According to Scribe, MSPs work with an average of 122 clients and must manage recurring monthly payments from most of them. According to Mordor Intelligence, the MSP market size in the U.S. is expected to grow at a CAGR of 10.82%, reaching $104.90 billion by 2029 from $62.76 billion in 2024.

MSPs must prepare for this growth by simplifying client payment collection and complying with payment regulations. Several regulations govern MSP payments, from protecting sensitive client data to minimizing processing fees.

Non-compliance with MSP payment regulations can lead to severe legal consequences, financial penalties ranging from $5,000 to $100,000 monthly, lost clients, and reputational damage. As payment regulations change to adapt to technological advancements, MSPs must be prepared to remain compliant.

This article will help MSPs navigate payment regulations across different states efficiently and effectively. We will also discuss the compliance strategies and best practices for smoother payment collection for MSPs.

Overview of Payment Regulations Impacting MSPs

MSP payment regulations impact all aspects of an MSP's business operations. You must comply with PCI DSS to maintain payment security, EFTA to manage chargebacks, AML to prevent money laundering, CCPA to ensure data privacy and other relevant local compliance requirements.

According to the Global Financial Stability Report, cyber incidents are increasing and may result in losses of up to $2.5 billion. Regulations undergo rapid changes to keep up with increasing cybercrime rates. The PCI DSS 4.0 standard became mandatory on April 1, 2024, and 51 new requirements will become mandatory on March 31, 2025.

Complying with these regulations can be complex for MSPs handling clients from different geographies, varying payment cycles, and inconsistent payment methods. However, the risk of non-compliance is not worth it.

Depending on the severity and nature of the compliance breach, non-compliant MSPs would face legal and financial burdens. Beyond direct economic costs, non-compliance in the long term impacts the MSP’s reputation and causes a loss of customer trust.

