ability to surcharge clients, it could indirectly affect the structure of card processing fees and how your processor calculates your rates.

Illinois legislators have considered limits in the past, most notably in 2021, when House Bill 3128 proposed capping surcharges at 1%—but that bill never became law. Currently, there are no active measures targeting surcharge practices.

Still, MSPs should remain alert, as future legislation could tighten rules or redefine how service providers must handle disclosures and fee thresholds.

If you’re unsure whether your surcharge policy aligns with current requirements or how much you’re actually paying in card processing fees, seek legal guidance.

{{usa-cta}}

Implementing Credit Card Surcharging for Illinois MSPs

While recouping credit card processing fees may seem like a straightforward financial decision, introducing and managing surcharges can affect client trust, retention, and even your legal standing.

The foundation of a successful surcharge strategy is clarity. Clients should understand the reason for the charge, the exact amount, and when it applies.

Overcharging can drive clients away, even if it’s by a fraction of a percent. Undercharging, on the other hand, leaves you covering more of the cost than necessary.

The goal is to strike a balance: recover your actual expense without creating confusion or tension in the relationship.

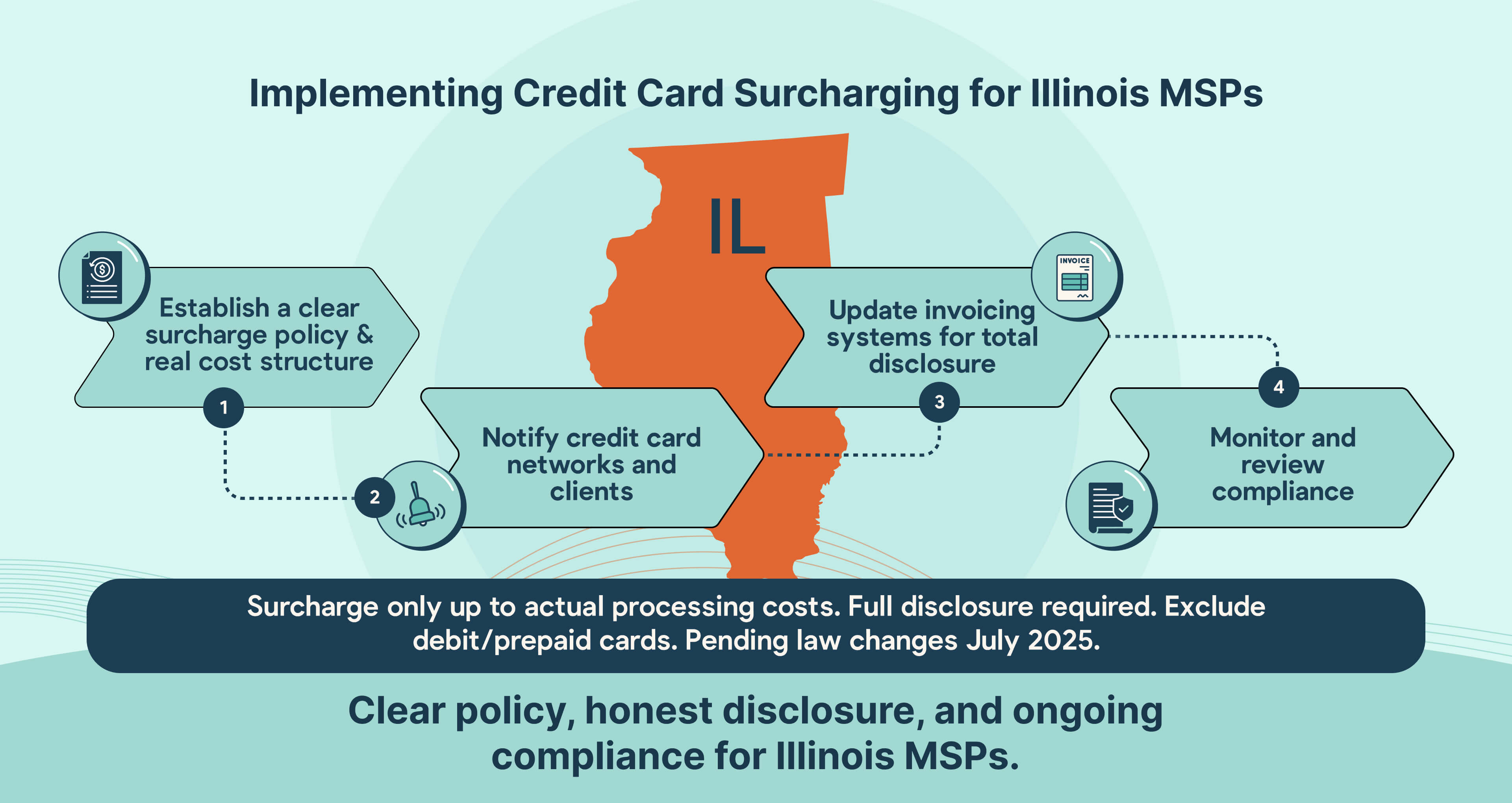

Follow these four steps to implement surcharging in a compliant and client-friendly way under Illinois law.

