As of [$c-month-year]May 2025[$c-month-year], Managed Service Providers (MSPs) in Maine face strict limitations on managing credit card payment costs, as state law continues to prohibit surcharging under any standard business transaction.

Unlike most other U.S. states, where surcharges can be applied with proper disclosures, Maine’s Consumer Credit Code bans any additional fees for using a credit card or debit card, forcing MSPs to absorb the full cost of processing each transaction. This can significantly impact profitability, especially when MSPs handle large recurring invoices.

This article will help Maine-based MSPs understand the current surcharging restrictions, explain the reasoning behind the state’s ban, and highlight lawful strategies for managing transaction costs.

We'll explore compliant alternatives, such as offering discounts for ACH payments, and show how platforms like FlexPoint can support cost-effective, legally sound billing practices.

Understanding Maine’s unique legal environment is essential. While you may not be able to shift card costs to your clients, there are still ways to reduce the financial pressure on your MSP, without crossing compliance lines.

What is Credit Card Surcharging for Maine MSPs?

Credit card surcharging involves adding an extra charge—either a percentage of the transaction or a flat fee—to the client’s invoice when they use a credit card to pay.

In many states, MSPs use this practice to recover the cost of card processing, which typically ranges from 2% to 4% per transaction, depending on the payment processor and the type of card used.

For instance, an MSP in a surcharge-permissible state might add a 3% surcharge to a $9,000 invoice, recouping $270 in card-related costs from the client.

This approach can help stabilize profit margins by passing fees from networks like Visa, Mastercard, and American Express directly to the card user. However, strict compliance rules apply: surcharges must be disclosed before the transaction and must not exceed either the actual cost of acceptance or limits set by the card brands.

Maine takes a different stance.

Under Title 9‑A §8‑509 of the Maine Consumer Credit Code, surcharging is explicitly prohibited for standard sales transactions.

If a client pays a $12,000 bill with a credit card, the MSP must absorb the $360 in processing costs rather than passing any of it on to the client. For MSPs operating on lean margins, those charges can quickly become a drag on profitability.

Rather than risk a violation, MSPs should look to alternatives like ACH transfers, which offer lower fees and fewer legal complexities.

Working within Maine’s strict framework requires careful planning, but with the right tools and practices—including support from platforms like FlexPoint—you can maintain financial control while staying fully compliant.

{{cal-one}}

Understanding Credit Card Surcharging Laws in Maine

Maine maintains one of the most restrictive legal environments in the country regarding credit card surcharges. The prohibition is clearly laid out in Title 9‑A, Section 8‑509 of the Maine Consumer Credit Code, which states that sellers may not impose a surcharge on clients who choose to pay with a credit or debit card instead of using cash, a check, or another low-cost method.

{{debit-cta}}

The law defines a surcharge as “any means of increasing the regular price to a cardholder that is not imposed on a customer paying by cash, check or similar means. A discount or reduction from the regular price is not a surcharge.”

In other words, an MSP in Maine cannot add a 3% fee to a $9,500 invoice just because a client wants to pay by credit card. The MSP would have to absorb the full $285 processing cost rather than shifting that expense to the client.

The core objective behind this prohibition is to promote transparency and fairness in business transactions. Lawmakers aimed to prevent consumers from being surprised at checkout with additional fees simply for choosing a particular payment method.

Maine’s approach reflects broader Truth-in-Lending principles, ensuring the price listed is the price paid, regardless of the client’s payment method.

Unlike many other states where surcharging is allowed under federal and network rules, Maine explicitly blocks this practice. Even though card brands permit surcharges in most jurisdictions if properly disclosed, they defer to state laws, and in Maine’s case, the answer remains a clear no.

However, Maine law does make a narrow exception for governmental entities. Under Subsection 2 of Title 9‑A, §8‑509, public institutions such as state departments, municipalities, counties, public universities, and the Maine Community College System are allowed to impose a surcharge for credit card or debit card payments used for official transactions—such as taxes, license fees, utility bills, or fines.

To qualify, the surcharge must meet two conditions:

- It must be clearly disclosed to the payer in advance.

