As of [$c-month-year]January 2025[$c-month-year], credit card surcharging is permitted in Arkansas. This practice allows businesses, including managed service providers (MSPs), to offset processing fees by passing them along to clients.

While Arkansas does not impose specific surcharge restrictions, MSPs must comply with federal regulations and card brand guidelines to assure fairness and legal compliance.

Credit card surcharging is a helpful approach to reducing the financial strain of payment processing fees. By distributing these costs to clients, MSPs can better manage operational expenses and protect their profitability.

However, careful planning and execution are paramount to maintaining compliance and preserving strong client relationships.

This guide provides Arkansas MSPs with valuable advice on implementing surcharges in alignment with federal and card brand rules.

It also explores how payment automation tools streamline compliance and simplify billing processes for transparency and client satisfaction.

Disclaimer: This information is provided for general informational purposes and does not constitute legal advice. Consult a legal professional for guidance tailored to your MSP’s distinctive circumstances.

What is Credit Card Surcharging for MSPs in Arkansas?

Credit card processing fees are unavoidable for MSPs accepting card payments.

Credit card processing fees typically range between 1.5% and 4% of a transaction’s total.

These fees cover transaction verification, processing, and security measures. They are paid to card networks, banks, and payment processors.

While necessary, they significantly strain profit margins, especially for MSPs managing recurring or high-volume transactions.

Credit card surcharging offers a solution to offset these costs.

This practice involves adding a small fee to a client’s credit card transaction, which helps cover the associated processing expenses.

MSPs preserve profitability while providing high-quality services when the financial burden is distributed across transactions.

For example, an MSP processing $60,000 in monthly credit card payments with an average 2.75% processing fee would incur $1,650 in monthly costs or $19,800 annually.

The Merchant Payments Coalition notes that credit card processing fees collectively cost U.S. businesses approximately $160 billion annually. This makes them one of the largest operational expenses, second only to labor costs.

Given this financial impact, it’s easy to see why MSPs in Arkansas are motivated to reduce these fees.

While credit card surcharging is a practical approach, it requires meticulous planning and compliance with federal, state, and card brand regulations. Missteps lead to penalties, disputes, or strained client relationships.

In addition to surcharging, some MSPs explore alternative strategies, such as reducing chargebacks or encouraging ACH payments, to lower overall costs.

For Arkansas MSPs, credit card surcharging can be beneficial when implemented thoughtfully and in line with all applicable regulations.

{{cal-one}}

Understanding Credit Card Surcharging Laws in Arkansas

Federal guidelines cap surcharges at 4%, but merchants cannot apply fees exceeding the actual cost of credit card processing.

For instance, if an MSP has a merchant discount rate (MDR) of 2.75%, their surcharge cannot exceed 2.75%, even though the federal cap allows up to 4%.

This ensures surcharges reflect legitimate processing costs rather than becoming a source of profit.

For example, consider an Arkansas MSP processing $100,000 in monthly credit card transactions with an MDR of 2.75%.

Without surcharges, the MSP incurs $2,750 in monthly processing fees, totaling $33,000 annually.

After implementing a 2.75% surcharge, they recover the full costs, considerably improving their financial position.

Alternatively, the MSP might choose a 1.5% partial surcharge, passing $1,500 of the monthly fees to clients while absorbing the remaining $1,250.

Over a year, this approach saves the MSP $18,000, balancing profitability with client satisfaction.

Arkansas merchants must clearly disclose surcharges at the point of sale and itemize them on receipts. Clients should be informed upfront to prevent disputes and maintain confidence in their transactions.

Further, according to the Durbin Amendment of the Dodd-Frank Act, surcharges may only apply to credit card transactions. This excludes debit and prepaid card payments, even if processed as credit.

{{debit-cta}}

To comply with Arkansas surcharging regulations, MSPs should:

- Disclose surcharge policies before processing transactions.

- Itemize surcharges on receipts for full transparency.

- Avoid charging fees higher than their actual processing costs.

- Only apply surcharges to credit card transactions.

Well-executed surcharging practices help MSPs recover operational costs without alienating clients.

Remaining informed of federal, state, and card network requirements is pivotal to avoiding compliance risks and legal complications.

Note: Seeking advice from legal professionals familiar with Arkansas regulations further supports accurate implementation and long-term success. As mentioned earlier, this article should not be taken as legal advice.

{{usa-cta}}

Implementing Credit Card Surcharging for Arkansas MSPs

Introducing credit card surcharges demands a thoughtful approach for MSPs in Arkansas, as it directly impacts client relationships.

