Credit card surcharging allows managed service providers (MSPs) in Colorado to recover the expenses associated with credit card processing.

By passing a portion—or all—of these fees to clients, MSPs can maintain healthier profit margins and reduce operational costs without absorbing these expenses themselves.

However, Colorado MSPs must comply with federal laws, strict state-specific regulations, and card network policies. This includes adhering to limits on surcharge percentages and ensuring surcharge details are communicated to clients to prevent disputes or confusion.

This guide outlines Colorado’s surcharging rules, offers strategies for implementation, and explains how automation tools can simplify compliance while making the process more efficient.

Disclaimer: This content is for informational purposes only and does not constitute legal advice. MSPs should consult with a qualified attorney to address any legal or operational concerns.

What is Credit Card Surcharging for MSPs in Colorado?

Credit card processing fees can be a significant financial burden for MSPs in Colorado, typically ranging between 2% and 4% of every transaction.

These costs, which include interchange fees and processor markups, can quickly cut into profits, especially for businesses that process recurring payments or handle a large volume of credit card transactions.

Many businesses adopt credit card surcharging as a practical solution to mitigate these expenses.

Surcharging involves adding a fee—capped at 2% in Colorado—to a client’s invoice.

The client covers this fee when paying with a credit card. Instead of the MSP shouldering the entire financial burden, the responsibility is shared, improving overall cost efficiency.

Colorado’s 2% surcharge cap provides a clear framework for businesses.

For example, an MSP processing $80,000 in monthly credit card payments with a 2% processing fee would face $1,600 in monthly costs—or $19,200 annually.

The MSP fully recovers these costs by applying a 2% surcharge to client invoices, effectively balancing its operational budget.

Some MSPs may choose a partial surcharge to balance cost recovery and client satisfaction. For instance, a 1% surcharge transfers $800 of the monthly processing cost to clients while the MSP absorbs the remaining $800.

Over a year, this approach reduces expenses by $9,600.

To implement surcharging effectively, MSPs must sustain transparency. This approach builds client trust and ensures all fees comply with state, federal, and card network regulations.

The following sections will provide detailed guidance on meeting these compliance standards and managing client relationships.

{{cal-one}}

Understanding Credit Card Surcharging Laws in Colorado

As of [$c-month-year]January 2025[$c-month-year], Colorado permits credit card surcharging, providing MSPs with a valuable tool for managing processing fees.

Note: Federal laws, including the Durbin Amendment of the Dodd-Frank Act, prohibit surcharges on debit and prepaid cards, even if these are processed as credit transactions.

{{debit-cta}}

As such, MSPs must ensure surcharges are applied only to credit card transactions to remain compliant.

Colorado Senate Bill 21-091 legalized credit card surcharging in 2022, reversing previous restrictions that prohibited private businesses from imposing these fees.

Before this law, only government agencies and businesses offering cash discounts could indirectly manage processing costs.

The legislation now allows businesses to impose surcharges up to 2% of the transaction total or the actual processing cost, whichever is lower.

This cap ensures fairness for clients while providing a way for MSPs to offset payment expenses.

Card networks like Visa, Mastercard, Discover, and American Express may have additional requirements for surcharging.

Visa enforces a surcharge cap of 3%, but Colorado’s legal maximum is 2%, meaning merchants must adhere to the lower state limit, regardless of Visa’s guidelines.

Transparency is vital for maintaining compliance and client trust. MSPs in Colorado should ensure surcharge policies are communicated to clients during onboarding and include detailed itemization on invoices.

This practice clarifies charges, reduces disputes, and upholds professionalism.

Consider a Colorado MSP that processes $50,000 in monthly credit card transactions with an average processing cost of 2%.

The MSP pays $1,000 per month, or $12,000 annually, in processing fees if they do not implement surcharging.

If the MSP applies a 2% surcharge, clients shoulder these fees, allowing the MSP to recover the entire $12,000 annually.

Alternatively, the MSP might impose a 1% surcharge, transferring $500 per month to clients while absorbing the remaining $500, saving $6,000 annually.

Regardless of the chosen approach, best practices include:

- Notify Visa, Mastercard, and other networks 30 days before implementing surcharges.

- Inform clients of surcharges before payments are processed.

- Itemize surcharges on all invoices and receipts.

For detailed information on Colorado’s surcharging guidelines, visit the Colorado Attorney General’s Office.

If you are uncertain about the rules surrounding surcharging in Colorado, you should seek advice from a legal professional.

