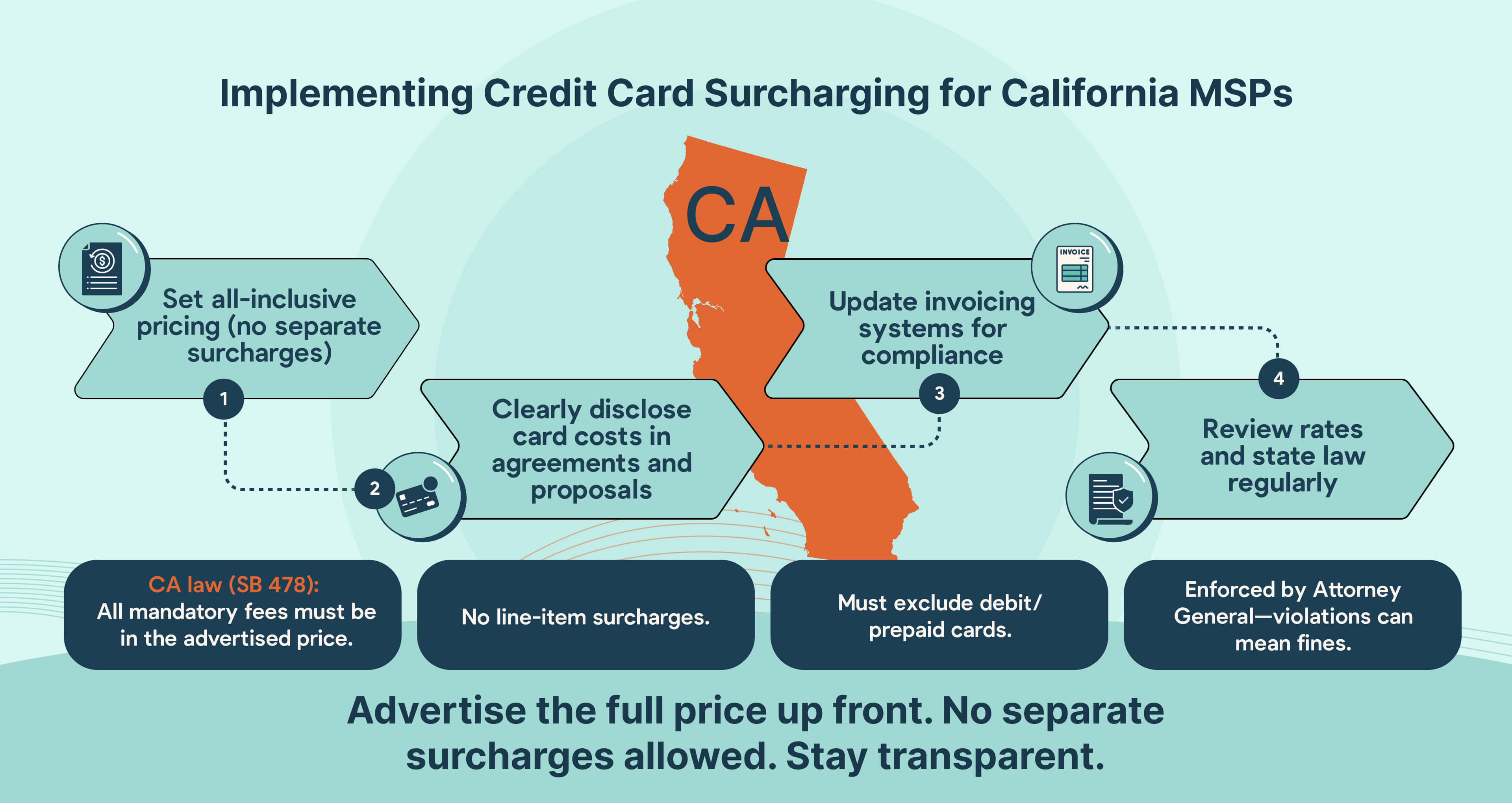

In California, credit card surcharging for MSPs is not outright banned as of [$c-month-year]April 2025[$c-month-year], but strict transparency laws passed in 2024 now regulate how these fees can be disclosed and applied.

As per an amendment of California’s “Hidden Fees Statute,” SB 478, that took effect on July 1, 2024, any required charge, including credit card surcharges, must be included in the upfront, advertised/listed price on invoices or during transactions.

Adding a separate fee at checkout without clear advance notice is no longer permitted under state law.

