Managed Service Providers (MSPs) in Massachusetts face a unique challenge when it comes to payment processing: credit card surcharging is explicitly prohibited under state law as of [$c-month-year]March 2025[$c-month-year]. This means an MSP cannot pass along credit card fees to clients who pay with credit cards, unlike MSPs in many other states.

Instead, Massachusetts MSPs often shoulder the entire burden of 2–4% credit card processing fees on every credit transaction. Over time, absorbing these fees eats into already thin margins and can become a significant financial strain.

This article will help Massachusetts MSPs understand the state’s surcharging regulations and explore compliant cost-management strategies.

We’ll discuss the laws, why they exist, and how you can navigate them, highlighting alternatives like ACH payments that keep you both profitable and compliant.

Disclaimer: This content is for informational purposes only and does not constitute legal advice. MSPs should conduct due diligence and consult with a legal professional to ensure full compliance with Michigan’s surcharging regulations.

What is Credit Card Surcharging for MSPs in Massachusetts?

Credit card surcharging is the practice of adding a small percentage fee or flat charge to a client’s bill when they pay by credit card.

Essentially, it passes the cost of the credit card processing fee back to the client. In U.S. states where surcharging is allowed, an MSP (or any business) might add, say, a 3% fee on an invoice if the client chooses to pay by credit card.

This helps the MSP recoup the merchant fees charged by Visa, Mastercard, etc. Surcharging typically requires clear disclosure to clients and often can’t exceed the actual processing cost or specific caps set by card networks.

However, Massachusetts is a unique case. As of [$c-month-year]March 2025[$c-month-year], credit card surcharges are prohibited by law in Massachusetts.

If a client pays a $10,000 invoice with a credit card, the MSP must absorb the ~$300 in processing fees rather than charging the client more to cover it. For MSPs with tight budgets, those fees add up quickly.

Understanding these regulations is critical—not only to avoid legal trouble but also to manage your payment costs wisely.

Compliance with the law ensures you won’t face fines or payment disputes, and it propels you to explore alternative strategies (like offering ACH or other payment methods) to handle the expense of credit card transactions.

By understanding what surcharging is and why Massachusetts does not permit it, you can better navigate your billing practices and find lawful, client-friendly ways to offset payment processing costs.