{{usa-cta}}

Implementing Credit Card Surcharging for Colorado MSPs

Introducing credit card surcharges requires thoughtful planning for MSPs, as these fees influence client perceptions and experiences.

Success depends on framing surcharges as a necessary measure to balance operational costs rather than as an added financial burden for clients.

Clients value transparency, especially regarding financial matters. Before rolling out surcharges, MSPs can initiate conversations through personalized emails or phone calls.

These touchpoints provide an opportunity to explain how surcharges help offset rising payment processing costs and ensure the sustainability of services.

Sharing concrete data, such as the percentage of revenue consumed by processing fees, can help clients understand the significance of surcharges.

MSPs can also introduce surcharges as part of a broader initiative to maintain high service standards while managing costs.

A clear explanation, such as: "This adjustment allows us to continue providing exceptional services without impacting all clients equally," can build understanding and trust.

These options provide flexibility and demonstrate a commitment to client satisfaction, reducing potential friction during the transition.

When approached thoughtfully, surcharges can support operational goals while preserving strong client relationships.

The following guide outlines actionable steps MSPs in Colorado can take to implement surcharges effectively, stay compliant, and maintain client trust.

Step 1: Establish a Clear Surcharge Policy and Structure

Creating a detailed surcharge policy is a foundational step for successful implementation.

This policy should outline the surcharge percentage, specify when it applies, and describe how it will be communicated to clients. Including the policy in service agreements will foster transparency and set upfront expectations.

Surcharges should be presented as a way to recover credit card processing costs rather than as a means to generate profit. A well-structured policy that aligns the surcharge with operational expenses strengthens trust.

Colorado MSPs choose from three standard surcharge models to suit their business needs:

Examples of Surcharge Structures

1. Fixed Percentage Surcharge

A consistent percentage is added to all credit card transactions, limited to Colorado’s legal cap of 2% or the merchant’s actual processing cost, whichever is lower.

Example: A $12,000 invoice incurs a 2% surcharge, adding $240 to the total, resulting in $12,240.

2. Tiered Surcharge System

Different surcharge rates are applied based on invoice amounts.

Example:

- Transactions under $5,000 incur a 1.5% surcharge.

- Transactions over $5,000 incur a 2% surcharge.

A $4,500 invoice would have a 1.5% surcharge of $67.50, while a $7,500 invoice would include a 2% surcharge of $150.

3. Flat Fee Surcharge

A fixed amount is added to each transaction regardless of size.

Example: A flat fee of $35 is applied to a $2,000 invoice, bringing the total to $2,035.

Important Note: Flat fee surcharges must not exceed the actual processing cost. For instance, if a $300 transaction incurs a 2% processing fee, resulting in a $6 cost, applying a $35 surcharge would violate compliance. The surcharge must instead match the actual cost, staying within $6.

Step 2: Notify Credit Card Institutions and Clients

The next critical step for MSPs in Colorado to ensure surcharging compliance is to inform both credit card networks and clients.

Card networks like Visa and Mastercard require merchants to provide written notice at least 30 days before implementing surcharges. This notification process is straightforward and helps prevent potential disputes or penalties.

Mastercard states:

“A merchant's ability to apply a surcharge is conditioned on the merchant's satisfaction of certain disclosure requirements. These disclosure requirements include advance notice to both Mastercard and the merchant's acquirer of the merchant's intention to impose a surcharge no less than thirty days before the merchant implements a surcharge.”

Once the required notice has been given to the networks, MSPs should focus on informing their clients.

Communicating surcharge policies proactively builds trust and prevents misunderstandings. Clients are more likely to accept surcharges if they understand these fees are designed to recover costs rather than generate profit.

Proactively explaining surcharges also reduces the risk of chargebacks, which can be costly and time-consuming.

According to Swipesum, chargebacks average $190 per dispute and are often the result of unexpected or unclear fees. Upfront communication minimizes these risks.

If an MSP sends a $9,000 invoice with a 2% surcharge, adding $180, but fails to disclose the fee clearly, the client might dispute the charge. Payment disputes could result in chargeback costs, penalties, and lost time resolving the issue.

By maintaining transparency and open communication, MSPs can reduce chargebacks, safeguard revenue, and uphold strong client relationships.

Step 3: Update Invoicing and Payment Systems

MSPs that charge surcharges must ensure their billing systems accurately present these charges. Surcharges should be listed as separate line items on invoices so clients can easily ascertain what the charge means.