- It may not exceed the actual cost incurred by the government agency or the fee charged by a third-party processor.

Importantly, if a debit card transaction incurs no processor fee, the government entity may not apply a surcharge at all. Government offices must also inform payers that the surcharge can be avoided by choosing another method, such as cash, check, or electronic bank transfer.

For private businesses such as MSPs, however, no such exception exists. If you’re an IT services provider in Portland or Bangor, the law applies in full. You cannot surcharge your clients under any circumstances, not even with consent or disclosure.

That said, Maine does allow for cash discounts, which offer a lawful workaround for managing card processing expenses.

For example, an MSP may set its regular service price at $1,050, then apply a $30 discount for payments made via ACH, bringing the total to $1,020. This approach aligns with the law as long as the higher amount is presented as the regular price and the discount is framed as an incentive for using a lower-cost method.

What Maine does not permit is advertising a $1,020 price and then increasing the total to $1,050 at checkout for credit card users. That would be classified as a surcharge, regardless of how the fee is labeled, and is prohibited under the law.

The bottom line for MSPs is that pricing practices must be structured carefully. Avoid surcharges entirely, rely on legal discounts when appropriate, and ensure all disclosures are consistent and compliant.

Billing automation platforms like FlexPoint can help simplify client payments while staying within Maine’s regulatory limits. We will discuss this in detail in the upcoming sections.

Why Credit Card Surcharging is Prohibited in Maine

The foundation for Maine’s surcharge ban is rooted in consumer protection.

When Title 9‑A, § 8‑509 was enacted in 2011, lawmakers clarified that sellers should not pass card processing fees directly to consumers as additional charges at checkout. The goal was to eliminate confusion, encourage consistent pricing, and prevent unfair surprises at the point of sale.

From a policy standpoint, Maine treats surcharging as potentially deceptive. Without proper framing, charging one price for card users and another for cash payers can lead clients to feel misled.

The law ensures greater clarity and consistency in client billing by requiring MSPs to either bake processing costs into their base price or offer discounts for alternative payment methods.

While federal courts have overturned similar bans in other states, Maine’s legislature has repeatedly upheld its position. Bills that would have relaxed the rule have failed to pass, and as of 2025, the surcharge prohibition remains fully enforceable.

Legal Implications and Penalties for Violating Surcharge Laws

Violating Maine’s surcharge law can result in significant financial and reputational consequences.

The Maine Bureau of Consumer Credit Protection enforces compliance and has the authority to investigate complaints. MSPs found to be in violation can face civil penalties, cease and desist orders, and be required to refund improperly charged amounts.

Fines may be imposed, and the Attorney General’s office may pursue further action under the Unfair Trade Practices Act. In more serious or willful cases, misdemeanor charges are possible, with maximum fines up to $5,000.

There’s also the matter of card brand compliance. Even if a violation slips past state regulators, card brands like Visa and Mastercard may take corrective action, including terminating a merchant’s processing agreement.

To stay compliant, Maine MSPs should:

- Avoid any language on invoices or receipts that implies a fee for credit card use.

- Clearly label any alternative payment incentives as discounts, not added fees.

- Disable surcharging features in billing or payment software that may be enabled by default.

- Ensure client-facing materials reflect the base price as the credit card price, not a discounted rate.

Platforms like FlexPoint can help MSPs ensure invoices remain compliant while giving clients multiple low-cost ways to pay. With built-in support for ACH and transparent client communications, FlexPoint enables Maine MSPs to maintain trust and avoid regulatory headaches.

In a state like Maine, where surcharging is off-limits, these strategies are essential to maintaining financial health without overstepping the law.

Alternative Cost-Effective Payment Methods for Maine MSPs

With Maine law prohibiting the use of credit card surcharges, MSPs must approach payment processing with a cost-conscious strategy that stays within legal limits. The most practical way to do this is by steering clients toward payment methods with lower fees and fewer restrictions.