Step 1: Establish a Clear Surcharge Policy and Structure

Before you begin charging any fees, develop a formal policy that outlines:

- What types of transactions are subject to the surcharge

- How the fee is calculated (flat rate or tiered percentage)

- What measures is your MSP taking to remain compliant with Illinois’s Consumer Fraud and Deceptive Business Practices Act (815 ILCS 505), network rules from Visa, Mastercard, and Discover, and federal rules like the Durbin Amendment

MSPs in Illinois can use one of two surcharge models:

a) Fixed Percentage Approach

You set a single, consistent surcharge percentage for all credit card payments.

Example: A 2.85%surcharge on every credit card payment. A $7,100 invoice would include a surcharge of $202.35, for a total of $7,302.35.

b) Tiered Surcharge Model

The surcharge rate changes depending on the invoice size.

Example:

- 2% for transactions under $4,000

- 3% for transactions $4,000 and above

If a client is invoiced $3,600, the surcharge would be $72. For a $5,200 invoice, the fee would total $156.

Whatever structure you choose, it must reflect your actual average processing cost. Illinois law and card brand rules prohibit rounding up or estimating fees that exceed what you actually pay.

A general disclaimer, such as a surcharge may apply,” is not enough. The exact percentage or dollar amount must be stated before the client is charged.

Step 2: Notify Credit Card Institutions and Clients

Before implementing a surcharge policy, notify both your payment processor and the applicable card brands. Visa and Mastercard require merchants to submit notice at least 30 days in advance.

You can do this through your payment gateway or by submitting the official forms on the Visa and Mastercard websites.

Once that’s done, your next priority is your clients. Unexpected fees, no matter how small, can erode trust.

Make sure your surcharge policy is clearly explained in:

- Client onboarding materials

- Payment instructions or checkout pages

- Contracts or service agreements

- Invoices or recurring billing statements

Let’s say you send a client an invoice for $8,250, and you include a 3% surcharge without prior explanation. The client sees an extra $247.50 added to their total and isn’t sure what it’s for. That could lead to a payment dispute—or worse, a chargeback.

According to Swipesum, the average chargeback costs around $190 in fees, penalties, and administrative expenses. Preventing those disputes starts with proactive, written communication.

Step 3: Update Invoicing Systems

Illinois does not have a surcharge-specific statute, but merchants are expected to represent fees honestly and clearly under the Consumer Fraud Act. One of the best ways to comply is to itemize all surcharge amounts on client invoices and receipts.

Example:

- Managed IT Services: $6,900

- Credit Card Surcharge (2.75%): $189.75

- Total Due: $7,089.75

Step 4: Monitor and Review Compliance

You’ll need to revisit your policy regularly to ensure it still reflects your current costs and the legal environment in Illinois.

As of [$c-month-year]April 2025[$c-month-year], Visa limits surcharges to 3%, while Mastercard allows up to 4%—but only up to your actual merchant discount rate (MDR). For example, if you’re paying 2.7% to accept Mastercard, then 2.7% is your maximum surcharge.

Exceeding it could violate network rules and may be considered deceptive under Illinois law.

To remain compliant, your MSP should:

- Review your actual processing costs at least every three months

- Adjust your surcharge percentage if your rates change

- Ensure surcharge disclosures remain clear and easy to find

- Continue excluding debit and prepaid cards from surcharges as required by the Durbin Amendment and card brand restrictions.

Also, be aware of pending changes in Illinois law. While it doesn’t ban surcharges outright, it could affect how your MSP presents pricing and fee information, especially on marketing materials or proposals.

Additionally, the Interchange Fee Prohibition Act is scheduled to take effect on July 1, 2025. It will prevent interchange fees from being applied to the sales tax and gratuity portions of credit or debit transactions. This may impact how processors calculate their charges and influence how you structure your surcharge policies in response.

{{ebook-cta}}

The Role of FlexPoint in Streamlining Credit Card Surcharging for Illinois MSPs

Now that surcharging is permitted in Illinois, managed service providers have a clear opportunity to recover credit card processing fees, provided they follow a few core rules. Surcharges must apply only to credit card payments, be capped at your actual processing rate, and be disclosed to the client before they are charged.