Conveying surcharges as a sensible way to share costs—rather than as a profit-generating measure—helps clients understand and accept the change.

Clients value transparency, especially when it comes to financial decisions.

MSPs can initiate conversations through personalized emails or calls, explaining how these fees help cover rising credit card processing costs. Tangible examples, such as illustrating how processing fees reduce profitability, provide context for the surcharge.

For instance, an MSP might share data showing that these fees account for a substantial portion of operating costs.

Positioning the surcharge as a way to sustain service quality without increasing prices across the board also encourages acceptance.

An MSP could explain that implementing surcharges allows them to avoid blanket rate hikes, keeping services affordable for most clients.

To help MSPs adopt surcharging successfully, the following guide provides four actionable steps for implementing surcharging that remains compliant and supports client trust.

Step 1: Establish a Clear Surcharge Policy and Structure

A surcharge policy tailored to your MSP sets the foundation for successful implementation.

This document should outline the surcharge amount, the conditions for applying it, and how it will be presented to clients. Including this information in client agreements avoids misunderstandings and builds trust.

Use the policy as a chance to clarify that surcharges are intended to recover costs, not as a way to profit from them.

MSPs may choose fixed percentages, tiered rates, or flat fees depending on their operations and client preferences.

Examples of Surcharge Structures

1. Fixed Percentage Surcharge

An Arkansas MSP applies a 3% surcharge to all credit card transactions.

• Example: For a $12,000 invoice, the surcharge adds $360, for a total of $12,360.

2. Tiered Surcharge System

Rates change depending on the transaction size. Transactions under $5,000 are charged 2%, while those exceeding $5,000 are charged 3%.

• For example, a $4,500 invoice adds $90 (2%), while a $9,000 invoice adds $270 (3%).

3. Flat Fee Surcharge

A flat amount is added regardless of the transaction total—provided it does not exceed the actual processing cost or the card network's maximum surcharge cap.

- Example: A $5,000 invoice with a $50 surcharge totals $5,050.

Regardless of the structure, surcharges must reflect actual processing costs.

For instance, if a $2,000 transaction costs 2.75% to process ($55), a $75 surcharge would violate card network policies and federal rules.

Step 2: Notify Credit Card Institutions and Clients

To start surcharging, Arkansas MSPs must notify credit card networks and payment processors at least 30 days in advance. Visa and Mastercard provide online forms to simplify this process.

As Visa explains, “U.S. merchants must first notify Visa and their acquirer of their intent to surcharge at least 30 days prior to implementing surcharging. Merchants can submit a notification form to Visa at www.visa.com/merchantsurcharging.”

Once networks are notified, clients must be informed about the surcharge policy.

To ensure compliance from the beginning, MSPs can take several actions:

- Send an Email Update: Explain that the surcharge is a cost-recovery tool, not a profit mechanism.

- Include a Policy Summary: Include a section in your service agreement to ensure clients are informed.

- Detail Surcharges on Invoices: Display the surcharge amount and how it’s calculated.

For example, a $10,000 invoice with a 2.5% surcharge should explicitly list:

- Subtotal: $10,000

- Surcharge: $250

- Total Due: $10,250

Without proper disclosure, clients may dispute charges.

According to Swipesum, chargebacks cost an average of $190 per dispute; and disputes can harm client relationships. Consistent and unambiguous communication minimizes these risks.

Step 3: Update Invoicing & Billing Systems

Visa caps surcharges at 3%, Mastercard allows up to the federal limit of 4%, and all charges must stay within the actual processing cost (based on the merchant discount rate).

MSPs planning to implement surcharging must update their billing systems to comply with these and other surcharging regulations.

MSP-specific payment automation platforms like FlexPoint simplify this process by accurately calculating surcharges and adding them as separate line items on invoices.

For example, if an MSP processes a $15,000 transaction with a 2.5% MDR, FlexPoint calculates the surcharge at $375, ensuring compliance with state and card network guidelines.

Updating billing systems minimizes manual errors and streamlines operations.

Step 4: Monitor and Review Compliance

Surcharging regulations frequently evolve due to updates from Visa, Mastercard, or federal agencies. MSPs should regularly evaluate their practices to avoid potential fines or penalties.

MSPs should implement regular oversight of:

- Surcharge Limits: Charges must not exceed 3% for Visa, 4% for Mastercard, or the actual processing cost.

- Service Agreement Updates: Revise contracts and notify clients promptly about any rule changes.

- Client Feedback: Address concerns or complaints to identify potential compliance gaps early.

For example, if Visa reduces its surcharge cap to 2.5%, MSPs charging 3% must promptly update their policies, revise invoices, and inform clients to maintain compliance.