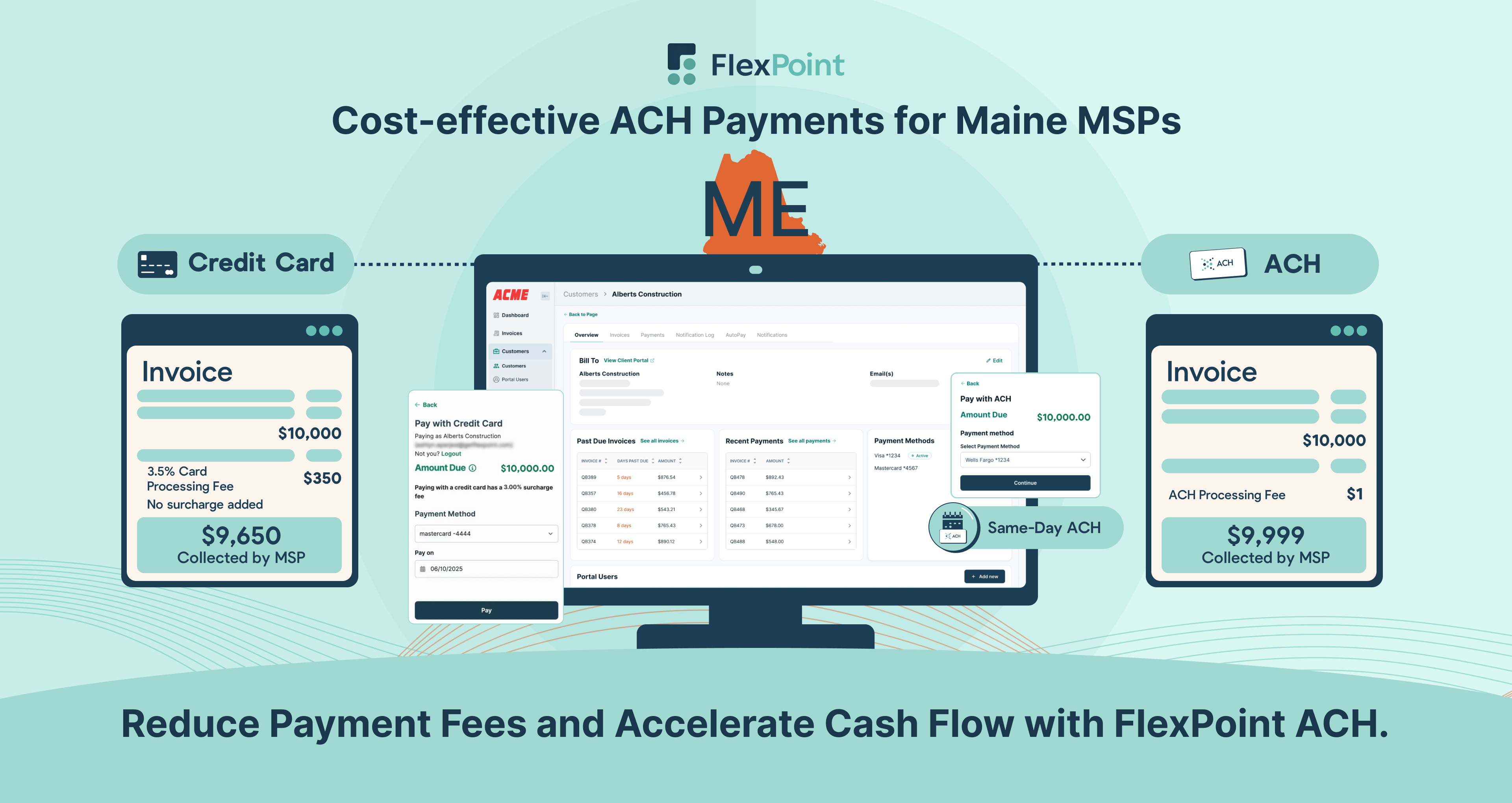

Among all alternatives, ACH (Automated Clearing House) payments are the top choice. These bank-to-bank transfers allow clients to authorize a direct debit from their account, bypassing card networks altogether.

If your MSP invoices a client for $8,600, the ACH system transfers that exact amount directly into your business account, without incurring the 3% to 4% that a credit card transaction would typically cost.