FlexPoint is also a valuable tool here. The platform’s billing and invoicing automation features can:

- Apply surcharges only to eligible credit card transactions

- Calculate rates dynamically based on card type and processing fees

- Insert the surcharge as a separate line item on every invoice

- Keep internal records showing that the fee matches your actual processing cost

FlexPoint provides MSPs with a way to manage all of this without relying on spreadsheets or guesswork. The platform automatically calculates surcharges based on card type, ensures these fees are disclosed and labeled correctly, and keeps your billing process aligned with both Illinois law and the rules of Visa, Mastercard, and Discover.

Whether you want to recover 100% of your costs, share them with the client, or absorb them entirely, FlexPoint has flexible billing options that support your approach.

a) Interchange+ Plan

Not all MSPs choose to pass fees on to clients; instead, they cover them internally. FlexPoint supports this approach with its Interchange+ Plan.

This plan breaks down the interchange fees associated with each transaction type. Instead of a flat percentage, you’re billed according to the actual rate associated with each card brand and type.

For example, if a client pays $3,200 using a Visa rewards card with a 2.2% processing rate, you’d pay $70.40 in fees. If another client pays the same amount with a basic Mastercard that carries a 1.65% rate, the cost would be $52.80.

This transparency allows you to understand how different payment methods affect your costs, even if you don’t apply a surcharge.

b) Customer Surcharge Plan

If you, as an MSP, want to pass those fees on to clients, the Customer Surcharge Plan offers a compliant and automated structure for doing just that.

Suppose you invoice a client for $6,200, and your average processing rate is 2.65%. FlexPoint calculates the surcharge at $164.30, bringing the total to $6,364.30. The client sees this fee identified on their invoice, and your MSP keeps the full $6,200 as revenue.

Remember, Illinois law, enforced through the Consumer Fraud and Deceptive Business Practices Act, expects merchants to disclose any surcharge before a payment is made, and that the amount must reflect your actual cost.

FlexPoint supports compliance by:

- Applying surcharges only to eligible credit card transactions

- Blocking surcharges on debit and prepaid cards (which are not permitted under federal law or card brand rules)

- Generating clear invoices and portal messaging that aligns with state-level disclosure standards

For MSPs that want to recover some, but not all, of the processing fee, FlexPoint also enables a shared-cost model.

Suppose your credit card fee averages 2.6%. You could decide to pass 1.1% to your client and absorb the remaining 1.5% yourself.

The surcharge on a $5,900 invoice would be $64.90, and your MSP would cover the remaining $88.50. This balanced approach allows you to protect margins while remaining client-friendly.

Whether you choose to entirely shift the expense, share it, or simply track it, FlexPoint provides you with the tools to do so accurately and in compliance with Illinois law.

How FlexPoint Enhances Surcharging Compliance and Transparency

Even though Illinois permits credit card surcharges, that permission comes with very specific conditions. Managed service providers must strictly follow transparency rules, and the surcharge must never exceed the actual cost of processing the payment.

Adding a fee that is even slightly higher than your average processing rate, or failing to disclose the fee before the payment is processed, can lead to more than just a frustrated client. You could face chargebacks, formal disputes, or penalties under the Illinois Consumer Fraud and Deceptive Business Practices Act (815 ILCS 505).

FlexPoint helps MSPs sidestep these risks by building surcharge compliance into the billing workflow.

It calculates the correct surcharge amount based on card type, adds it to eligible transactions only, and includes it as a separate line item. This ensures that each invoice reflects Illinois disclosure standards and aligns with Visa, Mastercard, and Discover requirements.

Whether you choose to apply the full processing cost to the client or share it between your business and theirs, FlexPoint supports your policy while keeping every transaction compliant.