This means California MSPs may still be authorized to recover credit card processing costs with surcharging, but only if the pricing is structured correctly, as this article will discuss.

For MSPs that regularly bill clients via credit card, absorbing those fees outright or restructuring prices can significantly affect profitability. Over time, those small percentages stack up, particularly on high-value, recurring payments.

This article will help California MSPs understand the current surcharge rules and their legal basis. It will also explore compliant alternatives to manage payment costs, like promoting ACH payments or offering transparent cash discounts.

It will cover practical pricing examples and how payment automation tools can simplify compliance while helping you protect your margins.

Disclaimer: This information is intended for general educational purposes only. It should not be taken as legal advice. California MSPs should perform their own due diligence and consult with a qualified legal professional before introducing surcharges or modifying payment practices.

What is Credit Card Surcharging for MSPs in California?/

Credit card surcharging refers to the practice of charging clients an additional fee, usually a percentage of the total amount, when they choose to pay with a credit card.

The goal is to cover the transaction fees charged by Visa, Mastercard, American Express, and Discover, which typically range from 2% to 4%, depending on the card and provider.

In many U.S. states, MSPs are permitted to add a surcharge if they provide upfront notice and stay within limits set by the card brands and federal law.

For example, an MSP might add a 2.8% fee to a $7,500 invoice, resulting in a total charge of $7,710. That extra $210 goes toward covering the processing fee rather than reducing the MSP’s revenue.

California, however, takes a stricter approach, as discussed in the following section.

Following California’s disclosure rules helps MSPs comply and avoid payment disputes, while also prompting them to consider lower-cost payment options, such as ACH transfers or direct bank debits.

With the right approach and compliant tools, you can maintain clarity, consistency, and profitability in your billing practices.

{{cal-one}}

Understanding Credit Card Surcharging Laws in California

Rather than banning the practice of surcharging entirely, California requires that any fee tied to the use of a credit card be fully included in the advertised price or invoices.

Under the state's new pricing transparency law, this rule took effect on July 1, 2024, as part of a broader effort to eliminate hidden or unexpected charges at checkout.

This law stems from California Civil Code Section 1770(a)(29), introduced through Senate Bill 478 (California’s “drip pricing law”), and applies to nearly every type of business transaction, including managed services.

The statute prohibits any seller from advertising or offering a product or service at one price and then adding a separate charge later. That includes credit card surcharges, regardless of whether they are a flat fee or a percentage-based upcharge.

MSPs operating in California must account for credit card processing costs in their pricing, but they can’t advertise a base price and then add a fee just because a client uses a Visa or Mastercard. They must display the total price upfront, including any card-related fees.

Here’s what that looks like in practice.

Suppose you charge $1,500 per month for your managed IT services. Your average processing rate across all credit cards is 2.9%.

Instead of listing the service at $1,500 and adding a $43.50 card fee at checkout, your listed price must be $1,543.50—regardless of the payment method. Only then would you be in compliance with California’s pricing laws.

Transparency in Credit Card Surcharging Practices for California MSPs

California’s surcharging policy was implemented to avoid what state regulators call “junk fees”—surcharges or service charges that appear late in the buying process after the consumer has already made a decision based on the original price.

For MSPs, this means transparency isn’t optional. It’s a legal requirement tied to consumer protection enforcement, and violating it can result in both civil penalties and exposure to class-action lawsuits.

That said, California does still permit cash discounts (as do all other states), as long as they are clearly communicated and uniformly applied. This can be a practical workaround for MSPs who want to encourage clients to pay by ACH or direct bank debit.

Instead of charging more for credit card use, you advertise the higher, all-inclusive price and offer a discount for using a non-card method.

For example, if your quoted price is $2,060 (which includes credit card costs), you could reduce the invoice to $2,000 for clients who pay by bank transfer.

Framed this way, you’re not penalizing card usage but rewarding alternative methods.

This structure complies with both state law and card network rules. It can be set up with minimal administrative hassle using platforms like FlexPoint, which automatically applies discounts based on payment type.

Federal Guidelines and Their Interaction with California Laws

California’s requirements also align with card network policies and federal guidelines, including the Durbin Amendment of the Dodd-Frank Act, which specifically bans surcharges on debit and prepaid cards in all forms.

{{debit-cta}}

Although Visa and Mastercard permit credit card surcharges under federal law and their internal merchant agreements, they defer to stricter state restrictions.