For instance, an invoice for $4,000 with a 2% surcharge might display as:

- Service Total: $4,000

- Credit Card Surcharge (2%): $80

- Total Due: $4,080

Automated solutions like FlexPoint simplify this process by automatically calculating surcharges and adding them to invoices. This approach minimizes manual entry errors and ensures invoices comply with Colorado’s surcharge regulations.

Integrating automated solutions into billing workflows allows MSPs to focus on business priorities and be confident their payment processes are accurate and in line with regulatory requirements.

Step 4: Continuously Monitor Compliance

Compliance requires ongoing attention. Regularly assessing surcharging practices ensures alignment with federal laws and card network policies.

For example, Visa lowered its surcharge cap to 3% in 2023, requiring businesses to adjust their practices to avoid penalties.

While this change did not affect Colorado MSPs due to the state’s 2% surcharge limit, it highlights how quickly regulations can shift and the importance of staying informed.

Even if specific changes don’t apply locally, monitoring industry updates helps MSPs remain prepared and maintain compliance in other operational areas.

Frequent reviews of surcharging policies reduce the risk of penalties and cultivate trust with clients by demonstrating a commitment to accountability and professionalism.

{{ebook-cta}}

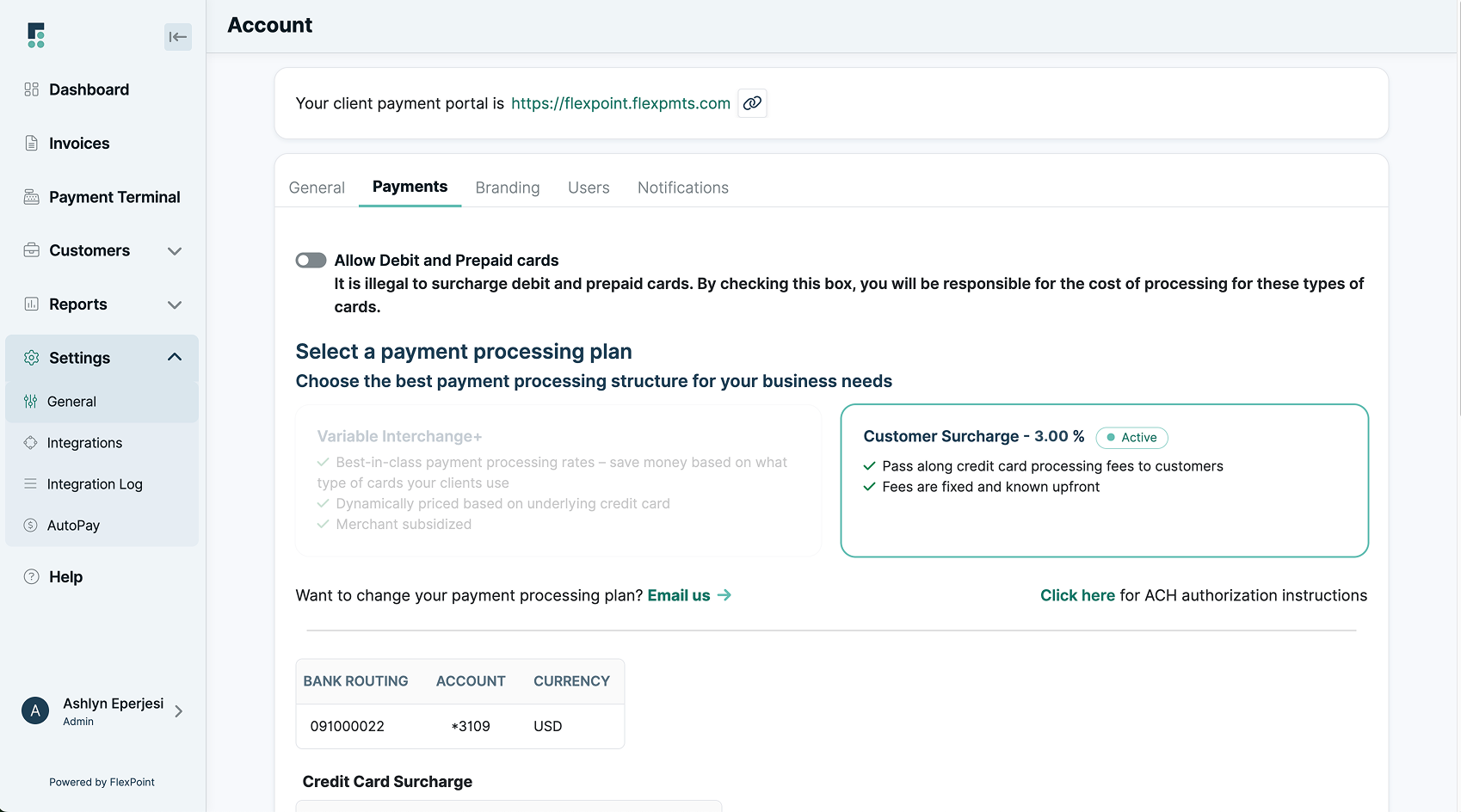

The Role of FlexPoint in Streamlining Credit Card Surcharging for Colorado MSPs

Many MSPs face high daily transaction volumes, and credit card fees can quickly cut profits.

Managing these costs effectively is crucial for financial stability, and FlexPoint offers tailored payment automation solutions designed specifically for MSPs to do so.

Payment Processing Plans

FlexPoint provides two distinct options to help MSPs streamline billing and manage fees:

a. Interchange+ Plan

Interchange+ offers MSPs a transparent way to manage fees without adding surcharges to client invoices.