The cost difference is hard to ignore. Depending on your provider, ACH fees are often between $0.25 and $1.00 (with FlexPoint).

Compared to the $344 in processing charges you'd absorb on a $8,600 credit card payment, ACH transfers could save your MSP over $3,000 annually on just a few recurring client accounts.

And the benefits of ACH over credit card payments don’t stop with cost.

1. Faster Processing

While traditional ACH transfers used to take three to five business days, providers like FlexPoint now offer Same-Day ACH, cutting the turnaround to just a few hours. If an MSP initiates a transfer by the 4:00 PM ET deadline, the funds can be credited by the end of the day.

That’s a significant win for Maine-based MSPs, who manage tight operating budgets. FlexPoint’s Same-Day ACH offers faster deposits so you can pay vendors, cover payroll, or fund ongoing support services without waiting days for the money to clear.

2. Lower Fees On High-Value Payments

MSPs in Maine frequently handle high-value recurring contracts—monthly retainers or recurring payments in the $10,000 to $25,000 range aren’t uncommon. The financial impact of using ACH over credit cards on these invoices adds up quickly.

For example, a $12,500 invoice paid via ACH with a $0.75 fee costs your MSP virtually nothing. However, if the same client paid by credit card, you could end up absorbing $375 or more.

Over the course of a year, that single client’s payment method could represent a difference of $4,000 to $5,000 in lost revenue.

3. Security and Reliability

ACH payments reduce fraud exposure, especially for card-not-present transactions.

A client paying by credit card can initiate a chargeback with little more than a phone call. And when they do, the cost goes beyond the reversal—according to Swipesum, the average cost of a chargeback is about $190.

By contrast, ACH reversals and payment disputes are less common and require a formal request, typically within a narrow window.

If you have written authorization from the client—something FlexPoint makes easy to track—you’re in a strong position to protect your funds. ACH also eliminates the risks of expired cards or stolen credit card data, making it a secure and stable solution.

4. Client Convenience

Many clients find ACH preferable once they’ve enrolled. After providing authorization, future payments can be pulled automatically—no reminders, manual check-cutting, or monthly card re-entry.

This simplicity matters for time-strapped businesses in Maine that rely on your services. Unlike credit card payments, there’s no risk of failure due to credit limits or declined authorizations. As long as funds are in the account, the payment clears.

By using ACH, your MSP creates a more predictable and efficient receivables process, and when combined with FlexPoint, the experience becomes fully automated.

FlexPoint supports Same-Day ACH and offers seamless integration with your accounting and PSA tools, making it easier to reconcile payments and manage cash flow.

{{ebook-cta}}

How FlexPoint Supports Maine MSPs in Reducing Processing Costs

Maine’s strict ban on credit card surcharging means there’s no legal way to recover processing fees through added client charges. However, this doesn’t mean you have to accept margin erosion as inevitable.

FlexPoint was built to help MSPs run smarter billing systems legally and efficiently. The platform offers integrated tools that address the most common pain points related to payments, compliance, and client experience.

Here’s how FlexPoint helps Maine-based MSPs reduce operational costs without breaking any rules.

1. Compliance and Transparency

With surcharge laws enforced statewide under Title 9‑A, §8‑509, Maine MSPs must be especially vigilant about compliance. FlexPoint is designed to support that vigilance.

The platform automatically ensures surcharging functionality is disabled in states where it’s prohibited, like Maine. That means you can invoice clients with confidence, knowing you’re not accidentally adding unlawful fees.

Instead of building in surcharge capabilities, FlexPoint emphasizes invoice clarity. You can present service rates as fixed amounts and apply discounts transparently for ACH or check payments. Clients see accurate, upfront pricing—there’s no hidden fee or after-the-fact adjustment.

If you’re ever asked to show how your billing practices align with state law (such as during a dispute or audit), FlexPoint also allows you to export detailed reports showing your fee structure and transaction history.

FlexPoint gives Maine MSPs the tools to ensure that every invoice reflects the agreement, building trust and reducing the risk of miscommunication or compliance errors.