That means even if your payment processor allows surcharges, it must still comply with California’s rules, ensuring that all mandatory fees are reflected in your base pricing and not added after the fact.

Payment processors and gateways that fail to enforce California’s pricing laws risk penalties from state regulators and the networks themselves.

Merchants who violate these laws face potential fines of $1,000 or more per incident, mainly if the pricing practice is found to be misleading or inconsistent.

Repeat violations or client complaints can lead to the suspension of your merchant account or even lawsuits under the state’s Consumer Legal Remedies Act.

While some states have challenged surcharge bans in court, arguing that such laws violate free speech rights by restricting how businesses describe their pricing, California’s policy takes a different route. It doesn’t restrict your ability to charge more for credit card usage.

Instead, it mandates that whatever fee you plan to charge be fully disclosed in advance. The legal emphasis is on fairness, transparency, and consistency.

There has been some pushback, especially from industries like restaurants and hospitality, which often rely on service fees and surcharges to cover rising operating costs.

In response, the legislature passed a narrow exemption through SB 1524 for food and beverage establishments, allowing them to list specific fees separately as long as they’re clearly disclosed on all menus and price displays.

However, this exemption does not apply to MSPs or other professional services. For most businesses, the requirement to include all credit card-related fees in the advertised price still stands.

While it’s possible future amendments could provide additional flexibility, there is no guarantee.

Until then, California’s pricing laws remain in full force, and enforcement is expected to grow more aggressive as regulators continue to crack down on what they view as deceptive fee structures.

Adding to the complexity, a federal judge previously ruled California’s original credit card surcharge ban unconstitutional in 2015 on First Amendment grounds.

That decision gave businesses temporary flexibility to impose surcharges, provided they followed transparency rules and stayed within card network limits.

However, the introduction of SB 478 effectively replaced the old surcharge ban with a broader pricing law focused on consumer disclosure, reintroducing confusion around how surcharges should be applied.

Accordingly, the safest—and most widely accepted—approach is to treat those fees as falling within the law’s scope and include them in your upfront pricing.

MSPs are advised not to gamble on this uncertainty. Even if a surcharge might be viewed as optional in isolation, the risk of client confusion or enforcement makes it far safer to embed the fee in your total service price.

Tools like FlexPoint make that easier to implement—automating invoice adjustments, syncing client payment preferences, and ensuring your quoted prices are compliant across all platforms and payment types. We will discuss this further in the upcoming sections.

California MSPs are urged to consult legal counsel before implementing any surcharge program.

{{usa-cta}}

Implementing Credit Card Surcharging for California MSPs

Survey data shows that clients don’t always respond well to surcharges.

According to a PYMNTS survey, more than 70% of U.S. consumers report being less likely to use a credit card when surcharges are added. About 42% say they would switch vendors entirely to avoid those fees.

A poorly implemented pricing model can lead to disputes, chargebacks, or state enforcement actions.

The best way to prevent this is to build a pricing model that reflects your processing costs in advance and explain it clearly.

The following steps help California MSPs approach credit card surcharging correctly.

Step 1: Establish a Clear Surcharge Policy and Structure

California law requires that the total price, including any mandatory charges, be listed upfront. So, rather than adding a 2.9% surcharge at the time of payment, MSPs must quote a fully inclusive amount that already takes into account credit card usage.

This means defining a pricing strategy internally that explains the following:

- How you calculate average processing rates

- Which services or client types those rates apply to

- How and when you offer discounts for lower-cost payment methods

MSPs typically choose between two surcharge models:

a) Fixed Percentage Surcharge

In this case, if your average processing fee is estimated at 2.9% (for example), you might adjust a $6,200 service package to be listed and quoted at $6,380, reflecting the built-in cost of credit card acceptance.

This approach complies with California’s pricing law by ensuring the total shown to the client already includes all applicable fees—no additional charges are added at checkout.

b) Tiered Surcharge System

In California, MSPs who want to account for processing fees based on invoice size must do so by adjusting the total price upfront, before presenting it to the client.

Example:

For invoices under $3,500, you might price your services 2% above the base rates, and for invoices of $3,500 and above, at 3%.

- A service package initially priced at $2,800 would be listed at $2,856 to account for average card fees.

- Using the same logic, a higher-tier engagement at $4,000 would be quoted at $4,120.

This tiered pricing model is permitted in California, but only if the total shown to the client includes the card fee and does not display it as a separate line item.