Automation tools like FlexPoint simplify these updates by recalculating surcharge amounts and ensuring invoices remain accurate.

Regular reviews of surcharging practices help MSPs avoid penalties and maintain positive client relationships. Demonstrating transparency and professionalism through compliance strengthens trust and breeds long-term success.

{{ebook-cta}}

The Role of FlexPoint in Streamlining Credit Card Surcharging for Arkansas MSPs

Managed service providers in Arkansas handle high transaction volumes, creating challenges when dealing with credit card processing fees. These fees quickly add up, cutting into profitability and straining budgets.

FlexPoint offers tailored payment automation software designed to address these financial hurdles, giving MSPs the tools they need to manage costs effectively.

Payment Processing Plans

FlexPoint provides two specialized payment plans for MSPs:

- Interchange+ Plan

- Customer Surcharge Plan

a. Interchange+ Plan

The Interchange+ Plan delivers transparent pricing by aligning fees with the specific interchange rates tied to each card type. This approach ensures more predictable processing costs for MSPs.

Example:

- Discover cards, which generally have lower interchange rates, lead to reduced fees.

- Conversely, American Express and high-reward credit cards have higher interchange rates, which increases the cost per transaction.

This plan is an excellent choice for MSPs who prefer to absorb processing fees rather than imposing them on clients.

It also provides a clear pricing structure that allows MSPs to manage overhead more efficiently.

b. Customer Surcharge Plan

The Customer Surcharge Plan allows MSPs to share the burden of credit card processing fees with clients.

By applying a flat percentage surcharge to all credit card transactions, this plan shifts the cost of processing directly to the client.

Example:

For a $7,000 transaction with a 2.5% surcharge:

- Service Total: $7,000

- Surcharge: $175

- Total Due: $7,175

This option is particularly beneficial for MSPs who want to offset rising processing costs without compromising their profitability.

FlexPoint offers additional flexibility through a shared-cost model. This approach allows MSPs to split processing fees with clients, creating a balanced solution that upholds trust while recovering some transaction costs.

Whether MSPs choose the Interchange+ Plan, the Customer Surcharge Plan, or a shared-cost model, FlexPoint provides the tools to help MSPs tailor their strategies to meet business goals while maintaining transparency with clients.

How FlexPoint Enhances Surcharging Compliance and Transparency

FlexPoint automates surcharge calculations and ensures compliance with federal laws, Arkansas state guidelines, and card network policies, such as Visa and Mastercard.

Its automated system keeps surcharges within the federal 4% cap while generating accurate, transparent invoices.