2. Operational Efficiency

Beyond compliance, FlexPoint offers robust automation features that reduce manual work and invoicing errors. The platform integrates with the tools you already use, such as QuickBooks Desktop, QuickBooks Online, Xero, ConnectWise, Autotask, SuperOps, and HaloPSA.

With these integrations, FlexPoint automates the entire billing lifecycle. Invoices are created with precise, up-to-date information from your PSA or accounting system, and payment links are sent automatically to clients.

When payments are received—whether via ACH or credit card—they’re matched to the appropriate invoice and synced back into your system. This eliminates the need for manual reconciliation and reduces human error.

Even subscription-based or usage-dependent billing is handled with ease. MSPs can automate notifications, due-date reminders, and recurring charges without having to track anything manually. The result is a billing process that runs quietly in the background while your team stays focused on delivering service.

Let’s take the example of Excellent Networks, an MSP that uses FlexPoint to streamline its collections process, is one such example.

While based outside of Maine, the lessons apply universally for all MSPs: invoice turnaround time dropped from 25 days to just five, and the business saved more than $10,000 per year in card fees and labor thanks to AutoPay and real-time reconciliation.

3. Optimized Cost Management

Maine MSPs often deal with tight operating margins, and the inability to add surcharges to cover credit card fees can make budgeting more complex. Instead of absorbing those costs without recourse, FlexPoint offers built-in tools that make cost reduction a natural part of your billing workflow.

Rather than asking clients to change behavior through policy changes or manual outreach, FlexPoint guides them toward more affordable payment options, like ACH, when they’re making payment decisions.

You can customize checkout messages to highlight that ACH transfers are fee-free, or gently position them as the preferred method for larger invoices. Clients are more likely to choose the lower-cost route when it’s presented clearly and without friction.

These shifts don’t require heavy lifting.

Once a client is enrolled in ACH, future payments can run on autopilot. MSPs handling recurring contracts—say, monthly retainers of $9,000 to $15,000—see real savings when payments come through bank transfers instead of cards.

Swapping just five regular clients from credit cards to ACH could result in more than $8,000 in annual savings, money that can be reinvested into your team, tools, or services.

Behind the scenes, FlexPoint tracks all of it. The analytics dashboard makes it easy to see which clients contribute most to your payment processing expenses and where small changes could have the biggest payoff.

You’ll spot patterns, evaluate the actual cost of accepting cards, and build data-driven strategies to shift behavior without modifying pricing or applying prohibited fees.

Same-Day ACH functionality adds another layer of value. Faster access to funds means more control over your cash position, and since FlexPoint includes Same-Day transfers in its pricing, you avoid last-minute fees or delays when time-sensitive payments are involved.

These features give Maine MSPs a realistic and legal path to stronger cost control, turning compliance challenges into opportunities for smarter financial operations.

Conclusion: Navigating Payment Compliance in Maine

Maine’s clear stance against credit card surcharges creates limitations, but those limits don’t have to undermine your MSP’s financial health. With the right strategies, it’s entirely possible to reduce transaction costs while staying compliant with state law.

The key is to understand what the law allows and doesn’t. Instead of trying to offset fees through prohibited surcharges, Maine MSPs can shift toward more cost-efficient practices.

Encouraging clients to use ACH, offering legally permitted discounts for check or bank payments, and implementing automated billing through FlexPoint all contribute to a more efficient operation.

By making thoughtful adjustments, such as introducing Same-Day ACH to enhance cash flow or leveraging data insights to manage payment preferences, you can maintain your margins without ever risking a compliance issue.

Following Maine’s rules doesn’t mean absorbing every cost. It means working smarter with the tools available, and platforms like FlexPoint make that easier than ever.

Optimize your MSP’s financial operations with FlexPoint’s ACH payment solutions.

Ensure compliance with Maine’s surcharging laws while reducing costs and improving efficiency.

Schedule a demo today to see how FlexPoint can transform your payment processes.

{{demo-cta}}

Additional FAQs: Credit Card Surcharging in Maine for MSPs

{{faq-section}}