Step 2: Notify Credit Card Institutions and Clients

Even though California MSPs are prohibited from adding separate line-item surcharges, clients still need to understand how and why their pricing is structured.

While the law mandates that fees be included in the advertised price, it doesn’t remove the need for transparency.

MSPs should clearly explain that their listed pricing reflects the typical costs associated with accepting credit card payments, including fees from providers like Visa, Mastercard, American Express, and Discover.

These card networks allow surcharging in many states. Still, in California, their rules defer to stricter state laws that require all mandatory fees to be disclosed upfront, within the total advertised price.

To avoid confusion or pushback from clients, it’s important to proactively share this information in:

- Master service agreements (MSAs)

- Initial proposals or quotes

- Payment policies and onboarding documents

Including clear language about credit card-related pricing protects your MSP from miscommunication and reduces the risk of disputes, chargebacks, or non-compliance with California law and credit card company requirements.

Step 3: Update Invoicing Systems

Presenting credit card surcharges as separate fees at the time of payment may be interpreted as deceptive pricing under California’s Consumer Legal Remedies Act, even if the surcharge aligns with Visa or Mastercard rules elsewhere.

Example of a non-compliant invoice (not allowed in California):

- Monthly Services: $6,100

- Credit Card Surcharge (2.85%): $173.85

- Total Due: $6,273.85

This approach would violate California law because the card-related fee was not included in the original advertised or quoted price. Even though such formats are permitted in some states, California requires a different billing strategy, which is discussed later in this article.

As such, an MSP might need to update its invoicing systems to ensure compliance with all relevant laws.

You can apply conditional pricing, automate ACH discounts, and ensure every line item aligns with both state regulations and card network expectations—even if those expectations differ from state to state.

Step 4: Monitor and Review Compliance

Even with compliant pricing models in place, ongoing monitoring is essential. Processing rates fluctuate, card brand rules evolve, and enforcement trends can shift, especially as regulators continue to target so-called “junk fees.”

Although California law prevents visible surcharges, pricing must still be grounded in real processing costs.

Inflating prices far beyond what’s required to cover merchant fees could still raise red flags with the California Attorney General’s office or consumer advocacy groups, especially if clients aren't made aware of how pricing is structured.

Note: Surcharges or pricing adjustments must never be applied to debit or prepaid card transactions. This is strictly prohibited under the Durbin Amendment, part of the Dodd-Frank Act, which bars merchants from applying extra fees to those card types, even when processed as credit.

To maintain compliance in California, MSPs should:

- Regularly review effective processing rates for each card brand

- Ensure any card-related pricing adjustments match real costs (not arbitrary markups)

- Avoid applying card-inclusive pricing logic to debit or prepaid card payments

- Monitor legal updates, including new interpretations of SB 478, enforcement actions, or advisory opinions

Any future changes—whether from card brands (like Visa’s 2023 reduction of its surcharge cap) or legislative clarifications in California—may require quick changes to your pricing or invoicing system.