{{cal-one}}

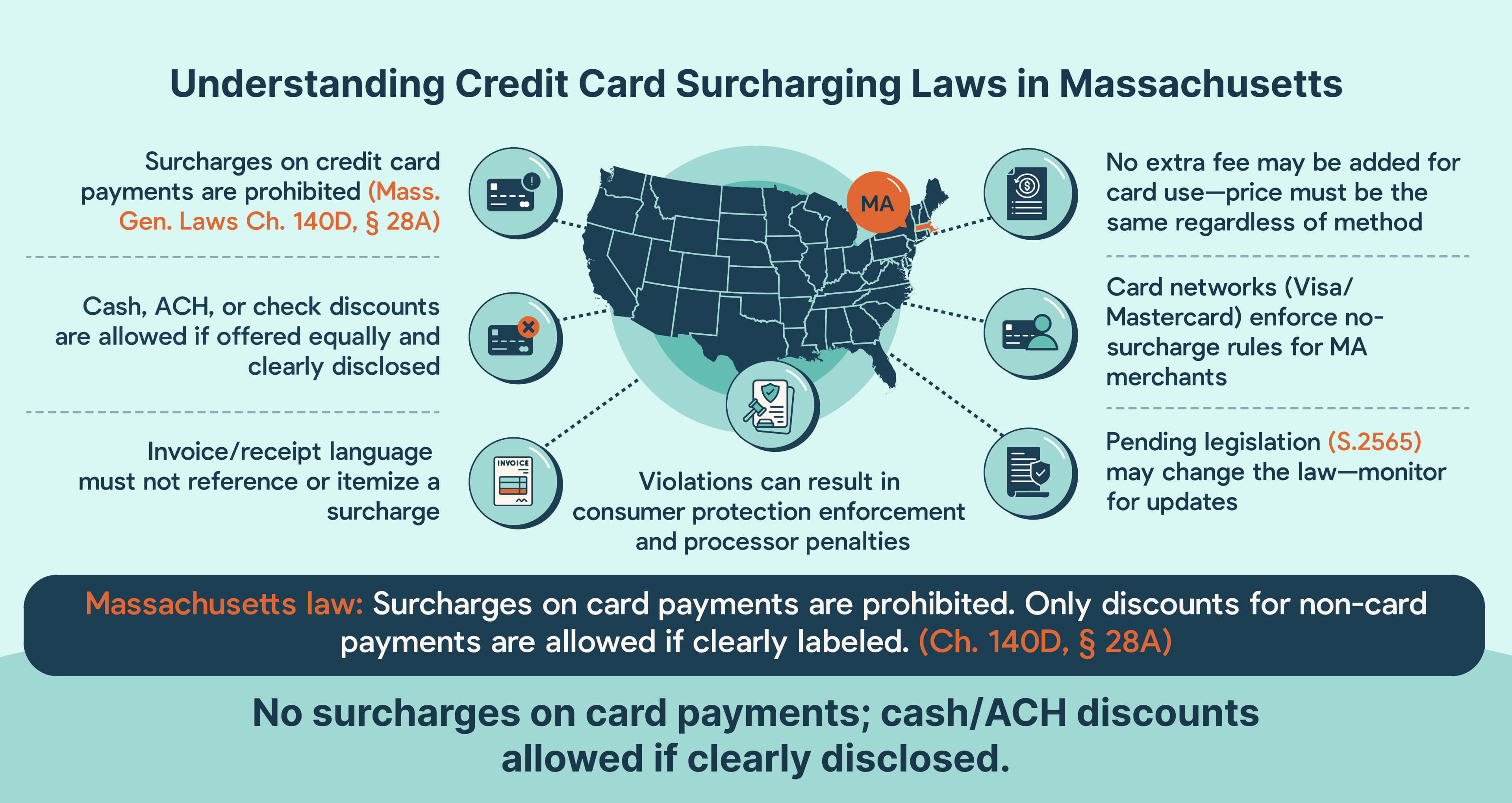

Understanding Credit Card Surcharging Laws in Massachusetts

Massachusetts has one of the strictest stances in the country regarding credit card surcharges.

Mass. General Laws Ch. 140D, § 28A explicitly states that no seller may impose a surcharge on a buyer who chooses to use a credit card instead of cash, check, or another payment method.

It reads, (in part):

“No seller in any sales transaction may impose a surcharge on a cardholder who elects to use a credit card in lieu of payment by cash, check or similar means.”

In plain language, if you’re an MSP selling services in Massachusetts, you cannot add an extra fee just because a client pays by credit card.

The prohibition on surcharging was established to promote fairness and transparency for consumers.

By banning surcharges, Massachusetts ensures the price a client sees upfront is the price they pay, regardless of payment method. It avoids scenarios where a client might feel “nickel-and-dimed” by unexpected fees.

Instead, any price differences for cash vs. credit must be made through discounts for other payment forms (which the law does permit). This approach is meant to protect clients from high or hidden charges and encourage fair competition.

It’s important to note that Massachusetts (as in all states) does allow “cash discounts,” as long as it’s offered to all clients and clearly disclosed.

In effect, a “cash discount” is just the inverse of a surcharge: you advertise the higher credit card price as the regular price, and give a small discount for paying with cash or other low-cost methods.

For example, you might list an IT service at $1,030 but give a $30 discount if the client pays via ACH or check, effectively recouping what would’ve been the card fee without calling it a surcharge.

The key is that the incentive is framed as a discount for non-card payments, not a penalty for card use. This distinction might seem semantic, but it’s exactly how some companies navigate the ban legally.

Still, it must be done carefully and transparently.

Credit card companies themselves also recognize Massachusetts as a no-surcharge zone.