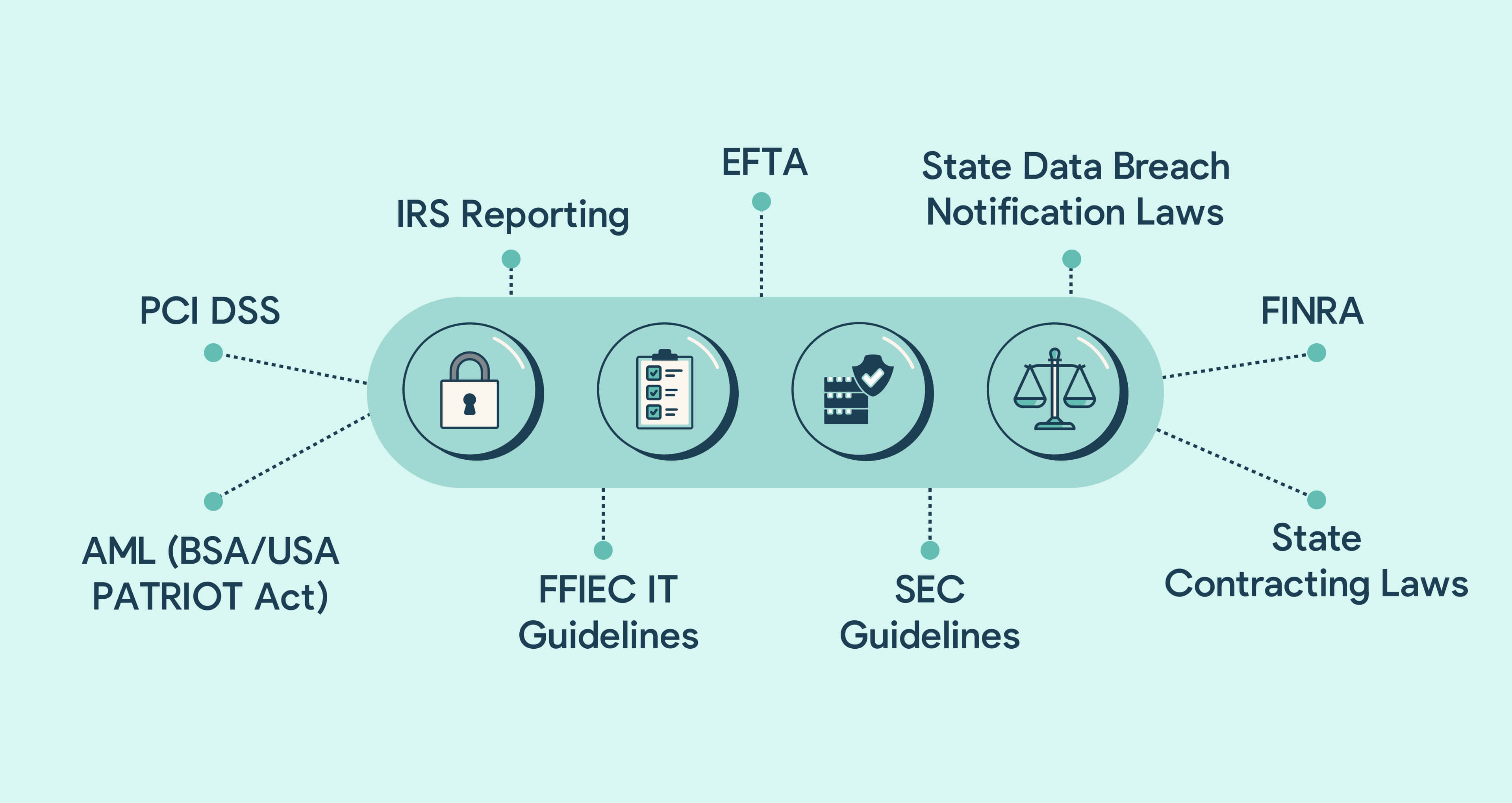

Here are the critical payment regulations impacting MSPs:

1. Payment Card Industry Data Security Standard (PCI DSS)

According to Verizon, only 52.4% of companies maintain payment data security systems, and only 47.6% test these systems regularly.

However, MSPs collecting credit card payments must comply with the PCI DSS security standard.

PCI-DSS sets guidelines for securely handling, processing, and storing payment card information. It applies to all MSPs regardless of size, type, and location. To ensure compliance, you must understand the 4 PCI merchant levels and their regulatory requirements. The regulations get stringent as your MSP's number of transactions and complexity of operations increases.

Here are the details of PCI compliance levels:

PCI Compliance Levels

PCI non-compliance can result in hefty fines of $5,000 to $100,000 per month, and you may even lose the privilege to process credit card payments. In a data breach, credit card processors may impose additional fines of $50 to $90 per exposed customer record, increasing financial liabilities.

Moreover, it damages your MSP’s reputation and leads to customer churn, as 75% of U.S. consumers would stop doing business with a company after a cybersecurity incident.

2. Electronic Fund Transfer Act (EFTA) – Regulation

EFTA is a framework for the rights, liabilities, and responsibilities of parties involved in electronic funds transfer. It mandates MSPs to maintain fee transparency and obtain client transaction authorization.

MSPs must comply with EFTA disclosure requirements under Regulation E when receiving payments through electronic fund transfers (EFTs) using telephone, computer, or any electronic device.

The regulation mandates informing customers about electronic transfer terms and their rights regarding unauthorized transactions. MSPs should also have a transparent process for resolving electronic fund transfer errors.

Non-compliance with EFTA can result in fines ranging from $5,000 to $10,000 or imprisonment of 1 to 10 years. MSPs may also lose the ability to process electronic payments, which may disrupt their business operations.

3. Internal Revenue Service (IRS) Regulations

MSPs must adhere to IRS guidelines regarding accurately reporting all income received. You must also issue Form 1099-NEC to report payments of over $600 to a contractor or vendor in a calendar year.

The penalty for failing to comply with IRS regulations may lead to scrutiny. Non-compliance with filing Form 1099-NEC results in hefty penalties as follows:

IRS Non-Compliance Fine (Cost Per Statement)

You may face criminal charges if there's evidence of intentional tax evasion or fraud.