{{ebook-cta}}

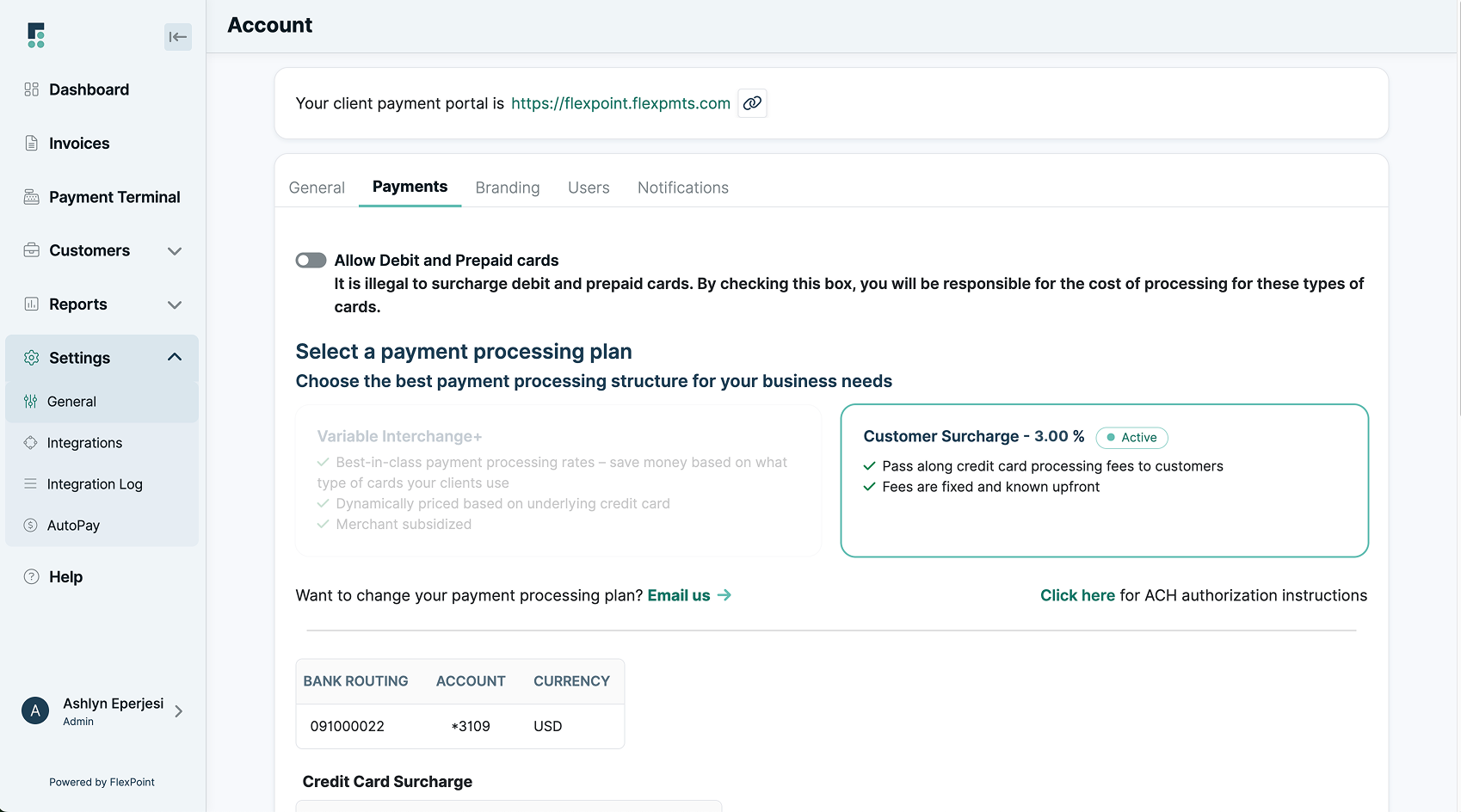

The Role of FlexPoint in Streamlining Credit Card Surcharging for California MSPs

While surcharging is technically permitted for many California MSPs, the state’s pricing transparency law (SB 478) prohibits displaying credit card fees as separate charges.

Instead, all mandatory costs must be built into the advertised price. This makes passing along processing fees more complex, especially for MSPs aiming to stay competitive without cutting margins.

FlexPoint simplifies this process with payment tools designed explicitly for MSPs operating in regulated environments, such as California.

Whether you choose to absorb card fees or encourage clients to use ACH, FlexPoint offers flexible, legally compliant ways to manage cost recovery through automation and transparency.

For MSPs that want to build credit card acceptance costs into their standard pricing while complying with SB 478, FlexPoint’s Interchange+ Plan is an effective solution.

Interchange+ pricing separates the wholesale cost of each card transaction—known as the interchange fee—from the processor's markup.

Unlike flat-rate models, this structure provides complete visibility into what you’re paying, whether it’s for a basic debit card or a premium rewards card, like American Express.

Example:

You typically bill $8,250 for your monthly services. With an estimated blended credit card fee of 2.75%, you would set your listed price at $8,477. Clients see one flat, final amount with no hidden fees, meeting both legal and client expectations.

This model works well for California MSPs who prefer not to offer alternative payment incentives and instead absorb processing variability through fixed, compliant pricing.

How FlexPoint Enhances Surcharging Compliance and Transparency

As of [$c-month-year]April 2025[$c-month-year], credit card surcharge visibility is strictly limited in California due to SB 478.

MSPs cannot add fees after the fact or itemize surcharges on invoices. Even though Visa, Mastercard, and other card brands are allowed to charge surcharges under federal rules, they defer to state law in jurisdictions like California.

FlexPoint reduces the risk of noncompliance by embedding state-aligned pricing logic directly into your billing system.

You can calculate blended card rates, apply client-specific payment preferences, and produce invoices that meet both California law and card brand standards, without displaying a separate surcharge line.