This plan aligns processing costs with interchange rates, which vary depending on the type of card used.

For example, with their lower interchange rates, Discover cards can reduce fees for the MSP.

Conversely, American Express and premium reward credit cards tend to have higher rates, which may increase processing costs.

The Interchange+ Plan is a good fit for MSPs who prefer to absorb processing fees while maintaining predictable costs and transparent pricing.

b. Customer Surcharge Plan

This plan applies a flat percentage surcharge to credit card transactions for MSPs planning to pass processing fees to clients.

Given Colorado's 2% surcharge cap, this option helps MSPs remain compliant while recovering costs.

Example:

For a $5,000 transaction with a 2% surcharge:

- Service Total: $5,000

- Surcharge (2%): $100

- Total Due: $5,100

This plan is ideal for MSPs focused on balancing cost recovery and client transparency.

FlexPoint also supports a shared-cost model, allowing MSPs to split processing fees with clients. This flexibility can strengthen client relationships while easing financial strain on the business.

With FlexPoint's flexible payment processing plans, Colorado MSPs can manage credit card fees efficiently while maintaining compliance and client satisfaction.

How FlexPoint Enhances Surcharging Compliance and Transparency

FlexPoint automates fee calculations and ensures compliance with Colorado's distinctive regulations, federal laws, and card network guidelines, eliminating the guesswork associated with surcharging.

This includes Colorado's 2% surcharge cap, which is lower than the federal limit and must always take precedence.

Here’s an example of how an invoice processed through FlexPoint might look with a 2% surcharge:

Colorado MSP Client INVOICE

Company Name: Your MSP

Invoice #: 025478

Invoice Date: March 10, 2025

Due Date: April 24, 2025

Bill To:

[Client Company Name]

[Client Address]

[Client Contact Name]

[Client Email]