4. State-specific Data Breach Notifications Laws

State-specific data breach notification laws in the U.S. have been enacted by all 50 states, including the District of Columbia, Guam, Puerto Rico, and the Virgin Islands. They mandate organizations to notify affected individuals promptly in case of a security breach that compromises private or financial information, including:

- Social Security Numbers

- Bank account numbers

- Credit or debit card numbers

- Biometric data (in some states)

In all cases, you must notify all individuals impacted by the breach within 30 to 60 days of discovering it. However, specific states also require organizations to notify state attorneys general or consumer protection agencies if the breach affects more than the specified people.

5. Financial Industry Regulatory Authority (FINRA)

The Financial Industry Regulatory Authority (FINRA) regulates MSPs serving clients in the financial sector.

FINRA regulations mandate firms to maintain compliance and protect sensitive financial data to keep their licenses and operate legally.

According to FINRA, firms must protect sensitive client information through robust cybersecurity measures, such as risk assessments, incident response plans, and employee training on security protocols.

FINRA mandates reporting suspicious activities and potential fraud. Non-compliance may result in hefty financial penalties ranging from $5,000 to $310,000.

Additionally, your MSP may face reputational harm and operational disruptions that impact service delivery.

6. Anti-Money Laundering (AML) Laws

Compliance with anti-money laundering (AML) laws is essential for MSPs receiving monthly payments from various clients. These laws prevent the illegal movement of money by ensuring businesses do not inadvertently facilitate money laundering or terrorist financing.

According to the Bank Secrecy Act (BSA) and the USA PATRIOT Act, MSPs must fulfill reporting requirements and due diligence procedures. It involves:

- Know Your Customer (KYC): Verify clients' identities and monitor their financial activities to assess risk.

- Customer Due Diligence (CDD): Conduct CDD to identify potential money laundering risks.

- Ongoing Monitoring: Continuously monitor and detect unusual transaction patterns.

- Reporting Obligations: For suspicious transactions, file suspicious activity reports (SARs) with the Financial Crimes Enforcement Network (FinCEN).

Non-compliance leads to legal actions from regulatory bodies or lawsuits from affected parties. It leads to substantial fines. For example, the banking industry paid $835 million+ in penalties for not complying with AML laws in 2023.

7. U.S. Securities and Exchange Commission (SEC) Cybersecurity Guidelines

U.S. Securities and Exchange Commission (SEC) has laid cybersecurity and risk management guidelines for MSPs with clients in the securities sector. You must adhere to the following regulations:

- Fulfill Incident Disclosure Requirements: Effective December 18, 2023, report cybersecurity incidents within four business days of identification.

- Comply with CIRCIA (Cyber Incident Reporting for Critical Infrastructure Act): Passed in March 2022, the CIRCIA law mandates reporting cybersecurity incidents within 72 hours.

- Meet the requirements of Cybersecurity Frameworks: Comply with established frameworks like the NIST Cybersecurity Framework and CIS Controls to meet SEC requirements.

- Follow Data Protection and Privacy Compliance Laws: Implement encryption and multi-factor authentication (MFA) to comply with GDPR and CCPA.

- Ensure Contractual Obligations: Clearly define incident detection, response, and reporting roles in your contracts to ensure compliance with SEC guidelines.

The SEC has broad enforcement powers, including the ability to impose sanctions such as cease-and-desist orders, suspension of trading privileges, and fines of up to $25 million.

8. Federal Financial Institutions Examination Council (FFIEC) IT Guidelines

MSPs working with banks or financial institutions must adhere to FFIEC information technology management and security guidelines. The FFIEC regulations are outlined in the following documents:

- IT Examination Handbook: Details of cybersecurity and IT controls financial institutions should adhere to.

- Cybersecurity Assessment Tool: Helps institutions identify their cybersecurity risks.

- Outsourcing Technology Services Booklet: Outlines specific standards for third-party service providers, which includes MSPs.

According to these documents, MSPs must implement the following security protocols to protect sensitive data:

- Multi-factor authentication for data access control.

- Encryption of data in transit and at rest.