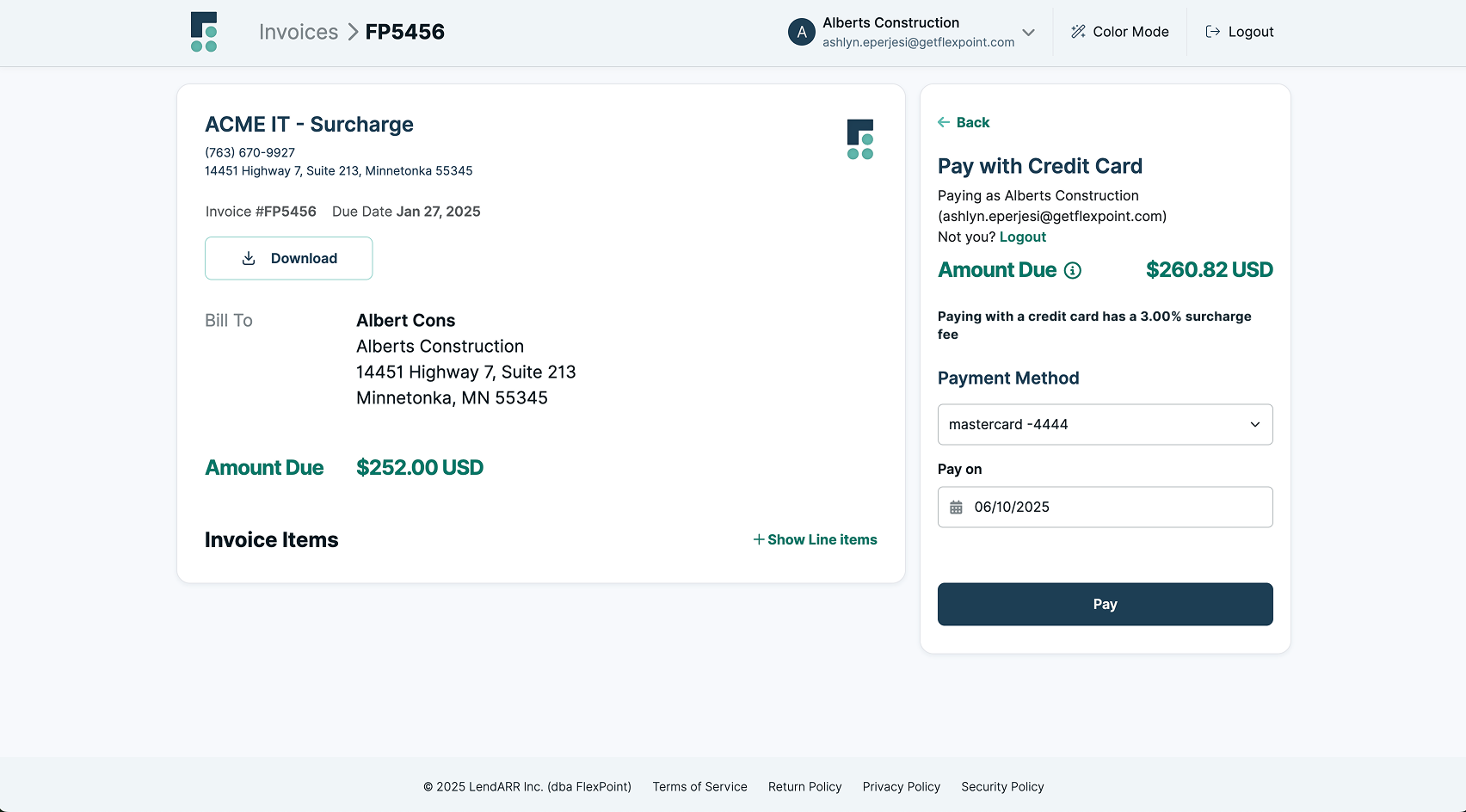

Here’s an example of an Arkansas MSP’s $13,800 invoice with a 3% surcharge:

FlexPoint’s Integration with MSP Tools for Seamless Billing

FlexPoint supports Arkansas MSPs by integrating with widely used platforms to maintain seamless workflows while reducing administrative burdens.

Some of FlexPoint’s supported integrations include:

These integrations simplify critical financial operations, reducing reliance on manual processes. MSPs can automate time-consuming tasks like invoicing, billing, and reconciliation, which often come with risks of human error.

For example, FlexPoint's integration with QuickBooks Online automatically synchronizes financial records, including surcharges, fees, and billing updates.

This automation ensures precision and saves time for teams to focus on higher-value activities.

Additional tools, such as branded client payment portals and real-time tracking, help MSPs manage payments more efficiently while keeping a clear view of cash flow. These features improve client communication and enrich overall financial management.