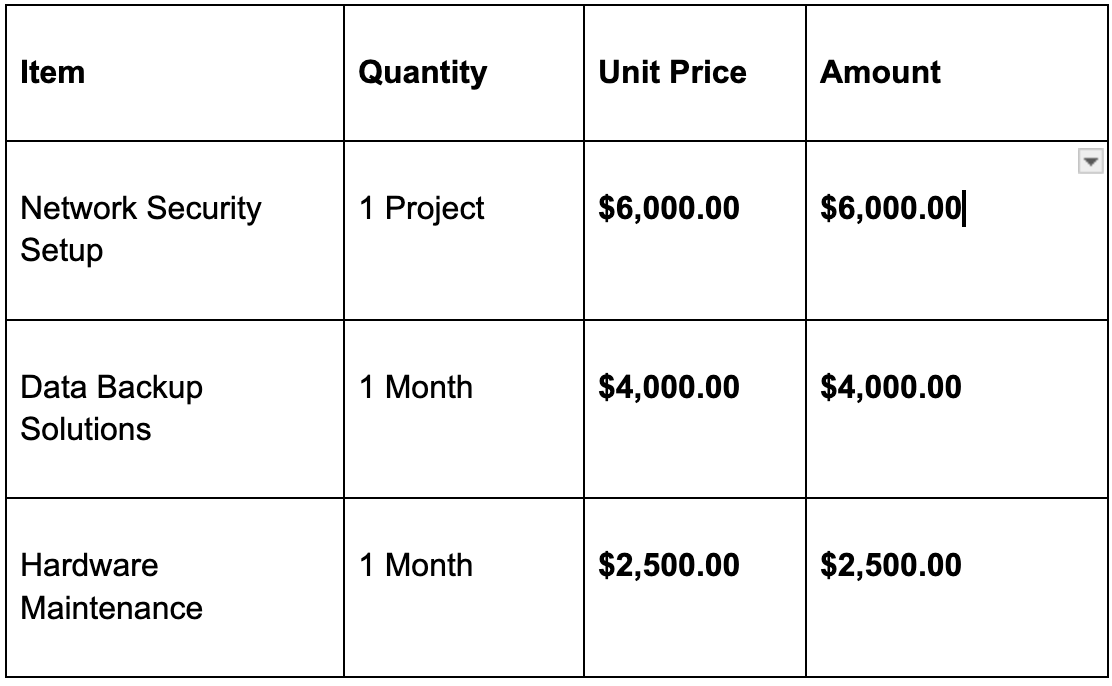

Services Provided:

- Network Security Setup

- Data Backup Solutions

- Hardware Maintenance

Description:

Subtotal: $12,500.00

Surcharge (2% of Subtotal): $250.00

Total Due: $12,750.00

Payment Terms:

Payment is due within 45 days of the invoice date. The surcharge complies with Colorado's 2% cap, federal laws, and card network requirements.

Notes:

We value your business and are here to help. Please reach out to [Your Contact Information] with any questions or concerns.

This example showcases how FlexPoint ensures surcharges are calculated accurately and integrated seamlessly into client invoices, saving time and reducing the risk of non-compliance.

With its automated billing features, FlexPoint helps MSPs streamline operations, maintain transparency, and focus on growing their business.

FlexPoint’s Integration with MSP Tools for Seamless Billing

FlexPoint connects seamlessly with widely used business tools, offering Colorado MSPs a comprehensive platform for managing invoicing, billing, and reconciliation.

These integrations include:

These integrations minimize manual administrative tasks, freeing MSPs to focus on client relationships and service delivery.

FlexPoint simplifies workflows by syncing payment details, surcharge amounts, and reconciliation updates across all integrated platforms. This diminishes the risk of manual errors and ensures financial data stays consistent across systems.

For example, FlexPoint’s integration with QuickBooks Online automatically applies real-time payments and surcharges to invoices.

MSPs benefit from instant updates on payment statuses, expediting month-end accounting, and creating a smoother financial process.

FlexPoint goes beyond essential integration by providing tools like branded client payment portals and live financial reporting.

- Branded Client Portals: Offer clients a professional payment experience while maintaining consistency with your MSP’s branding.

- Live Reporting: Access real-time data to scrutinize cash flow, surcharges, and payment trends.

By integrating these platforms and their advanced features, FlexPoint supports Colorado MSPs in reducing administrative burdens, improving accuracy, and focusing on expansion.