- Regular vulnerability testing and patch management.

- Assess risk and develop mitigation strategies for different levels of threats.

- Create and test backup plans and disaster recovery protocols.

- Ensure rapid incident response to breaches, including containment, investigation, and remediation.

Failure to comply with FFIEC guidelines can result in a financial penalty of up to $2 million. If non-compliance causes data breaches or disruptions for financial institutions, MSPs may face lawsuits from clients. Depending on the breach, it can also lead to revoked contracts or licenses.

9. State Contracting Laws

Contract law governs the interpretation, enforcement, and resolution of agreements in courts.

A valid contract requires clear terms, mutual consent, consideration, and intent to create a binding agreement. MSPs must follow local state laws regulating their operation, including payment terms and obligations.

Each state has rules on contract terms and payment obligations that MSPs must follow.

For example, Louisiana Senate Bill 273 (Act 117) requires MSPs servicing state, parish, or municipal governments to register with the Secretary of State and renew this registration every two years.

You must check the specific payment timelines, penalties for late payments, and reasonable time frames for dispute resolution applicable to the states where you operate. It may also include late fees regulations, refund policies, and notice requirements for contract changes.

States have specific fines for violations, such as data protection laws and consumer protection statutes. The Federal Trade Commission (FTC) may impose penalties from $5,000 to $1 million daily for violations.

Key Compliance Strategies for MSP Payment Regulations

MSPs must comply with state and federal payment regulations to avoid fines. You must stay updated on the latest laws in your operating states.

Using secure payment systems with encryption and fraud monitoring helps make transactions safer.

Conduct regular payment audits to catch and fix compliance gaps. Train staff regularly on payment regulations to reduce errors.

Integrating automated tools and software solutions simplifies compliance processes by automating compliance tasks and reducing human error.

Automated payment systems detect anomalies and potential violations more quickly than manual methods. MSPs can use the alerts to respond promptly to compliance issues and reduce the risk of costly penalties.

Here are the best practices MSPs must implement to ensure compliance with payment regulations:

1. Multi-factor Authentication (MFA)

Multi-factor authentication (MFA) is a security system requiring multiple authentication methods to verify a user's identity before a login or transaction.

MFA combines two or more independent credentials for authenticity. It includes:

- The password that the user knows

- A security token that the user has

- Biometric verification of the user

Using the layered approach, MSPs can increase the security of their payment systems and protect sensitive cardholder data from unauthorized access.

According to MarketsandMarkets, the global MFA market will grow at a CAGR of 18% and is estimated to reach $34.8 billion by 2028, with North America being the largest market size.

Stricter regulations are pushing MSPs to adopt MFA solutions to protect cardholder information. Updates to PCI DSS and the FTC Safeguards Rule mandate MFA for accounts accessing sensitive data, highlighting its importance in compliance.

2. Compliant Payment Software Solutions

Compliant payment software solutions help MSPs comply with state and federal regulations. Their built-in compliance features enforce encryption standards, data protection, and secure transmission protocols to minimize the risk of data breaches.

Audit trails, reporting features, and automated alerts help promptly detect any potential security threats. MSPs can use these insights during regulatory audits.

In addition, compliant payment software solutions save costs by protecting against potential data breaches and fines by updating to evolving standards and compliance requirements.

3. Implement Robust Security Measures

According to IBM, the average data breach cost is $4.88 million, and 75% of it consists of lost business and post-breach response.

MSPs must safeguard client data gathered during payment collection to comply with PCI DSS and cybersecurity regulations.

Key measures include:

- Encryption: To make data unreadable for unauthorized parties

- Tokenization: Reducing the risk of exposing actual payment information by replacing sensitive data with a unique identifier

Secure networks: Using firewalls and MFA to protect against cyber threats.

4. Audit and Risk Assessment

MSPs must systematically review and evaluate their payment processes to identify weaknesses, inefficiencies, or compliance shortfalls.

Regular audits help identify and fill compliance gaps before they result in fines or penalties.