For instance, Visa’s merchant guidelines acknowledge that certain states prohibit surcharging, and Massachusetts is included in that list. Card networks like Visa and Mastercard lifted their own bans on surcharging back in 2013 (after a legal settlement), but they defer to state laws.

Although most U.S. merchants can surcharge within card network rules as of [$c-month-year]March 2025[$c-month-year], Massachusetts merchants cannot because state law overrides it.

If a Massachusetts MSP tried registering a surcharge program with Visa or Mastercard, the acquirer/bank would likely reject it due to the state restriction.

{{debit-cta}}

MSPs in MA should not even attempt to implement surcharges through their payment processor—if your MSP address is in Massachusetts, the systems are typically set to disallow it.

Following federal court opinions that held similar bans in Florida, California, and Texas to be unconstitutional and therefore unenforceable, on January 13, 2020, the Massachusetts Division of Banks published an opinion letter that did not take a final position on the matter. Still, it acknowledged the constitutional questions surrounding the surcharge ban.

Despite this, Visa still includes Massachusetts on its list of states that prohibit surcharging, and most payment processors continue to enforce the restriction in accordance with state law.

Recognizing the burden of credit card processing fees on businesses, there have been recent efforts to change the law. A bill known as S.2565, “An Act relative to transparency in credit card fees,” was introduced to the Massachusetts legislature in 2024.

If passed, this legislation would lift the surcharge ban and allow businesses (including MSPs) to add credit card surcharges under certain conditions (often called “guardrails”).

However, as of this writing, that bill has not become law. It’s still important to stay informed—this area is evolving, and pressure from small business communities could eventually lead to a change.

Monitor the Massachusetts General Court’s updates or industry news for any movement on surcharge legislation. Until any new law is enacted, the current prohibition remains in full effect. Violating the surcharge ban can lead to legal and financial repercussions.

Credit card processors and networks also monitor compliance. If they discover a merchant surcharging illegally, the merchant could face consequences like termination of their merchant account or network fines.

In summary, the cost of non-compliance—legal issues, fines up to potentially a few hundred dollars per violation, not to mention reputational damage—far outweighs any short-term gain from surcharging. MSPS must follow the law diligently in Massachusetts.

Fortunately, there are other ways to manage processing fees without breaking any rules.

Why Credit Card Surcharging is Prohibited in Massachusetts

Massachusetts enforces one of the most definitive bans on credit card surcharges in the United States, based on Chapter 140D, Section 28A of the General Laws. The statute is direct in its language: Sellers are not allowed to impose additional fees when a customer opts to pay by credit card rather than cash or check.

This law's primary purpose is to prevent any shift in pricing based solely on payment method. Lawmakers intended to uphold transparency in sales transactions and reduce the risk of misleading practices.

The law helps ensure clients can trust the advertised or quoted price to be the final price by eliminating the ability to tack on fees at the point of sale.

This rule is designed to protect individual buyers and create consistency in how businesses present their pricing. It removes ambiguity around payment-related charges and levels the playing field for all clients, regardless of how they choose to pay.

Legal Implications and Penalties for Violating Surcharge Laws

MSPs that impose surcharges in Massachusetts—even unintentionally—are exposing themselves to legal and financial risk.

While the state statute doesn’t include a fixed penalty amount, violations may be treated as unfair or deceptive practices under consumer protection laws. That opens the door to enforcement actions, complaints, and fines administered by the Attorney General’s office.

In addition, payment networks like Visa and Mastercard require compliance with state laws. A violation could result in processor intervention, account suspension, or financial penalties imposed by the networks themselves.

MSPs can reduce risk by adopting strong internal billing controls. That includes disabling surcharging features in any software used, clearly labeling all client incentives as discounts rather than fees, and reviewing invoice templates to confirm they reflect Massachusetts compliance.

{{usa-cta}}

Alternative Cost-Effective Payment Methods for Massachusetts MSPs

Since adding a credit card surcharge fee isn’t an option in Massachusetts, MSPs must manage payment costs strategically. One of the most effective solutions is encouraging legally compliant alternative payment methods with much lower fees.