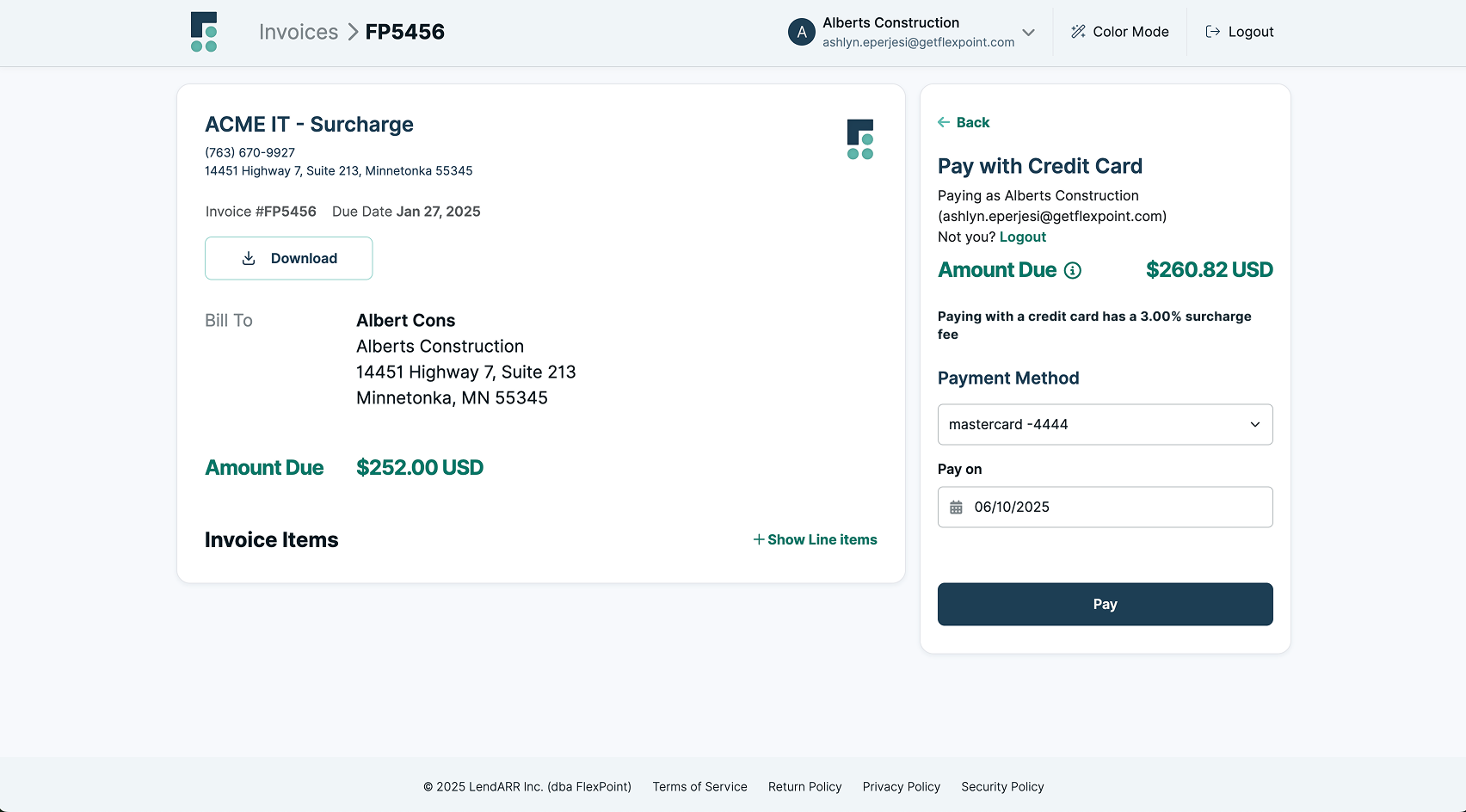

Here’s an example of how a FlexPoint-generated invoice might list these fees and charges to support surcharge compliance in California:

Example: California MSP Client Invoice

FlexPoint’s Integration with MSP Tools for Seamless Billing

FlexPoint integrates directly with the accounting and PSA platforms used by California managed service providers (MSPs) to manage daily operations.

These include:

This integration ecosystem brings your invoicing, billing, and reconciliation systems into one unified environment.

Instead of exporting invoices or updating records manually, FlexPoint syncs payment activity in real time, streamlining internal workflows and reducing the risk of discrepancies.