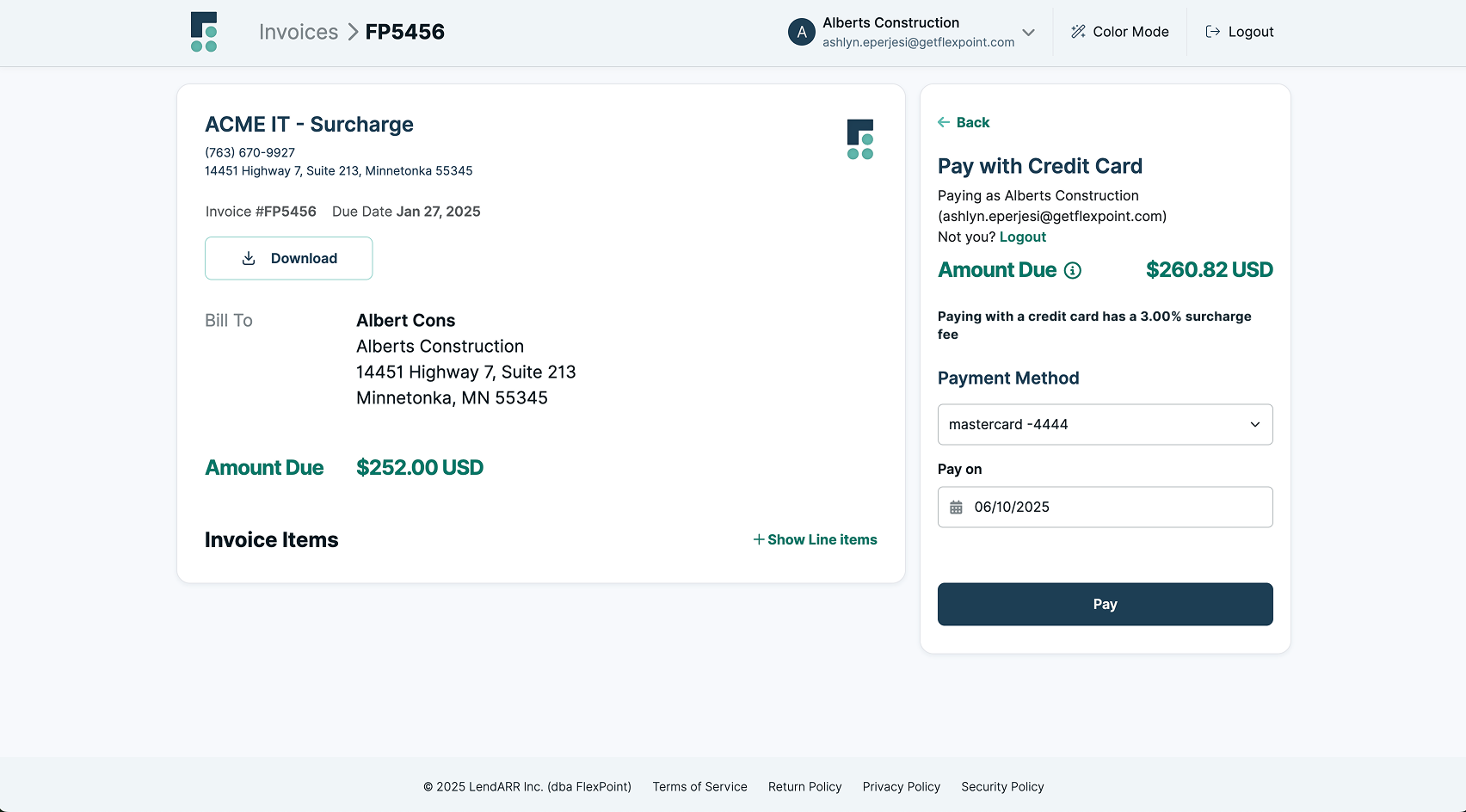

{{client-portal-gif}}

Offering Flexibility in Surcharging

{{admin-portal-gif}}

MSPs can rely on FlexPoint to implement surcharging practices tailored to their business needs while maintaining strong client relationships. This approach helps MSPs balance cost recovery with client satisfaction by applying surcharges strategically.

For example, MSPs may waive surcharges for high-value or long-term clients and apply them to other transactions to more effectively cover operational expenses.

Before completing payments, clients must also receive detailed information about surcharges to reinforce trust and ensure compliance.

The payment portals provided by FlexPoint allow clients to manage their payment preferences seamlessly.

For instance, a client using American Express may switch to Discover to reduce surcharge fees. The ability to update payment methods independently also reduces administrative work for MSPs.

With its emphasis on flexibility, compliance, and client-focused tools, FlexPoint helps Colorado MSPs implement surcharging strategies that align with their financial goals while preserving strong client relationships.

Conclusion: Streamlining Payments with Effective Surcharging Strategies

Payment processing fees can reduce the profitability of Colorado MSPs. Credit card surcharging offers a practical solution: MSPs can share these costs with clients.

However, this process must be handled carefully to meet federal laws, Colorado’s state guidelines, and card network regulations.

To comply with Colorado’s cap of 2% on surcharges, MSPs must itemize fees on invoices and inform clients about these charges before payment is processed.

Failure to disclose fees or exceeding the allowed surcharge percentage can result in penalties, client dissatisfaction, or card network restrictions.

FlexPoint streamlines the surcharging process through its specialized payment automation platform, which is tailored for MSPs. The system automates surcharge calculations, keeping them within legal and network limits, and integrates compliance into everyday operations.

It also helps MSPs manage surcharging without administrative burdens, from precise fee calculations to transparent invoicing.

Enhance your MSP’s bottom line and compliance with automated credit card surcharging solutions from FlexPoint.

Stay within Colorado’s regulations and simplify your MSP payment processes using FlexPoint today.

Schedule a demo to see how FlexPoint can transform your financial operations and maximize profitability.

{{demo-cta}}

Additional FAQs: Credit Card Surcharging in Colorado for MSPs

{{faq-section}}