The standout option for most MSPs today is ACH payments. ACH (Automated Clearing House) payments are bank-to-bank transfers. Instead of the client putting a charge on their credit card, they would authorize a direct debit from their bank account for the invoice amount.

For example, if you bill a client $10,000 for managed services, an ACH transfer would pull $10,000 from the client’s checking account into your business account.

The cost of ACH transactions is significantly lower than that of credit card processing. ACH fees are often a flat rate (between $0.25 and $1.00 with FlexPoint) or a very small fee (like 0.5% or lower), with many caps in place.

Compare that to the ~3 to 4% that credit cards would cost – the savings are substantial. With ACH, an MSP can avoid the high interchange fees and network assessments that come with cards.

Beyond just cost, ACH offers other benefits for MSPs compared to credit cards:

1. Faster Processing

Traditionally, standard ACH took 3 to 5 business days to clear. But modern fintech solutions (like FlexPoint) offer Same-Day ACH capabilities.

FlexPoint’s Same-Day ACH means if you initiate a payment before the 4 PM ET cutoff window, the funds can reach your account by the end of that business day.

Faster payments mean better liquidity and less time spent on accounts receivable follow-up.

For MSPs who often manage tight cash flow to pay for software licenses, contractor fees, or payroll, getting client payments sooner can relieve a lot of stress.

2. Lower Fees On High-Value Payments

MSP contracts and projects can be pretty large, totaling thousands or even tens of thousands per month per client.

ACH, even Same-Day, might cost only a few dollars or a nominal monthly fee for unlimited usage—ACH payment fees average between $0.25 and $1.00 per transaction. The money saved goes straight back to your bottom line.

Over a year, switching a handful of big clients from credit cards to ACH could save tens of thousands of dollars that would otherwise go to the card companies. That money can be reinvested in the business to keep service prices competitive.

3. Security and Reliability

With ACH, no sensitive card number is keyed in each time, and there is less risk of fraud compared to credit cards in card-not-present transactions.

In JP Morgan’s 2023 AFP Payments Fraud and Control Survey Report, 30% of businesses reported incidents of fraud with ACH debits and credits compared to 36% for commercial and corporate credit cards.

ACH payments are authorized directly by clients from their bank accounts, which can also reduce chargeback scenarios.

For example, a disgruntled client can easily dispute a credit card charge. These might result in a chargeback. According to Swipesum, the average cost of a chargeback is $190 per dispute, so they are worth avoiding.

Importantly, ACH disputes (bank reversals) exist but are more straightforward if you have proper authorization on file.

Additionally, electronically debiting via ACH eliminates the hassle of paper checks, which can be lost or delayed, and require manual deposit. All transactions are digitally tracked and can integrate seamlessly into accounting systems.

4. Client Convenience

Many clients prefer ACH once it’s set up. Authorizing payments can be as simple as filling out a form once. After that, they don’t need to initiate anything manually—payments can be automated on due dates.

Busy clients appreciate not remembering to cut a check or log in to pay a bill. And unlike credit cards, there’s no risk of an ACH payment “failing” due to hitting a credit limit or an expired card number. As long as their bank account has funds, the payment goes through.

ACH offers the best of all worlds: digital, efficient, inexpensive, and now fast (with same-day processing).

Especially with a solution like FlexPoint’s integrated ACH tools, MSPs can modernize their collections while saving money.

{{ebook-cta}}

How FlexPoint Supports Massachusetts MSPs in Reducing Processing Costs

Operating within Massachusetts’s no-surcharge environment doesn’t have to put MSPs at a financial disadvantage.

FlexPoint is a platform purpose-built to help MSPs streamline billing, invoicing, and payments. The platform offers several features that directly address the challenges we’ve discussed.

Here’s how FlexPoint supports MSPs in Massachusetts:

1. Compliance and Transparency

FlexPoint’s payment tools are designed with compliance in mind. The platform is aware of various state-specific rules (like Massachusetts’s surcharge ban) and helps ensure you don’t accidentally violate them.