For example, if you use QuickBooks to issue monthly invoices, FlexPoint ensures payments (whether by credit card or ACH) are reflected immediately, giving your finance team a real-time view of cash flow.

This automation is especially valuable for MSPs required to comply with California’s SB 478, as it ensures all client-facing prices are consistent with what is recorded internally, with no surprise fees or invoice mismatches.

FlexPoint also tracks ACH discounts and embedded card costs within each transaction, helping MSPs verify that all charges align with California’s requirement to present the full price upfront. This protects both you and your clients—supporting billing clarity, compliance, and faster payment cycles.

Beyond internal systems, FlexPoint provides California MSPs with a branded client payment portal designed to reduce friction and simplify the payment experience.

Clients can log in to:

- View invoices

- Manage saved ACH and credit card payment methods

- See pricing that reflects any card cost recovery as part of the full-service total

This level of clarity minimizes billing questions and gives clients confidence in your process, while saving your team hours of follow-up and reconciliation work.

In short, FlexPoint reduces administrative burdens, promotes transparent pricing, and helps California MSPs deliver a compliant and client-friendly payment experience.

This gives you the flexibility to adjust surcharge strategies based on factors like:

- Client size or invoice volume

- Contract tenure

- Preferred payment method

For instance, you could include a varying discount for long-term clients or those with higher invoice volumes, creating a clear incentive to grow the relationship while still recovering card processing costs.

FlexPoint’s automation ensures this pricing logic is applied accurately and consistently—no manual recalculations or exceptions are needed. Each client’s billing rules are stored within their profile, and all generated invoices reflect the compliant, pre-quoted price. This approach gives you full control over how you manage cost recovery, while protecting profitability, supporting retention, and complying with California’s legal requirement to disclose the full price.

Alternative Cost-Effective Payment Method - ACH for California MSPs

.jpeg)

For California MSPs who want to avoid the legal complexities of credit card surcharging or simply reduce costs without upsetting clients, ACH payments provide a practical and compliant solution.

With SB 478 limiting how fees can be disclosed and applied, more MSPs are turning to ACH as a clean, low-cost alternative that delivers both savings and convenience.

ACH (Automated Clearing House) payments are direct transfers from a client’s bank account to yours.

Unlike credit cards, no percentage-based processing fee is tied to rewards programs or interchange rates. Instead, you’re typically looking at a flat fee between $0.25 and $1.00 per transaction.

Compare that to the ~3%–4% cost of a typical credit card payment, and the savings quickly become clear.

Beyond lower fees, ACH reduces friction, improves security, and streamlines billing operations. With FlexPoint, you can automate ACH debits with client authorization, set up recurring payments, and eliminate the delays and risks associated with paper checks.

With the launch of FlexPoint’s Same-Day ACH, California MSPs no longer need to wait three to five business days for funds to clear.

Initiate a payment before the 4:00 PM ET cutoff, and the funds may arrive on the same business day, improving your cash flow and reducing your reliance on credit lines or short-term loans.

ACH also helps reduce chargebacks. Because funds are pulled directly from the client’s bank account with authorization, disputes are less frequent and typically easier to resolve than credit card chargebacks, which can cost around $190 per incident, according to Swipesum.

With lower costs, faster settlement times, greater security, and enhanced client convenience, ACH through FlexPoint offers a modern and efficient way for California MSPs to take control of their payment processing.

Conclusion: Reduce Processing Costs AND Maintain Compliance with Credit Card Surcharging

Understanding California’s pricing laws—and the intent behind them—can help your MSP avoid compliance issues, client confusion, and financial setbacks. While the state restricts how credit card fees can be disclosed, it doesn’t necessarily prevent MSPs from managing those costs strategically.

By exploring compliant options like built-in card-inclusive pricing, offering ACH, and implementing fast and alternative payment solutions like Same-Day ACH, you can reduce or even eliminate processing costs without disrupting the client experience.

FlexPoint simplifies this process by automating compliant billing practices, supporting client-preferred payment methods, and giving you control over how fees are factored into your pricing.

Enhance your MSP’s bottom line and compliance with automated credit card surcharging solutions from FlexPoint.

Navigate California’s regulations and simplify your payment processes using FlexPoint today.

Schedule a demo to see how FlexPoint can transform your financial operations and maximize profitability.

{{demo-cta}}

Additional FAQs: Credit Card Surcharging in California for MSPs

{{faq-section}}