{{client-portal-gif}}

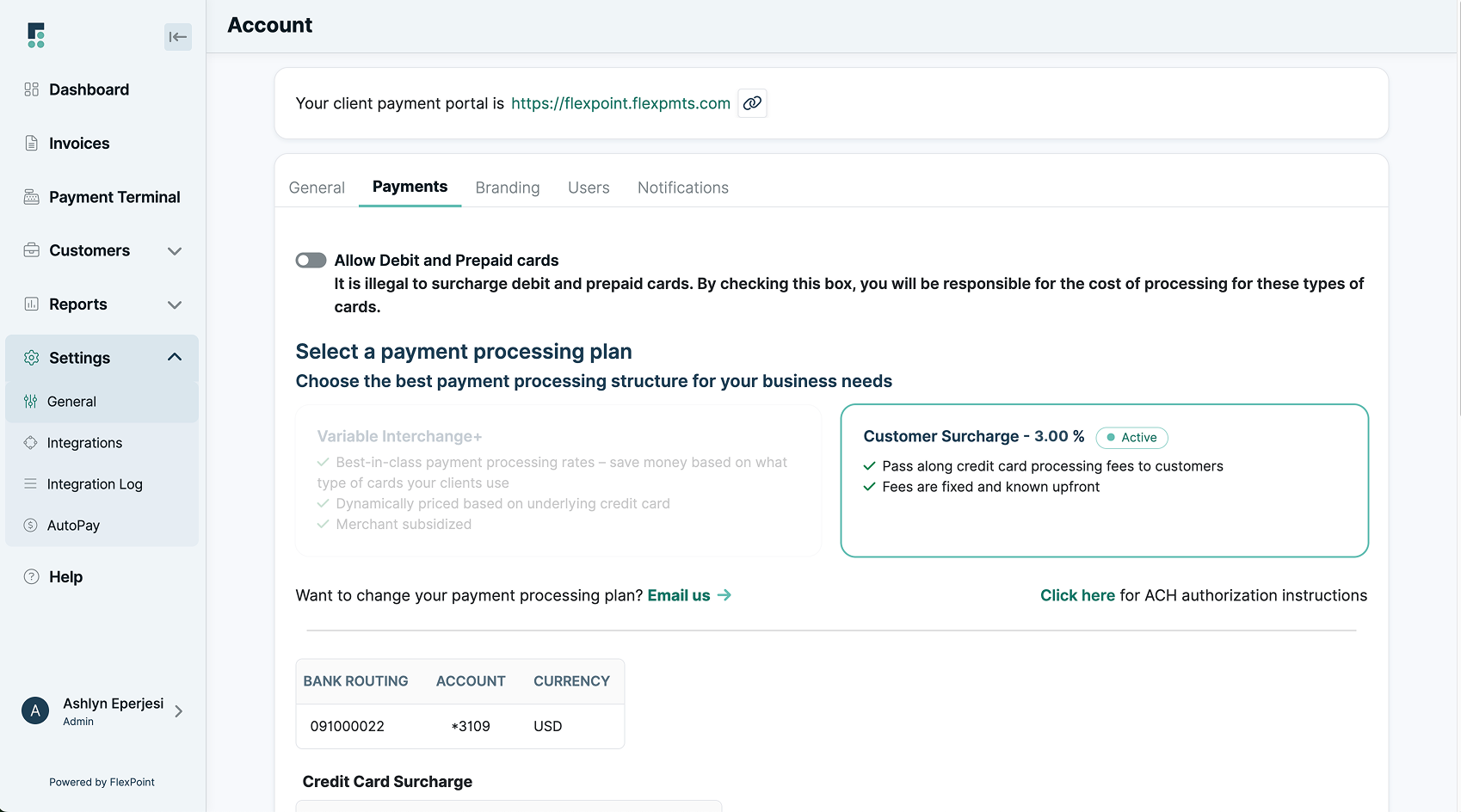

Offering Flexibility in Surcharging

{{admin-portal-gif}}

FlexPoint equips Arkansas MSPs with adaptable tools to tailor surcharging strategies according to client needs.

For example, MSPs can waive surcharges for loyal, long-term clients while applying standard fees for others.

This adaptable approach balances cost recovery with maintaining strong client relationships, offering a solution that aligns with specific business goals.

Automated payment rules ensure surcharges comply with the caps set by Visa, Mastercard, and other card networks.

For example, if a client pays with Visa, FlexPoint will automatically cap the surcharge at 3%, which is according to Visa's guidelines.

By automating these calculations, FlexPoint reduces the risk of regulatory issues and disputes, applying surcharges accurately every time.

Clients benefit from greater transparency, as surcharge details are displayed before payments are finalized.

Personalized payment portals allow clients to view invoices, update payment information, and choose payment methods directly online.

For instance, if a client typically pays with Mastercard, which carries a 4% surcharge, that client might switch to Visa to save 1%.

With FlexPoint's personalized payment portal, customers can make this update independently, avoiding delays and simplifying the process.

Clients can also update expiring card details directly through the portal to eliminate the need for MSP intervention.

This self-service capability saves time and strengthens client trust by offering greater control and convenience over their payments.

FlexPoint streamlines operations for MSPs, creating a more efficient and client-friendly payment experience.

Conclusion: Streamlining Payments with Effective Surcharging Strategies

Credit card surcharging is an appealing option for Arkansas MSPs who want to offset rising payment processing costs.

This practice helps recover costs while improving cash flow. However, its success relies on a well-structured, compliant policy and transparency with clients.

Managing surcharges manually creates challenges, especially regarding compliance with state and card network rules.

FlexPoint eliminates these obstacles with automation tools that simplify invoicing, enforce surcharge caps, and integrate seamlessly with platforms like QuickBooks, Xero, ConnectWise, and SuperOps.

With FlexPoint, MSPs implement surcharges effectively without compromising client trust.

Automated surcharging supports your MSP’s cash flow and helps maintain strong relationships with clients through straightforward and fair billing practices.

Unlock the benefits of credit card surcharging while staying compliant with Arkansas state laws.

FlexPoint makes surcharging simple, transparent, and efficient for MSPs —helping you manage costs and boost revenue.

Ready to optimize your payment processing?

Schedule a demo today and experience the power of automated compliance with FlexPoint.

{{demo-cta}}

Additional FAQs: Credit Card Surcharging in Arkansas for MSPs

{{faq-section}}