For example, FlexPoint does not apply any surcharging features to transactions in states where it’s illegal. Instead, it provides transparent invoicing options where any fees are clearly communicated as standard pricing or discounts, not surcharges.

With FlexPoint, MSPs can be confident that the system won’t inadvertently add an improper fee to a Massachusetts client’s invoice.

Additionally, FlexPoint can help generate reports and records that show you are abiding by the law (useful in the event of any audit or client question).

Transparency is also essential. You can easily show clients a breakdown of charges, demonstrating that you’re trying to subtly add additional fees. This builds trust and keeps you on the right side of the law and client satisfaction.

2. Operational Efficiency

FlexPoint automates and optimizes your whole billing workflow. The platform integrates with popular MSP tools to reconcile client payment data and invoicing

Notable integrations include:

These integrations mean no more manual data entry for billing and payment workflows. Invoices can be generated automatically with the correct amounts, and payment links can be sent out on schedule.

When clients pay (via ACH or credit card), the payment is automatically matched to the invoice and synced back to your accounting records.

This reduces human error and frees your finance or billing ops team to focus on more value-added tasks than chasing payments or updating spreadsheets.

FlexPoint’s automation also extends to subscription billing, usage-based billing, and notifications. The result is a streamlined payment process that runs with minimal oversight.

Consider Excellent Networks, an MSP based in El Paso, Texas, that implemented FlexPoint.

After doing so, the MSP’s invoice turnaround time was reduced from 25 days to just five.

Additionally, Excellent Networks saves 24 hours of work per year and over $10,000 in annual credit card fees with FlexPoint’s AutoPay feature and auto-reconciliations.

3. Optimized Cost Management

FlexPoint helps MSPs optimize costs in a few ways.

First, it facilitates the use of lower-cost payment methods like ACH.

FlexPoint makes it simple to set up ACH debit for clients and even offers tools to encourage clients to choose ACH at checkout (such as allowing you to highlight a “free ACH” versus a note that credit cards incur higher costs to the business).

Some MSPs using FlexPoint have introduced an “ACH preferred” policy, where they gently educate clients during the payment process that ACH is the preferred method.

Because the platform handles transactions seamlessly, clients hardly notice a difference, except when they are asked for bank info instead of card info.

Secondly, FlexPoint’s analytics and dashboard give MSPs insight into their payment fees and behaviors. You can actually see how much credit card fees are costing you and model how switching more volume to ACH would save money.

These insights empower MSPs to make data-driven decisions about payment policies and client incentives.

Finally, FlexPoint’s pricing model includes a certain number of Same-Day ACH transactions, which helps control costs (there are no surprise fees for using the faster service).

By leveraging all these features, MSPs in Massachusetts can significantly lower their operational costs and improve profitability without ever considering illegal surcharges.

FlexPoint provides the financial tools to operate efficiently within the law, turning what could be a burden (i.e., credit card fees) into an opportunity to modernize and save.

Conclusion: Navigating Payment Compliance in Massachusetts

Massachusetts’s strict prohibition on credit card surcharging presents a challenge for MSPs, but it’s a navigable one.

Understanding the law and its intent can help you avoid costly mistakes and focus on alternative solutions.

By exploring compliant avenues like ACH payments and implementing modern payment tools, you can manage or even eliminate those fees in a client-friendly way.

Embracing strategies such as offering cash/ACH discounts, leveraging Same-Day ACH for speed, and using platforms like FlexPoint for automation helps maintain your margins while keeping you within Massachusetts law.

Ultimately, the goal is to keep your MSP healthy and your clients happy while following regulations that protect both parties.

Optimize your MSP’s financial operations with FlexPoint’s ACH payment solutions.

Ensure compliance with Massachusetts’s surcharging laws while reducing costs and improving efficiency.

Schedule a demo today to see how FlexPoint can transform your payment processes.

{{demo-cta}}

Additional FAQs: Credit Card Surcharging in Massachusetts for MSPs

{{faq-section}}