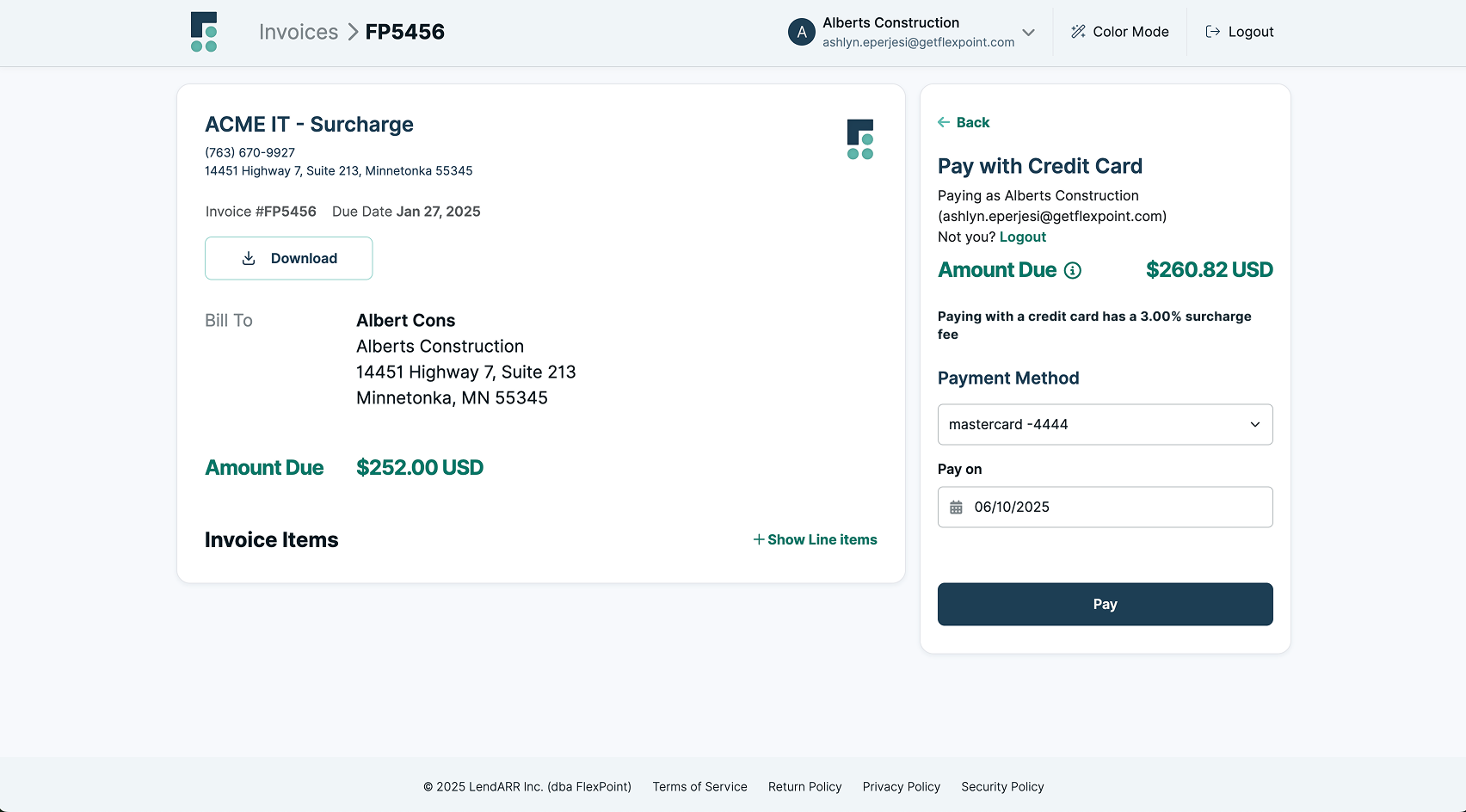

Here’s how an Illinois-compliant invoice generated through FlexPoint might appear:

FlexPoint’s Integration with MSP Tools for Seamless Billing

Managing operations across disconnected systems is a typical inefficiency for growing managed service providers (MSPs).

FlexPoint was built to solve that, offering native integrations with the tools Illinois-based providers already depend on, including:

When these platforms connect through FlexPoint, you get more than just convenience—you gain an end-to-end workflow that eliminates data duplication, manual entry, and reconciliation delays.

Everything, from invoicing to payment recording, happens in one place, so your financial data stays consistent. Your team can focus on service delivery instead of dealing with accounting workarounds.

This is especially important in Illinois, where surcharging is legal but must be tied to actual credit card processing costs and clearly disclosed to clients in advance.

For example, if you apply a 2.6% surcharge on a $5,000 invoice, FlexPoint records the $130 fee, links it directly to the payment method, and reflects it on both the client-facing invoice and your internal reporting.

It is not only your internal systems that benefit—FlexPoint also improves how clients interact with your billing.

Every Illinois MSP using FlexPoint can offer clients a white-label (or branded) secure payment portal where they can:

- Review fully itemized invoices, including a breakdown of services and any fees

- Manage ACH and credit card payment options

- View any applied credit card surcharge as a distinct line, separate from service charges

This also reduces the risk of chargebacks and delays. Clients can log in, see exactly why a $6,150 invoice includes a $159.90 surcharge (at 2.6%), and proceed with complete confidence.