A proactive risk assessment approach reduces the chances of data breaches, prevents financial losses, and protects the company's reputation. You must create a detailed audit plan that includes scope, timelines, resources, and methodologies.

In addition, MSPs should implement strict security protocols for all employees who handle payment information. You should provide regular training on data protection best practices and enforce strict password policies with role-based access to sensitive information.

5. Contract Management

MSPs must maintain contracts and transaction records that help with audits and compliance reporting. Accurate documentation allows for quick identification and resolution of discrepancies and helps maintain an MSP's operational integrity.

All MSP contracts must meet legal standards, and you must regularly review the following:

- Standard templates are used for each contract

- Contract terms are compliant with the latest regulations

- All parties are promptly informed of amendments

Automated contract management tools help regularly update contract templates to prevent non-compliance due to outdated agreements. It helps by:

- Providing reminders for renewals and changes

- Streamlining communication between involved parties

- Minimizing oversight

6. Data Encryption and Secure Transaction Protocols

According to IBM’s Cost of a Data Breach Report 2023, customer personally identifiable information (PII) is among the top compromised data during a breach.

Strong encryption helps protect sensitive data in financial transactions, ensuring it remains secure during transmission and at rest.

MSPs must safeguard their clients' information using established standards like AES-256 for data encryption. They must also employ HTTPS and secure shell (SSH) protocols to protect data moving across networks and Transport Layer Security (TLS) to ensure secure communications between client endpoints and servers.

Implement a robust key management solution for secure encryption key generation, storage, and rotation. Limit key access to authorized personnel.

Conduct regular audits to ensure compliance and effectiveness of encryption practices. It improves trust in the MSP's data handling practices and ensures compliance with regulatory standards such as PCI DSS.

7. Document Policies and Procedures

Documenting all compliance policies and procedures helps maintain consistent and secure compliance practices.

According to the Occupational Fraud Report 2024 by the Association of Certified Fraud Examiners (ACFE), organizations with documented fraud prevention policies have 50% fewer fraud incidents than those without.

Detailed documentation is a single source of truth that guides employees in adhering to legal and regulatory requirements. It includes guidelines for handling sensitive information and incident response plans.

The policies must be current to keep up with changing security threats and regulations. It also helps MSPs keep documentation ready for audits or inspections.

In addition, MSPs should document incident response plans in case of a data breach or other security incident. It helps mitigate damage by quickly informing affected parties. These documents should also be easily accessible to clients to boost transparency and trust building.

8. Regular Compliance Training

According to Drata’s 2023 Compliance Trends Report, companies spend an average of 4,300 hours a year on compliance, and all see value in adopting continuous compliance.

MSPs must keep staff trained and updated on regulatory changes as standards and guidelines are updated often. They must also be aware of emerging threats and technological advancements.

A structured training program includes regular sessions, workshops, and online courses. Training employees on recognizing fraud can help prevent security breaches and mitigate losses due to damaged client trust.

Conclusion: Enhancing Compliance and Efficiency in MSP Payment Operations

Compliance in MSP payment operations helps protect client data and maintain operational integrity. MSPs must implement robust data protection and conduct regular risk assessments to fix potential vulnerabilities.

A proactive compliance strategy prevents legal issues and financial losses. You must keep staff aware and systems updated on current regulations and emerging threats. This strategy builds client trust by showing a commitment to data security and compliance.

Technological solutions like FlexPoint help MSPs streamline compliance and optimize payment processes efficiently. The platform strengthens compliance through encryption, tokenization, and automated fraud detection.

FlexPoint helps:

- Makes PCI compliance accessible through SAQ-A (Self-Assessment Questionnaire A)

- Integrates with existing systems to enhance their functionality

- Review transactions for adherence to regulatory standards

FlexPoint's real-time monitoring and reporting give MSPs immediate insights into compliance and financial transactions. It allows proactive adjustments to avoid service disruptions.

Using FlexPoint, streamline your compliance with MSP payment regulations. Our automated payment solutions simplify the complexities of payment compliance, ensuring your operations are efficient and secure.

Visit our website or contact us today to learn how we can help you enhance your payment compliance strategies.