From invoice generation to payment reconciliation, FlexPoint simplifies every step.

It eliminates time-consuming tasks, keeps payment records accurate, and supports surcharge compliance without complicating your internal workflows.

{{client-portal-gif}}

Offering Flexibility in Surcharging

{{admin-portal-gif}}

With FlexPoint, Illinois MSPs can decide how credit card surcharges are applied, down to the individual client. This client-level customization gives complete control over your billing strategy, making it easy to adjust fee policies based on account size, service scope, or the value of your long-term relationship.

This flexibility means you don’t have to adopt a one-size-fits-all approach. Instead, you can make strategic decisions that reflect your financial goals and client retention efforts.

Suppose your MSP has a client that pays $12,000 monthly and has been with you for five years. You may choose to absorb the 2.5% credit card fee ($300) as a loyalty benefit.

Meanwhile, for a new account billed at $2,750 per month, you might apply a 2.6% surcharge ($71.50) to preserve your margins while onboarding.

FlexPoint makes this possible without creating administrative complexity.

You can turn surcharging on or off per client, define who gets charged and who doesn’t, and rest assured that every applied fee complies with Illinois’s laws, as well as card brand and federal rules.

That flexibility is critical in a state like Illinois, where surcharges are permitted but must be tied to your actual cost and disclosed clearly in advance.

Alternative Cost-Effective Payment Method - ACH for Illinois MSPs

While surcharging offers Illinois MSPs a legal and structured way to recover card processing fees, it’s not the only method available to reduce payment costs.

Accepting ACH payments can be a simple, fee-friendly alternative that keeps billing straightforward for both your clients and your internal team.

Unlike credit card transactions, which can have fees ranging from 2% to 4%, ACH payments typically cost between $0.25 and $1.00 per transaction, regardless of the invoice amount.

There’s no need to monitor surcharge percentages, track card types, or worry about violating compliance rules tied to card brand limitations.

ACH offers a reliable path for MSPs looking to simplify payment acceptance while minimizing processing costs.

Clients also benefit. ACH transactions avoid the friction of added surcharges or unexpected fees. When MSPs steer clients toward ACH as the default payment option, they can maintain transparency, simplify the approval process, and avoid disputes over credit card fees.

Consumer behavior supports this shift.

A recent report from PYMNTS showed that nearly 75% of customers are less likely to use a credit card if an additional fee is involved. That means surcharges, while helpful in recouping costs, can potentially deter specific clients from completing payments as quickly.

Encouraging ACH usage can prevent that hesitation and keep payments flowing without added back-and-forth.

FlexPoint supports this strategy by offering Same-Day ACH, which allows Illinois MSPs to access cleared funds faster than the traditional 3–5 business-day timeline.

With FlexPoint, your ACH payments can settle within hours, giving you quicker access to revenue and better control over your cash flow.

Initiate a payment before the 4:00 PM ET cutoff, and the funds may arrive on the same business day, improving your cash flow and reducing your reliance on credit lines or short-term loans.

There are also additional operational benefits. ACH transactions typically carry a lower risk of chargebacks than credit card payments, resulting in less time spent handling disputes or reprocessing failed transactions.

When managed through FlexPoint, your ACH workflows are fully integrated, meaning you don’t have to track payments separately, manually reconcile bank deposits, or update your books by hand.

There are no hidden fees, last-minute charges, or confusion. Clients pay what they expect, and you keep more of your revenue where it belongs: in your business.

With FlexPoint, Illinois MSPs can easily promote ACH as a default option, speeding up payment cycles and reducing administrative overhead—all without sacrificing clarity, compliance, or client satisfaction.

Conclusion: Reduce Processing Costs AND Maintain Compliance for Illinois MSPs with Credit Card Surcharging

Illinois permits surcharges under its current legal structure, but only when those fees are applied correctly. That means disclosing the surcharge before the transaction takes place, limiting it to your actual cost, and ensuring clients understand how and why the fee appears on their invoice.

Failing to meet these expectations doesn’t just create friction—it can lead to enforcement under Illinois’s Consumer Fraud and Deceptive Business Practices Act (815 ILCS 505).

Card brand networks, such as Visa, Mastercard, and Discover, also impose strict requirements regarding surcharge calculation and notification.

To avoid the complexity of managing these overlapping standards, many Illinois MSPs rely on FlexPoint.

Enhance your MSP’s bottom line and compliance with automated credit card surcharging solutions from FlexPoint.

Schedule a demo to see how FlexPoint can transform your financial operations and maximize profitability.

{{demo-cta}}

Additional FAQs: Credit Card Surcharging in Illinois for MSPs

{{faq-section}}